Research in International Business and Finance ( IF 6.3 ) Pub Date : 2021-01-11 , DOI: 10.1016/j.ribaf.2021.101384 Burak Pirgaip , Hasan Murat Ertuğrul , Talat Ulussever

|

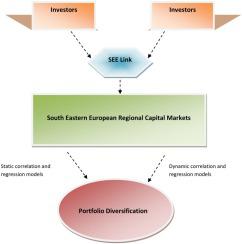

A remarkable process of financial integration has taken place throughout the world capital markets over the last decades. In line with this integration process, the effect of financial integration locally and/or globally has been one of the contemporary topics of interest to academics, practitioners as well as policy makers. In this study, we investigate the availability of portfolio diversification benefits after the initiation of the South Eastern Europe Link (the SEE Link) trading platform in 2016 as a connecting hub for stock markets in the South Eastern European region. Our empirical methodology is primarily based on various static and dynamic correlation (Dynamic Conditional Correlation-GARCH) and regression (Autoregressive Distributed Lag, Fully Modified Ordinary Least Squares, Dynamic Ordinary Least Squares, Markov Switching Regression Model and Kalman Filter Model) analyses. We employ our methods for a daily frequency stock exchange (namely, the Zagreb Stock Exchange and Bulgarian Stock Exchange) return data between January 4, 2005 and December 30, 2019. The findings reveal that the two stock exchanges have a significantly decreasing pattern of correlation and regression relationship over the sample period implying the existence of diversification opportunities in the SEE Link markets.

中文翻译:

集成市场中的投资组合多样化是否可能?来自东南欧的证据

在过去的几十年中,整个世界资本市场都发生了惊人的金融整合过程。在这种整合过程中,本地和/或全球金融整合的影响已成为学者,从业者以及政策制定者关注的当代主题之一。在本研究中,我们调查了东南欧链接(SEE Link)交易平台于2016年启动后作为东南欧地区股票市场的连接枢纽后投资组合多元化收益的可利用性。我们的经验方法主要基于各种静态和动态相关性(动态条件相关GARCH)和回归(自回归分布式滞后,完全修正的普通最小二乘,动态普通最小二乘,马尔可夫切换回归模型和卡尔曼滤波器模型)分析。我们将我们的方法用于2005年1月4日至2019年12月30日之间的每日频率证券交易所(即Zagreb证券交易所和保加利亚证券交易所)的收益数据。研究结果表明,这两个证券交易所的关联度显着下降样本期内的回归和回归关系表明,SEE Link市场存在多元化机会。

京公网安备 11010802027423号

京公网安备 11010802027423号