Research in International Business and Finance ( IF 6.3 ) Pub Date : 2021-05-05 , DOI: 10.1016/j.ribaf.2021.101424 Afees A Salisu 1, 2 , Xuan Vinh Vo 2, 3 , Brian Lucey 4, 5

|

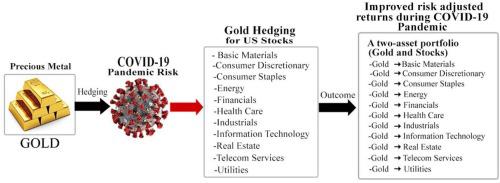

In this study, we examine the hedging relationship between gold and US sectoral stocks during the COVID-19 pandemic. We employ a multivariate volatility framework, which accounts for salient features of the series in the computation of optimal weights and optimal hedging ratios. We find evidence of hedging effectiveness between gold and sectoral stocks, albeit with lower performance, during the pandemic. Overall, including gold in a stock portfolio could provide a valuable asset class that can improve the risk-adjusted performance of stocks during the COVID-19 pandemic. In addition, we find that the estimated portfolio weights and hedge ratios are sensitive to structural breaks, and ignoring the breaks can lead to overestimation of the hedging effectiveness of gold for US sectoral stocks. Since the analysis involves sectoral stock data, we believe that any investor in the US stock market that seeks to maximize risk-adjusted returns is likely to find the results useful when making investment decisions during the pandemic.

中文翻译:

COVID-19 大流行期间的黄金和美国板块股票

在这项研究中,我们研究了 COVID-19 大流行期间黄金和美国板块股票之间的对冲关系。我们采用多元波动率框架,该框架在计算最优权重和最优对冲比率时考虑了该序列的显着特征。我们发现了黄金和行业股票之间对冲有效性的证据,尽管在大流行期间表现较低。总体而言,将黄金纳入股票投资组合可以提供有价值的资产类别,可以改善股票在 COVID-19 大流行期间的风险调整后表现。此外,我们发现估计的投资组合权重和对冲比率对结构性突破很敏感,忽略结构性突破可能导致高估黄金对美国板块股票的对冲有效性。由于分析涉及行业股票数据,我们相信,美国股市中任何寻求风险调整回报最大化的投资者在疫情期间做出投资决策时都可能会发现这些结果很有用。

京公网安备 11010802027423号

京公网安备 11010802027423号