Metrika ( IF 0.7 ) Pub Date : 2022-06-18 , DOI: 10.1007/s00184-022-00869-y Chang-Sheng Liu , Han-Ying Liang

|

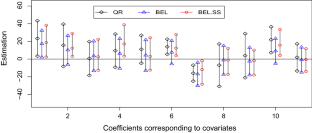

In this paper, we focus on partially linear varying coefficient quantile regression with observations missing at random, which allows the responses or responses and covariates simultaneously missing. By means of empirical likelihood method, we construct posterior distributions of the parameter in the model, and investigate their large sample properties under fixed prior. Meanwhile, we use a Bayesian hierarchical model based on empirical likelihood, spike and slab Gaussian priors to discuss variable selection. By using MCMC algorithm, finite sample performance of the proposed methods is investigated via simulations, and real data analysis is discussed too.

中文翻译:

缺少观察的分位数回归的贝叶斯经验似然

在本文中,我们专注于部分线性变系数分位数回归,其中观察值随机缺失,这使得响应或响应和协变量同时缺失。通过经验似然法,我们构造了模型中参数的后验分布,并研究了它们在固定先验条件下的大样本特性。同时,我们使用基于经验似然、尖峰和平板高斯先验的贝叶斯层次模型来讨论变量选择。通过使用MCMC算法,通过仿真研究了所提方法的有限样本性能,并讨论了真实数据分析。

京公网安备 11010802027423号

京公网安备 11010802027423号