Frontiers of Business Research in China ( IF 1.3 ) Pub Date : 2020-03-25 , DOI: 10.1186/s11782-020-00076-4 Haican Diao , Guoshan Liu , Zhuangming Zhu

|

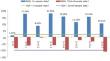

In recent years, with strict domestic financial supervision and other policy-oriented factors, some products are becoming increasingly restricted, including nonstandard products, bank-guaranteed wealth management products, and other products that can provide investors with a more stable income. Pairs trading, a type of stable strategy that has proved efficient in many financial markets worldwide, has become the focus of investors. Based on the traditional Gatev–Goetzmann–Rouwenhorst (GGR, Gatev et al., 2006) strategy, this paper proposes a stock-matching strategy based on bi-objective quadratic programming with quadratic constraints (BQQ) model. Under the condition of ensuring a long-term equilibrium between paired-stock prices, the volatility of stock spreads is increased as much as possible, improving the profitability of the strategy. To verify the effectiveness of the strategy, we use the natural logs of the daily stock market indices in Shanghai. The GGR model and the BQQ model proposed in this paper are back-tested and compared. The results show that the BQQ model can achieve a higher rate of returns.

中文翻译:

基于双目标优化的股票撮合交易策略研究

近年来,受国内金融监管严格等政策导向因素的影响,一些产品受到越来越多的限制,包括非标产品、银行保本理财产品等能够为投资者提供更稳定收益的产品。配对交易作为一种在全球许多金融市场上被证明有效的稳定策略,已成为投资者关注的焦点。在传统的Gatev-Goetzmann-Rouwenhorst(GGR,Gatev et al.,2006)策略的基础上,本文提出了一种基于二次约束双目标二次规划(BQQ)模型的股票匹配策略。在保证配对股票价格长期均衡的情况下,尽可能增大股票价差的波动性,提高策略的盈利能力。为了验证该策略的有效性,我们使用上海每日股市指数的自然对数。对本文提出的GGR模型和BQQ模型进行了回测和比较。结果表明BQQ模型可以获得较高的回报率。

京公网安备 11010802027423号

京公网安备 11010802027423号