Methodology and Computing in Applied Probability ( IF 1.0 ) Pub Date : 2022-07-21 , DOI: 10.1007/s11009-022-09970-1 Erik Hintz , Marius Hofert , Christiane Lemieux , Yoshihiro Taniguchi

|

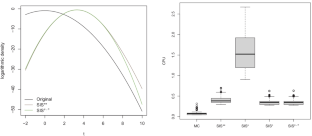

In many stochastic problems, the output of interest depends on an input random vector mainly through a single random variable (or index) via an appropriate univariate transformation of the input. We exploit this feature by proposing an importance sampling method that makes rare events more likely by changing the distribution of the chosen index. Further variance reduction is guaranteed by combining this single-index importance sampling approach with stratified sampling. The dimension-reduction effect of single-index importance sampling also enhances the effectiveness of quasi-Monte Carlo methods. The proposed method applies to a wide range of financial or risk management problems. We demonstrate its efficiency for estimating large loss probabilities of a credit portfolio under a normal and t-copula model and show that our method outperforms the current standard for these problems.

中文翻译:

带分层的单指标重要性抽样

在许多随机问题中,感兴趣的输出取决于输入随机向量,主要通过单个随机变量(或索引)通过输入的适当单变量变换。我们通过提出一种重要性采样方法来利用此功能,该方法通过更改所选索引的分布使罕见事件更有可能发生。通过将这种单指标重要性抽样方法与分层抽样相结合,可以进一步减少方差。单指标重要性采样的降维效果也增强了准蒙特卡罗方法的有效性。建议的方法适用于广泛的财务或风险管理问题。我们证明了它在正常和t条件下估计信用组合的大损失概率的效率-copula 模型,并表明我们的方法优于这些问题的当前标准。

京公网安备 11010802027423号

京公网安备 11010802027423号