Metrika ( IF 0.9 ) Pub Date : 2022-05-21 , DOI: 10.1007/s00184-022-00866-1 Songqiao Tang , Huiyu Wang , Guanao Yan , Lixin Zhang

|

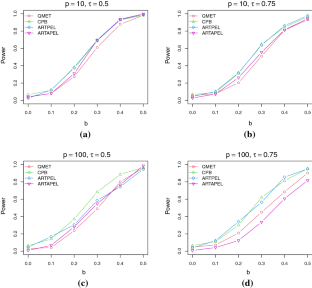

This article investigates detecting the presence of significant predictors in marginal quantile regression. The main idea comes from the connection between the quantile correlation and the slope parameter of the marginal quantile regression, which is quite different from other methods. By introducing the local linear model and the plug-in empirical likelihood method, consistent asymptotic distribution and its adjusted version are obtained. We not only circumvent the non-regularity encountered by post-model-selected estimators but also make the results more concise. Two adaptive resampling test procedures are proposed in practice by comparing the t-statistics with a threshold to decide whether to use the traditional centered percentile bootstrap or otherwise adapt to the asymptotic distribution under the local model. Simulation studies compare these two resampling tests with other competing methods in several cases. Results show that the approaches proposed are more robust for each quantile level and can control type I error well. Two real datasets from Forbes magazine and the HIV drug resistance database are also applied to illustrate the new methods.

中文翻译:

基于经验似然的检验,用于检测边际分位数回归中显着预测因子的存在

本文研究了在边际分位数回归中检测显着预测变量的存在。主要思想来自边际分位数回归的分位数相关性和斜率参数之间的联系,这与其他方法有很大不同。通过引入局部线性模型和插件经验似然法,得到一致渐近分布及其调整版本。我们不仅规避了模型后选择的估计器遇到的不规则性,而且使结果更加简洁。通过比较t在实践中提出了两种自适应重采样测试程序- 具有阈值的统计量来决定是使用传统的居中百分位自举法还是以其他方式适应局部模型下的渐近分布。模拟研究在几种情况下将这两种重采样测试与其他竞争方法进行了比较。结果表明,所提出的方法对于每个分位数水平都更加稳健,并且可以很好地控制 I 类错误。福布斯杂志和 HIV 耐药性数据库的两个真实数据集也用于说明新方法。

京公网安备 11010802027423号

京公网安备 11010802027423号