Resources Policy Pub Date : 2021-04-08 , DOI: 10.1016/j.resourpol.2021.102079 Qian Ding , Jianbai Huang , Hongwei Zhang

|

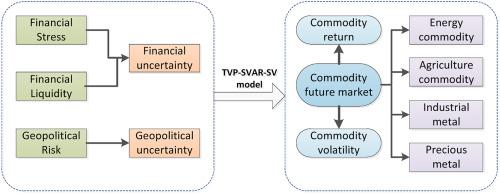

We explore the time-varying effects of financial and geopolitical uncertainties on commodity markets using a time-varying parameter structural vector autoregression with stochastic volatility (TVP-SVAR-SV) model. Our results indicate that the effects of geopolitical and financial uncertainties on commodity dynamics are concentrated in the short-term, and commodity volatility is more affected than returns. The volatility of commodity futures responds differently to different types of financial uncertainty shocks, and the uncertainty shocks caused by financial stress have produced relatively large effects, especially since the global financial crisis. Furthermore, our findings contradict traditional wisdom, as we observe that the uncertainty shocks caused by financial liquidity lead to increased commodity returns only in the short term. There are obvious heterogeneity responses of commodity futures in different sectors to uncertainty shocks. Energy and industrial metals are more affected than other commodities. Our findings are an important reference for decision makers and investors.

中文翻译:

金融和地缘政治不确定性对商品市场动态的时变影响:TVP-SVAR-SV分析

我们使用具有随机波动率的时变参数结构矢量自回归(TVP-SVAR-SV)模型来探索金融和地缘政治不确定性对商品市场的时变影响。我们的结果表明,地缘政治和金融不确定性对商品动态的影响集中在短期内,商品波动比收益受到的影响更大。大宗商品期货的波动对不同类型的金融不确定性冲击的反应不同,而金融压力引起的不确定性冲击产生了相对较大的影响,特别是自全球金融危机以来。此外,我们的发现与传统观点相悖,因为我们观察到,由金融流动性引起的不确定性冲击仅在短期内导致商品收益增加。不同部门的商品期货对不确定性冲击有明显的异质性响应。能源和工业金属比其他商品受到的影响更大。我们的发现为决策者和投资者提供了重要参考。

京公网安备 11010802027423号

京公网安备 11010802027423号