Methodology and Computing in Applied Probability ( IF 1.0 ) Pub Date : 2022-05-14 , DOI: 10.1007/s11009-022-09959-w Pavel V. Gapeev , Peter M. Kort , Maria N. Lavrutich , Jacco J. J. Thijssen

|

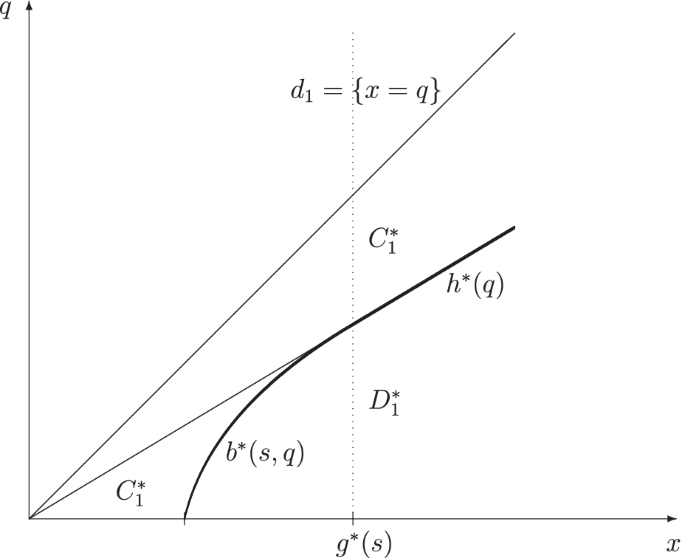

We present closed-form solutions to some double optimal stopping problems with payoffs representing linear functions of the running maxima and minima of a geometric Brownian motion. It is shown that the optimal stopping times are th first times at which the underlying process reaches some lower or upper stochastic boundaries depending on the current values of its running maximum or minimum. The proof is based on the reduction of the original double optimal stopping problems to sequences of single optimal stopping problems for the resulting three-dimensional continuous Markov process. The latter problems are solved as the equivalent free-boundary problems by means of the smooth-fit and normal-reflection conditions for the value functions at the optimal stopping boundaries and the edges of the three-dimensional state space. We show that the optimal stopping boundaries are determined as the extremal solutions of the associated first-order nonlinear ordinary differential equations. The obtained results are related to the valuation of perpetual real double lookback options with floating sunk costs in the Black-Merton-Scholes model.

中文翻译:

几何布朗运动最大值和最小值的最优双停问题

我们提出了一些双重最优停止问题的封闭形式解决方案,其收益表示几何布朗运动的运行最大值和最小值的线性函数。结果表明,最佳停止时间是基础过程根据其运行最大值或最小值的当前值达到某些较低或较高随机边界的第一次时间。证明是基于将原始双最优停止问题简化为生成的 3 维连续马尔可夫过程的单最优停止问题序列。后一个问题通过最优停止边界和三维状态空间边缘的值函数的平滑拟合和法向反射条件作为等效自由边界问题求解。我们表明,最佳停止边界被确定为相关的一阶非线性常微分方程的极值解。获得的结果与 Black-Merton-Scholes 模型中浮动沉没成本的永久真实双重回溯期权的估值有关。

京公网安备 11010802027423号

京公网安备 11010802027423号