Energy Economics ( IF 13.6 ) Pub Date : 2023-03-05 , DOI: 10.1016/j.eneco.2023.106603 Lu-Tao Zhao , Zhi-Yi Zheng , Yi-Ming Wei

|

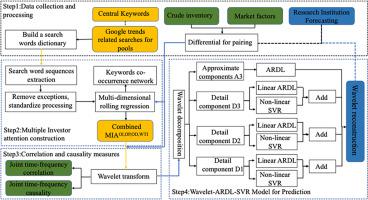

The current crude oil inventory is still at a historical high, and the destocking of crude oil has become a long-term pattern. In the context that changes in crude oil inventories have attracted much attention from the market, a hybrid Wavelet-ARDL-SVR (WAS) model is proposed to predict the change in the oil inventory.1 First, this paper constructs a new indicator to express the correlation between investor behavior and inventory through Google Trends. Then, aiming at the problem that the relationships between inventory and influencing factors are not significant in the time domain, the application of wavelet finds the driving factors and frequency characteristics of inventory changes. We innovatively find that the buffering effect of inventory is reflected in the long-term, while the speculation effect is mainly superimposed in the short-term, especially the speculation on the supply side is more likely to cause market risks. Finally, the empirical results show that the proposed method provides better prediction accuracy. Especially, it improves sign consistency by 19% compared to the predictions of the research institution.

中文翻译:

使用 Google 趋势预测石油库存变化:混合小波分解器和 ARDL-SVR 集成模型

当前原油库存仍处于历史高位,原油去库存成为长期格局。在原油库存变化备受市场关注的背景下,提出了一种混合Wavelet-ARDL-SVR(WAS)模型来预测原油库存变化。1个首先,本文通过谷歌趋势构建了一个新的指标来表达投资者行为与库存之间的相关性。然后,针对库存与影响因素在时域上关系不显着的问题,应用小波寻找库存变化的驱动因素和频率特征。我们创新性地发现,库存的缓冲作用体现在长期,而投机效应主要叠加在短期,尤其是供给端的投机更容易引发市场风险。最后,实证结果表明,所提出的方法提供了更好的预测精度。特别是,与研究机构的预测相比,它提高了 19% 的符号一致性。

京公网安备 11010802027423号

京公网安备 11010802027423号