Physica A: Statistical Mechanics and its Applications ( IF 2.8 ) Pub Date : 2021-01-04 , DOI: 10.1016/j.physa.2020.125728 Yong Shi , Bo Li , Guangle Du , Wei Dai

|

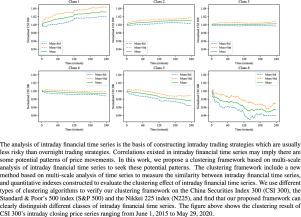

The analysis of intraday financial time series is the basis of constructing intraday trading strategies which are usually less risky than overnight trading strategies. Correlations existed in intraday financial series may imply there are some potential patterns of price movements. In this work, we propose a clustering framework based on multi-scale analysis of intraday financial time series to seek these potential patterns. The clustering framework include a new method based on multi-scale analysis of time series to measure the similarity between intraday financial time series, and quantitative indexes constructed to evaluate the clustering effect of intraday financial time series. We use different types of clustering algorithms to verify our clustering framework on the China Securities Index 300 (CSI 300), the Standard & Poor’s 500 index (S&P 500) and the Nikkei 225 index (N225), and find that our proposed framework can clearly distinguish different classes of intraday financial time series.

京公网安备 11010802027423号

京公网安备 11010802027423号