当前位置:

X-MOL 学术

›

WIREs Energy Environ.

›

论文详情

Our official English website, www.x-mol.net, welcomes your feedback! (Note: you will need to create a separate account there.)

Risk mitigation in the electricity market driven by new renewable energy sources

Wiley Interdisciplinary Reviews: Energy and Environment ( IF 6.1 ) Pub Date : 2019-08-22 , DOI: 10.1002/wene.362 Nikola Krečar 1 , Andrej F. Gubina 1

Wiley Interdisciplinary Reviews: Energy and Environment ( IF 6.1 ) Pub Date : 2019-08-22 , DOI: 10.1002/wene.362 Nikola Krečar 1 , Andrej F. Gubina 1

Affiliation

|

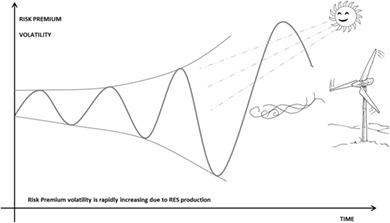

An important indicator of supply and demand uncertainty on electricity markets is risk premium (RP), an integral part of electricity price. The level of RP is describing the risk the market actors expect in the future due to the market uncertainties. With the electricity market price behavior rapidly changing, the rising market supply uncertainty is increasing the volatility of RP. To better understand this behavior, power market participants need new models that will efficiently use the information available in the processes driving the electricity price and RP and to explain the influence of RES uncertainties on the future RP and electricity prices. A decade ago, researchers investigating RP focused primarily on the uncertainties arising from consumption forecast and generation outages. RES share in generation mix was small and its influence on uncertainty was negligible, leading to much lower volatilities of RP than today. With the increasing influence of RES, typically exhibiting variability on a sub‐hourly level, traditional models using daily electricity price to calculate RP were becoming inadequate. In this dynamic period of electricity market transformation, this paper highlights the importance of RP signals to market actors. A stochastic method for RP calculation is discussed with the associated RP model, driven by the intraday dynamics. An example of the RP signal is presented on historical price data from the German electricity market, highlighting uncertainty pattern developed over the years. With such an approach, the market actors can adjust their trading strategies thus mitigating their market risk exposure.

中文翻译:

由新的可再生能源驱动的电力市场中的风险缓解

电力市场供需不确定性的重要指标是风险溢价(RP),它是电价不可或缺的一部分。RP级别描述的是市场参与者由于市场不确定性而在未来所预期的风险。随着电力市场价格行为的快速变化,不断增加的市场供应不确定性加剧了RP的波动性。为了更好地理解这种行为,电力市场参与者需要新的模型,这些模型将有效地利用驱动电价和RP的过程中可用的信息,并解释RES不确定性对未来RP和电价的影响。十年前,对RP进行研究的研究人员主要集中在消费预测和发电中断所带来的不确定性上。RES在发电量中所占的份额很小,并且对不确定性的影响可以忽略不计,从而导致RP的波动性比今天低得多。随着RES的影响越来越大,通常表现为每小时小时以下的可变性,使用每日电价来计算RP的传统模型变得不足。在这个充满活力的电力市场转型时期,本文着重强调了RP信号对市场参与者的重要性。在日内动态的驱动下,结合相关的RP模型讨论了一种随机计算RP的方法。在德国电力市场的历史价格数据上显示了RP信号的一个示例,突出显示了多年来发展起来的不确定性模式。通过这种方法,市场参与者可以调整其交易策略,从而减轻其市场风险敞口。

更新日期:2019-08-22

中文翻译:

由新的可再生能源驱动的电力市场中的风险缓解

电力市场供需不确定性的重要指标是风险溢价(RP),它是电价不可或缺的一部分。RP级别描述的是市场参与者由于市场不确定性而在未来所预期的风险。随着电力市场价格行为的快速变化,不断增加的市场供应不确定性加剧了RP的波动性。为了更好地理解这种行为,电力市场参与者需要新的模型,这些模型将有效地利用驱动电价和RP的过程中可用的信息,并解释RES不确定性对未来RP和电价的影响。十年前,对RP进行研究的研究人员主要集中在消费预测和发电中断所带来的不确定性上。RES在发电量中所占的份额很小,并且对不确定性的影响可以忽略不计,从而导致RP的波动性比今天低得多。随着RES的影响越来越大,通常表现为每小时小时以下的可变性,使用每日电价来计算RP的传统模型变得不足。在这个充满活力的电力市场转型时期,本文着重强调了RP信号对市场参与者的重要性。在日内动态的驱动下,结合相关的RP模型讨论了一种随机计算RP的方法。在德国电力市场的历史价格数据上显示了RP信号的一个示例,突出显示了多年来发展起来的不确定性模式。通过这种方法,市场参与者可以调整其交易策略,从而减轻其市场风险敞口。

京公网安备 11010802027423号

京公网安备 11010802027423号