The European Physical Journal B ( IF 1.6 ) Pub Date : 2022-08-27 , DOI: 10.1140/epjb/s10051-022-00402-0 Anantya Bhatnagar 1 , Dimitri D Vvedensky 1

|

Abstract

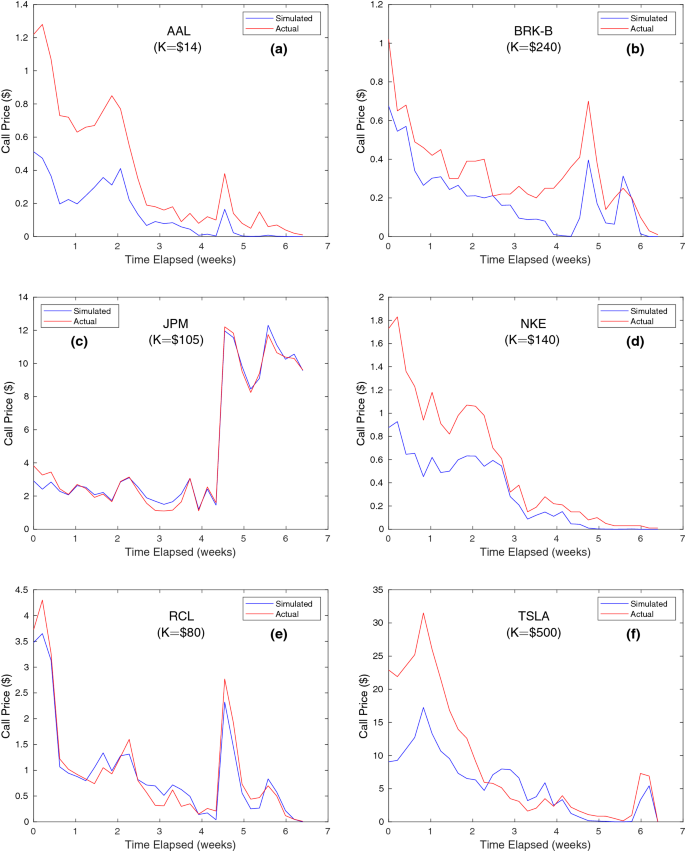

The limitations of the classical Black–Scholes model are examined by comparing calculated and actual historical prices of European call options on stocks from several sectors of the S &P 500. Persistent differences between the two prices point to an expanded model proposed by Segal and Segal (PNAS 95:4072–4075, 1988) in which information not simultaneously observable or actionable with public information can be represented by an additional pseudo-Wiener process. A real linear combination of the original and added processes leads to a commutation relation analogous to that between a boson field and its canonical momentum in quantum field theory. The resulting pricing formula for a European call option replaces the classical volatility with the norm of a complex quantity, whose imaginary part is shown to compensate for the disparity between prices obtained from the classical Black–Scholes model and actual prices of the test call options. This provides market evidence for the influence of a non-classical process on the price of a security based on non-commuting operators.

Graphic Abstract

中文翻译:

扩展 Black-Scholes 模型中的量子效应

摘要

通过比较标准普尔 500 指数多个板块股票的欧式看涨期权的计算价格和实际历史价格来检验经典 Black-Scholes 模型的局限性。两个价格之间的持续差异指向 Segal 和 Segal 提出的扩展模型( PNAS 95:4072–4075, 1988),其中不能与公共信息同时观察或可操作的信息可以由附加的伪维纳过程表示。原始过程和附加过程的真正线性组合导致了类似于量子场论中玻色子场与其规范动量之间的对等关系。由此产生的欧式看涨期权定价公式将经典波动率替换为复数规范,其虚部用于补偿从经典 Black-Scholes 模型获得的价格与测试看涨期权的实际价格之间的差异。这为非经典过程对基于非通勤运营商的证券价格的影响提供了市场证据。

京公网安备 11010802027423号

京公网安备 11010802027423号