Statistical Papers ( IF 1.3 ) Pub Date : 2022-05-20 , DOI: 10.1007/s00362-022-01320-0 Terezinha K. A. Ribeiro , Silvia L. P. Ferrari

|

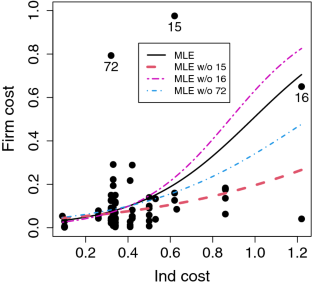

Beta regression models are widely used for modeling continuous data limited to the unit interval, such as proportions, fractions, and rates. The inference for the parameters of beta regression models is commonly based on maximum likelihood estimation. However, it is known to be sensitive to discrepant observations. In some cases, one atypical data point can lead to severe bias and erroneous conclusions about the features of interest. In this work, we develop a robust estimation procedure for beta regression models based on the maximization of a reparameterized L\(_q\)-likelihood. The new estimator offers a trade-off between robustness and efficiency through a tuning constant. To select the optimal value of the tuning constant, we propose a data-driven method which ensures full efficiency in the absence of outliers. We also improve on an alternative robust estimator by applying our data-driven method to select its optimum tuning constant. Monte Carlo simulations suggest marked robustness of the two robust estimators with little loss of efficiency when the proposed selection scheme for the tuning constant is employed. Applications to three datasets are presented and discussed. As a by-product of the proposed methodology, residual diagnostic plots based on robust fits highlight outliers that would be masked under maximum likelihood estimation.

中文翻译:

通过最大 L $$_q$$ q -likelihood 在 beta 回归中进行稳健估计

Beta 回归模型广泛用于对受限于单位区间的连续数据进行建模,例如比例、分数和比率。β回归模型的参数推断通常基于最大似然估计。然而,众所周知,它对不一致的观察结果很敏感。在某些情况下,一个非典型数据点可能会导致严重的偏差和对感兴趣特征的错误结论。在这项工作中,我们开发了一个基于重新参数化 L \(_q\)最大化的 beta 回归模型的稳健估计程序。-可能性。新的估计器通过调整常数在鲁棒性和效率之间进行权衡。为了选择调整常数的最佳值,我们提出了一种数据驱动的方法,该方法可确保在没有异常值的情况下完全有效。我们还通过应用我们的数据驱动方法来选择其最佳调谐常数来改进替代的稳健估计器。蒙特卡罗模拟表明,当采用所提出的调谐常数选择方案时,两个稳健估计器具有显着的稳健性,几乎没有效率损失。介绍并讨论了对三个数据集的应用。作为所提出方法的副产品,基于稳健拟合的残差诊断图突出显示在最大似然估计下会被掩盖的异常值。

京公网安备 11010802027423号

京公网安备 11010802027423号