Methodology and Computing in Applied Probability ( IF 1.0 ) Pub Date : 2022-03-30 , DOI: 10.1007/s11009-022-09928-3 Anna B. Zaremba 1 , Gareth W. Peters 2

|

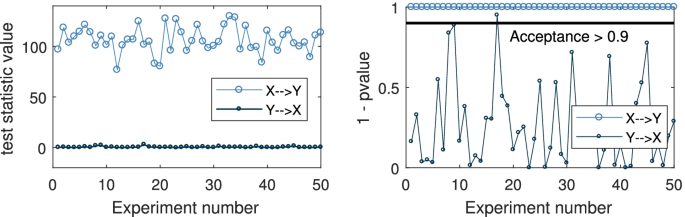

The ability to test for statistical causality in linear and nonlinear contexts, in stationary or non-stationary settings, and to identify whether statistical causality influences trend of volatility forms a particularly important class of problems to explore in multi-modal and multivariate processes. In this paper, we develop novel testing frameworks for statistical causality in general classes of multivariate nonlinear time series models. Our framework accommodates flexible features where causality may be present in either: trend, volatility or both structural components of the general multivariate Markov processes under study. In addition, we accommodate the added possibilities of flexible structural features such as long memory and persistence in the multivariate processes when applying our semi-parametric approach to causality detection. We design a calibration procedure and formal testing procedure to detect these relationships through classes of Gaussian process models. We provide a generic framework which can be applied to a wide range of problems, including partially observed generalised diffusions or general multivariate linear or nonlinear time series models. We demonstrate several illustrative examples of features that are easily testable under our framework to study the properties of the inference procedure developed including the power of the test, sensitivity and robustness. We then illustrate our method on an interesting real data example from commodity modelling.

中文翻译:

基于高斯过程模型的多元非线性时间序列的统计因果关系

在线性和非线性环境中、在平稳或非平稳环境中检验统计因果关系以及确定统计因果关系是否影响波动趋势的能力构成了在多模态和多变量过程中探索的一类特别重要的问题。在本文中,我们为一般类别的多元非线性时间序列模型中的统计因果关系开发了新的测试框架。我们的框架适应灵活的特征,其中因果关系可能存在于:正在研究的一般多元马尔可夫过程的趋势、波动性或两个结构组成部分。此外,当将我们的半参数方法应用于因果关系检测时,我们在多变量过程中适应了灵活结构特征的附加可能性,例如长记忆和持久性。我们设计了一个校准程序和正式的测试程序,通过高斯过程模型类来检测这些关系。我们提供了一个通用框架,可以应用于广泛的问题,包括部分观察到的广义扩散或一般多元线性或非线性时间序列模型。我们展示了几个在我们的框架下易于测试的特性示例,以研究开发的推理过程的属性,包括测试的能力、灵敏度和鲁棒性。然后,我们用一个来自商品建模的有趣真实数据示例来说明我们的方法。我们提供了一个通用框架,可以应用于广泛的问题,包括部分观察到的广义扩散或一般多元线性或非线性时间序列模型。我们展示了几个在我们的框架下易于测试的特性示例,以研究开发的推理过程的属性,包括测试的能力、灵敏度和鲁棒性。然后,我们用一个来自商品建模的有趣真实数据示例来说明我们的方法。我们提供了一个通用框架,可以应用于广泛的问题,包括部分观察到的广义扩散或一般多元线性或非线性时间序列模型。我们展示了几个在我们的框架下易于测试的特性示例,以研究开发的推理过程的属性,包括测试的能力、灵敏度和鲁棒性。然后,我们用一个来自商品建模的有趣真实数据示例来说明我们的方法。

京公网安备 11010802027423号

京公网安备 11010802027423号