The Japanese Economic Review ( IF 1.5 ) Pub Date : 2020-07-04 , DOI: 10.1007/s42973-020-00051-x Dimitrios Kartsonakis-Mademlis , Nikolaos Dritsakis

|

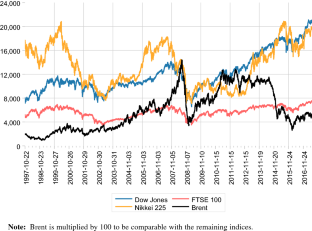

This research shows that accounting for structural breaks within the asymmetric GJR-GARCH model reduces volatility persistence in stock and oil returns. More importantly, we ascertain that good news has less impact on current volatility if sudden changes are accounted for, while bad news has more impact in all cases with an exception of Nikkei225. Our findings are in line with previous studies and highlight that it is plausible to include structural breaks in asymmetric GARCH models to model volatility dynamics more precisely. The results of the univariate analysis provide evidence of bi-directional volatility spillover effects between the Japanese stock market and the rest of the markets, independently of the model choice. Thus, neglecting structural breaks in variance may lead to different results but not to the extent of distortion of the direction of volatility transmission effects. The latter finding does not hold true under the multivariate context highlighting the power difference between the CCF approach and the BEKK-GARCH models. Finally, we ascertain that data frequency may also affect the direction of the volatility spillovers among the markets.

中文翻译:

结构性突破下日本股市的不对称波动传导

这项研究表明,考虑到不对称 GJR-GARCH 模型中的结构性中断,会降低股票和石油收益的波动持续性。更重要的是,我们确定如果考虑到突然的变化,好消息对当前波动性的影响较小,而坏消息在所有情况下都具有更大的影响,但 Nikkei225 除外。我们的研究结果与之前的研究一致,并强调在不对称 GARCH 模型中包含结构性中断以更精确地模拟波动率动态是合理的。单变量分析的结果提供了日本股市与其他市场之间双向波动溢出效应的证据,与模型选择无关。因此,忽略方差的结构性中断可能会导致不同的结果,但不会导致波动率传递效应方向的扭曲程度。在强调 CCF 方法和 BEKK-GARCH 模型之间的功效差异的多元背景下,后一种发现并不成立。最后,我们确定数据频率也可能影响市场之间波动溢出的方向。

京公网安备 11010802027423号

京公网安备 11010802027423号