Metrika ( IF 0.9 ) Pub Date : 2022-07-16 , DOI: 10.1007/s00184-022-00875-0 Holger Dette , Vasyl Golosnoy , Janosch Kellermann

|

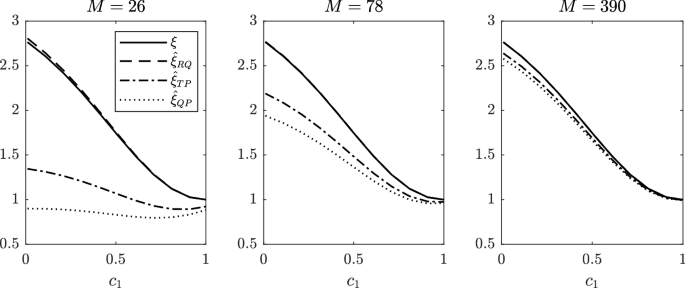

We focus on estimating daily integrated volatility (IV) by realized measures based on intraday returns following a discrete-time stochastic model with a pronounced intraday periodicity (IP). We demonstrate that neglecting the IP-impact on realized estimators may lead to invalid statistical inference concerning IV for a common finite number of intraday returns. For a given IP functional form, we analytically derive robust IP-correction factors for realized measures of IV as well as their asymptotic distributions. We show both in Monte Carlo simulations and empirically that the proposed bias corrections are the robust way to account for IP by computing realized estimators.

中文翻译:

日内周期性对已实现波动率指标的影响

我们专注于根据具有明显日内周期性 (IP) 的离散时间随机模型,通过基于日内回报的已实现度量来估计每日综合波动率 ( IV )。我们证明,忽略 IP 对已实现估计量的影响可能会导致针对常见有限数量的日内收益的IV的无效统计推断。对于给定的 IP 函数形式,我们通过分析推导出用于实现IV测量的稳健 IP 校正因子及其渐近分布。我们在蒙特卡洛模拟和经验上都表明,所提出的偏差校正是通过计算已实现的估计量来解释 IP 的稳健方法。

京公网安备 11010802027423号

京公网安备 11010802027423号