当前位置:

X-MOL 学术

›

Methodol. Comput. Appl. Probab.

›

论文详情

Our official English website, www.x-mol.net, welcomes your

feedback! (Note: you will need to create a separate account there.)

Moments of the Ruin Time in a Lévy Risk Model

Methodology and Computing in Applied Probability ( IF 1.0 ) Pub Date : 2022-07-30 , DOI: 10.1007/s11009-022-09967-w Philipp Lukas Strietzel , Anita Behme

中文翻译:

Lévy 风险模型中的毁灭时刻

更新日期:2022-07-30

Methodology and Computing in Applied Probability ( IF 1.0 ) Pub Date : 2022-07-30 , DOI: 10.1007/s11009-022-09967-w Philipp Lukas Strietzel , Anita Behme

|

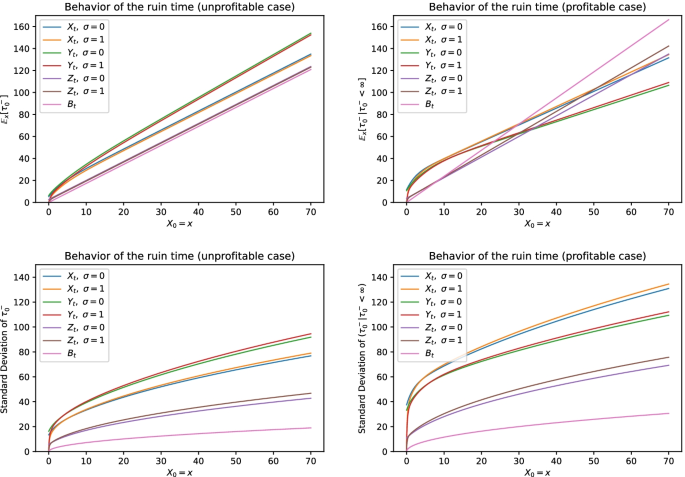

We derive formulas for the moments of the ruin time in a Lévy risk model and use these to determine the asymptotic behavior of the moments of the ruin time as the initial capital tends to infinity. In the special case of the perturbed Cramér-Lundberg model with phase-type or even exponentially distributed claims, we explicitly compute the first two moments of the ruin time. All our considerations distinguish between the profitable and the unprofitable setting.

中文翻译:

Lévy 风险模型中的毁灭时刻

我们在 Lévy 风险模型中推导出破产时刻的公式,并使用这些公式来确定破产时刻的渐近行为,因为初始资本趋于无穷大。在具有相位类型甚至指数分布声明的扰动 Cramér-Lundberg 模型的特殊情况下,我们明确计算了破产时间的前两个时刻。我们所有的考虑都区分了有利可图和无利可图的环境。

京公网安备 11010802027423号

京公网安备 11010802027423号