Methodology and Computing in Applied Probability ( IF 1.0 ) Pub Date : 2022-04-27 , DOI: 10.1007/s11009-022-09927-4 Yan Zhang 1 , Rufei Ma 1 , Peibiao Zhao 2

|

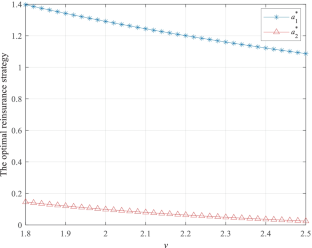

This paper is devoted to investigating a robust optimal excess-of-loss reinsurance and investment problem with defaultable risk, in which the insurer’s wealth process is described by a more general dependent risk model with two classes of insurance business. The insurer is allowed to purchase excess-of-loss reinsurance and invest in a risk-free asset, a defaultable bond and a risky asset whose price depends on a square-root stochastic factor process which makes the geometric Brownian motion, CEV model and Heston model as special cases. Our aim is to seek the optimal excess-of-loss reinsurance and investment strategy under the criterion of maximizing the expected exponential utility of the terminal wealth. Applying the stochastic control theory, the robust Hamilton-Jacobi-Bellman (HJB) equations for the post-default case and the pre-default case are first established, respectively. Then the explicit expressions of the optimal control strategy are obtained, moreover, we provide the verification theorem. Finally, some numerical examples are given to illustrate our results.

中文翻译:

具有更多一般从属索赔风险和可违约风险的稳健最优超额损失再保险和投资问题

本文致力于研究具有可违约风险的稳健最优超额损失再保险和投资问题,其中保险公司的财富过程由具有两类保险业务的更一般的依赖风险模型描述。保险公司可以购买超额损失再保险并投资于无风险资产、可违约债券和风险资产,其价格取决于产生几何布朗运动、CEV 模型和 Heston 的平方根随机因子过程模型作为特殊情况。我们的目标是在终端财富的期望指数效用最大化的准则下,寻求最优的超额损失再保险和投资策略。应用随机控制理论,首先分别建立了违约后情况和违约前情况的鲁棒 Hamilton-Jacobi-Bellman (HJB) 方程。然后得到了最优控制策略的显式表达式,并给出了验证定理。最后,给出了一些数值例子来说明我们的结果。

京公网安备 11010802027423号

京公网安备 11010802027423号