当前位置:

X-MOL 学术

›

International Review of Financial Analysis

›

论文详情

Our official English website, www.x-mol.net, welcomes your feedback! (Note: you will need to create a separate account there.)

Bitcoin price volatility transmission between spot and futures markets

International Review of Financial Analysis ( IF 8.235 ) Pub Date : 2024-03-29 , DOI: 10.1016/j.irfa.2024.103251 George N. Apostolakis

International Review of Financial Analysis ( IF 8.235 ) Pub Date : 2024-03-29 , DOI: 10.1016/j.irfa.2024.103251 George N. Apostolakis

|

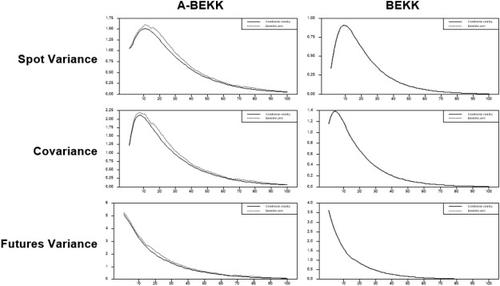

In this paper, the volatility transmission between the two bitcoin markets, namely, the spot and futures markets is examined. We use the daily series over a sampling period spanning from December 2017 to September 2022. We focus on several events that have spread severe risk throughout cryptomarkets, such as the COVID-19 pandemic of 2020, the governmental announcements and environmental concerns of 2021, and the crypto-winter cases of 2022. We calculate the symmetric and asymmetric volatility impulse responses (VIRFs) using a VEC-BEKK-MGARCH model and the Hafner and Herwartz (2006) framework. The results of the VIRF analysis demonstrate the existence of asymmetric responses between the two markets, with the shock of the COVID-19 pandemic exerting a greater impact on the variance of the futures market than on that of the spot market. Additionally, we employ the connectedness approach of Diebold and Yilmaz (2012, 2014) as modified by Gabauer (2020) and apply a DCC-GARCH model to examine the volatility spillovers across the two markets. Our results suggest that the bitcoin spot market is the dominant transmitter of volatility shocks to the futures market.

中文翻译:

比特币价格波动在现货和期货市场之间的传递

本文研究了两个比特币市场(即现货市场和期货市场)之间的波动性传递。我们在 2017 年 12 月至 2022 年 9 月的采样期间使用每日系列。我们关注在整个加密市场传播严重风险的几个事件,例如 2020 年的 COVID-19 大流行、2021 年的政府公告和环境问题,以及2022 年的加密冬季情况。我们使用 VEC-BEKK-MGARCH 模型以及 Hafner 和 Herwartz (2006) 框架计算对称和非对称波动性脉冲响应 (VIRF)。 VIRF分析结果表明,两个市场之间存在不对称反应,COVID-19大流行的冲击对期货市场的方差影响大于对现货市场的影响。此外,我们采用 Diebold 和 Yilmaz(2012,2014)经 Gabauer(2020)修改的连通性方法,并应用 DCC-GARCH 模型来检查两个市场的波动溢出效应。我们的研究结果表明,比特币现货市场是波动性冲击向期货市场的主要传导者。

更新日期:2024-03-29

中文翻译:

比特币价格波动在现货和期货市场之间的传递

本文研究了两个比特币市场(即现货市场和期货市场)之间的波动性传递。我们在 2017 年 12 月至 2022 年 9 月的采样期间使用每日系列。我们关注在整个加密市场传播严重风险的几个事件,例如 2020 年的 COVID-19 大流行、2021 年的政府公告和环境问题,以及2022 年的加密冬季情况。我们使用 VEC-BEKK-MGARCH 模型以及 Hafner 和 Herwartz (2006) 框架计算对称和非对称波动性脉冲响应 (VIRF)。 VIRF分析结果表明,两个市场之间存在不对称反应,COVID-19大流行的冲击对期货市场的方差影响大于对现货市场的影响。此外,我们采用 Diebold 和 Yilmaz(2012,2014)经 Gabauer(2020)修改的连通性方法,并应用 DCC-GARCH 模型来检查两个市场的波动溢出效应。我们的研究结果表明,比特币现货市场是波动性冲击向期货市场的主要传导者。

京公网安备 11010802027423号

京公网安备 11010802027423号