Abstract

The article presents the speculative frame method for analysing the real estate market, identifying market tensions, small shocks and price bubbles. The method relies on time and price data series. In the speculative frame method, time is expressed by the horizontal parameter of the frame with a fixed interval, and house price dynamics is denoted by the vertical parameter that changes over time. The frame sequence is analysed to determine the rate of changes in housing prices. The main advantage of this index-based approach is that it diagnoses the real estate market in real time. The method was presented on the example of Polish housing markets and under simulated market conditions. The time series of home prices were analysed in Wrocław (the fourth largest Polish city) during dynamic price increases in 2002–2012, as well as in Warsaw (the Polish capital) in 2016–2018 during a period of market stability. Research limitations were identified, and robustness tests were conducted. The study demonstrated that the speculative frame method can be used as a rapid screening method for analysing a market’s performance based on house price dynamics.

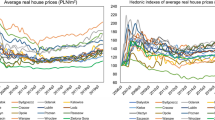

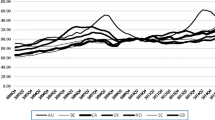

Source: own elaboration

Source: own elaboration

Source: own elaboration, (Own elaboration based on illustration from: https://pl.wikipedia.org/wiki/Plik:POLSKA_mapa_woj_z_powiatami.png (accessed in February 2022) and (accessed in February 2022) and (accessed in February 2022))

Source: own elaboration

Source: own elaboration

Source: own elaboration, Vertical axis—price; horizontal axis—time

Source: own elaboration

Source: own elaboration

Source: own elaboration

Source: own elaboration based on formula (10)

Source: own elaboration based on formula (12)

Source: own elaboration based on formula (12)

Source: own elaboration based on formula (12)

Source: own elaboration based on formula (12)

Source: own elaboration

Source: own elaboration based on formula (12)

Source: own elaboration based on formula (10)

Source: own elaboration based on formula (10)

Source: own elaboration based on formula (12)

Source: own elaboration

Source: own elaboration

Source: own elaboration

Similar content being viewed by others

Data availability

Is not available, I provide only results.

Code availability

Code availability is not available; I provide only methodological framework without software.

Notes

The adopted format relies on an Excel function which converts a date to a serial number and vice versa. A date is recorded as a number to describe a period of time in numerical terms. This approach was used to standardise the data.

https://www.random.org/integers/ (accessed in July 2020).

References

Afsar, A., & Dogan, E. (2018). Analyzing asset of bubbles in the housing market with right-tailed unit root tests: The case of turkey. Journal of Business Economics and Finance, 7(2), 139–147.

Al-Masum, M. A., & Lee, C. L. (2020). Modelling housing prices and market fundamentals: Evidence from the Sydney housing market. International Journal of Housing Markets and Analysis, 12(4), 746–762.

Ardila, D., Sanadgol, D., & Sornette, D. (2018). Out-of-sample forecasting of housing bubble tipping points. Quantitative Finance and Economics, 2(4), 904–930.

Author 1, (2017). Doctoral dissertation …… (We will complete this reference in the final version to ensure a blind review).

Author 1, (2022). The application of the …… (We will complete this reference in the final version to ensure a blind review).

Barańska, A. (2016). The significance of database size in modelling the market of nonresidential premises. Real Estate Management and Valuation, 24(2), 47–56.

Berlemann, M., Freese, J., & Knoth, S. (2019). Dating the start of the US house price bubble: An application of statistical process control. Empirical Economics, 58, 2287–2307.

Black, A., Fraser, P., & Hoesli, M. (2006). House prices, fundamentals and bubbles. Journal of Business Finance and Accounting, 33(9–10), 1535–1555.

Brzezicka, J. (2016). Speculative bubbles and their components on the real estate market – a preliminary analysis. Real Estate Management and Valuation, 24(1), 87–99.

Brzezicka, J. (2020). Typology of housing price bubbles: A literature review. Housing, Theory & Society, 38(3), 320–342.

Brzezicka, J., Gross, M., & Kobylińska, K. (2020). The applicability of the gini coefficient for analyses of real estate prices. World of Real Estate Journal, 1(111), 4–15.

Brzezicka, J., Łaszek, J., Olszewski, K., & Waszczuk, J. (2019). Analysis of the filtering process and the ripple effect on the primary and secondary housing market in Warsaw, Poland. Land Use Policy, 88, 104098.

Brzezicka, J., & Wiśniewski, R. (2014). Price bubble in the real estate market - behavioural aspects. Real Estate Management and Valuation, 22(1), 80–93.

Brzezicka, J., Wisniewski, R., & Figurska, M. (2018). Disequilibrium in the real estate market: Evidence from Poland. Land Use Policy, 78, 515–531.

Cannon, S., Miller, N. G., & Pandher, G. S. (2006). Risk and return in the US housing market: A cross-sectional asset-pricing approach. Real Estate Economics, 34(4), 519–552.

Capozza, D. R., Hendershott, P. H., Mack, C., & Mayer, C. J. (2002). Determinants of real house price dynamics. NBER working paper series, no. 9262.

Case, K. E., & Shiller, R. (1988). The behavior of home buyers in boom and post-boom markets. Working Paper, National Bureau of Economic Research, 2748.

Case, K. E., & Shiller, R. J. (1990). Forecasting prices and excess returns in the housing market. Real Estate Economics, 18(3), 253–273.

Case, K. E., & Shiller, R. J. (2003). Is There a Bubble in the Housing Market? Brookings Papers on Economic Activity, 2, 299–362.

Case, K. E., Shiller, R. J., & Thompson, A. K. (2012). What have they been thinking? Homebuyer behavior in hot and cold markets. Brookings Papers on Economic Activity, 18400, 265–315.

Chan, L. C., Lee, S. K., & Woo, K. Y. (2001). Detecting rational bubbles in the residential housing markets of Hong Kong. Economic Modelling, 18, 61–73.

Clapp, J. M., & Giaccotto, C. (1998). Price indices based on the hedonic repeat-sales method: Application to the housing market. The Journal of Real Estate Finance and Economics, 16(1), 5–26.

Crawford, G., & Fratantoni, M. (2003). Assessing the forecasting performance of regime-switching, ARIMA and GARCH models of house prices. Real Estate Economics, 31, 223–243.

Czerski, J., Gluszak, M., & Zygmunt, R. (2017). Repeat sales index for residential real estate in Krakow (No. 29/2017). Institute of Economic Research Working Papers.

Damianov, D. S., & Escobari, D. (2016). Long-run equilibrium shift and short-run dynamics of US home price tiers during the housing bubble. The Journal of Real Estate Finance and Economics, 53(1), 1–28.

De Wit, E. R., Englund, P., & Francke, M. K. (2013). Price and transaction volume in the Dutch housing market. Regional Science and Urban Economics, 43(2), 220–241.

Diba, B. T., & Grossman, H. L. (1988). Explosive Rational Bubbles in Stock Prices? American Economic Review, 78, 520–530.

Drake, L. (1993). Modelling UK house prices using cointegration: An application of the Johansen technique. Applied Economics, 25(9), 1225–1228.

Fisher, J. D., Geltner, D. M., & Webb, R. B. (1994). Value indices of commercial real estate: A comparison of index construction methods. The Journal of Real Estate Finance and Economics, 9(2), 137–164.

Flood, R. P., & Hodrick, R. J. (1990). On testing for speculative bubbles. The Journal of Economic Perspectives, 4(2), 85–101.

Follain, J. R., & Jimenez, E. (1985). Estimating the demand for housing characteristics: A survey and critique. Regional Science and Urban Economics, 15(1), 77–107.

Fraser, P., Hoesli, M., & McAlevey, L. (2008). House Prices and Bubbles in New Zealand. The Journal of Real Estate Finance and Economics, 37(1), 71–91.

Galati, G., & Teppa, F. (2017). Heterogeneity in house price dynamics. De Nedrelandsche Bank Working Paper, 564.

Gallin, J. (2006). The long-run relationship between house prices and income: Evidence from local housing markets. Real Estate Economics, 34(3), 417–438.

Gao, A., Lin, Z., & Na, C. F. (2009). Housing market dynamics: Evidence of mean reversion and downward rigidityq. Journal of Housing Economics, 18, 256–266.

Głuszak, M., Czerski, J., & Zygmunt, R. (2018). Estimating repeat sales residential price indices for Krakow. Oeconomia Copernicana, 9(1), 55–69.

Hendershott, P. H. (2000). Property Asset Bubbles: Evidence from the Sydney Office Market. The Journal of Real Estate Finance and Economics, 20(1), 67–81.

Hill, R., & Trojanek, R. (2020). Strategic house price indexes for warsaw: An evaluation of competing methods. Graz Economics Papers, University of Graz, Department of Economics, 2020-08

Himmelberg, C., Mayer, C., & Sinai, T. (2005). Assessing high house prices: Bubbles, fundamentals and misperceptions. Journal of Economic Perspectives, 19(4), 67–92.

Hott, C., & Monnin, P. (2008). Fundamental real estate prices: An empirical estimation with international data. The Journal of Real Estate Finance and Economics, 36(4), 427–450.

Hui, E. C. M., Ng, I., & Lau, O. M. F. (2011). Speculative bubbles in mass and luxury properties: An investigation of the Hong Kong residential market. Construction Management and Economics, 29(8), 781–793.

Hui, E. C., & Wang, Z. (2014). Market sentiment in private housing market. Habitat International, 44, 375–385.

Hui, E. C. M., & Yue, S. (2006). Housing price bubbles in Hong Kong, Beijing and Shanghai: A comparative study. The Journal of Real Estate Finance and Economics, 33(4), 299–327.

Hulchanski, J. D. (1995). The concept of housing affordability: Six contemporary uses of the housing expenditure-to-income ratio. Housing Studies, 10(4), 471–491.

Kouwenberg, R., & Zwinkels, R. (2014). Forecasting the US housing market. International Journal of Forecasting, 30(3), 415–425.

Krainer, J., & Wei, C. S. (2004). House prices and fundamental value. FRBSF Economic Letter, No. 2004–27, Federal Reserve Bank of San Francisco.

Kucharska-Stasiak, E., Schneider, B., & Załęczna, M. (2009). Methodology for Local and Regional real estate market, Wydawnictwo Uniwersytetu Łódzkiego, Łódź.

Łaszek, J., Augustyniak, H., Widłak, M., (2009), House price bubbles on the major polish housing markets, Working paper presented at the Annual Conference of the European Network for Housing Research, Prague.

Łaszek, J. (2013). Podejście modelowe do rynku nieruchomości. Bezpieczny Bank, 53(4), 204–268.

Łaszek, J., Olszewski, K., & Waszczuk, J. (2016). Monopolistic competition and price discrimination as a development company strategy in the primary housing market. Critical Housing Analysis, 3(2), 1–12.

Leamer, E. E. (2007). Housing is the business cycle. NBER working paper series, no. 13428.

Leszczyński, R., & Olszewski, K. (2015). Commercial property price index for Poland. Bank i Kredyt, 46(6), 565–578.

Madsen, J. B. (2012). A behavioural model of house prices. Journal of Economic Behavior & Organization, 82(1), 21–38.

Malpezzi, S. (1999). A simple error correction model of house prices. Journal of Housing Economics, 8(1), 27–62.

Mao, G., & Shen, Y. (2019). Bubbles or fundamentals? Modeling provincial house prices in China allowing for cross-sectional dependence. China Economic Review, 53(June 2017), 53–64.

Mayer, C., & Sinai, T. (2009). U.S. House Price Dynamics and Behavioral Finance. In Policymaking Insights from Behavioral Economics. Federal Reserve Bank Boston.

McMillen, D. P., & Thorsnes, P. (2006). Housing renovations and the quantile repeat-sales price index. Real Estate Economics, 34(4), 567–584.

Mikhed, V., & Zemčík, P. (2009). Do house prices reflect fundamentals? Aggregate and panel data evidence. Journal of Housing Economics, 18(2), 140–149.

Miles, W. (2008). Boom-bust cycles and the forecasting performance of linear and non-linear models of house prices. The Journal of Real Estate Finance and Economics, 36(3), 249–264.

Moons, C., & Hellinckx, K. (2019). Did monetary policy fuel the housing bubble? An application to Ireland. Journal of Policy Modeling, 41(2), 294–315.

Morano, P., & Tajani, F. (2014). Least median of squares regression and minimum volume ellipsoid estimator for outliers detection in housing appraisal. International Journal of Business Intelligence and Data Mining, 9(2), 91–111.

Author 1, Author 2. (2021). Normalisation of the ……. (We will complete this reference in the final version to ensure a blind review).

Olszewski, K., Decyk, P., Gałaszewska, K., Jakubowski, A., Kulig, M., Modzelewska, R., & Żywiecka, H. (2018). Hedonic analysis of office and retail rents in three major cities in Poland (pp. 383–391) IN: Recent trends in the real estate market and its analysis łaszek J., Olszewski K., Sobiecki R. (reds.), SGH Warsaw School Of Economics.

Olszewski, K., Waszczuk, J., & Widłak, M. (2017). Spatial and hedonic analysis of house price dynamics in Warsaw, Poland. Journal of Urban Planning and Development, 143(3), 04017009.

Ozhegov, E. M., & Sidorovykh, A. S. (2017). Heterogeneity of sellers in housing market: Difference in pricing strategies. Journal of Housing Economics, 37, 42–51.

Pan, W. F. (2019). Detecting bubbles in China’s regional housing markets. Empirical Economics, 56(4), 1413–1432.

Phillips, P. C. B., Shi, S., & Yu, J. (2015a). Testing for multiple bubbles: Historical episodes of exuberance and collapse in the S&P 500. International Economic Review, 56(4), 1043–1078.

Phillips, P. C., Shi, S., & Yu, J. (2015b). Testing for multiple bubbles: Limit theory of realtime detectors. International Economic Review, 56(4), 1079–1134.

Phillips, P. C., Wu, Y., & Yu, J. (2011). Explosive behavior in the 1990s Nasdaq: When did exuberance escalate asset values? International Economic Review, 52(1), 201–226.

Qiu, L., & Tu, Y. (2018). Homebuyers’ heterogeneity and housing prices. Available at SSRN 3187233.

Renigier-Biłozor, M., Janowski, A., & d’Amato, M. (2019). Automated valuation model based on fuzzy and rough set theory for real estate market with insufficient source data. Land Use Policy, 87, 104021.

Shen, Y., Hui, E. C. M., & Liu, H. (2005). Housing price bubbles in Beijing and Shanghai. Management Decision, 43(4), 611–627.

Smith, M. H., & Smith, G. (2006). Bubble, Bubble, Where’s the Housing Bubble? Brookings Papers on Economic Activity, 2006(1), 1–50.

Śpiewak, B., & Barańska, A. (2020). Chosen statistical methods for the detection of outliers in real estate market analysis. Acta Scientiarum Polonorum Administratio Locorum, 19(2), 109–118.

Stevenson, S. (2008). Modeling housing market fundamentals: Empirical evidence of extreme market conditions. Real Estate Economics, 36(1), 1–29.

Stone, M. E. (2006a). A housing affordability standard for the UK. Housing Studies, 21(4), 453–476.

Stone, M. E. (2006b). What is housing affordability? The case for the residual income approach. Housing Policy Debate, 17(1), 151–184.

Swanson, N. R. (1998). Money and output viewed through a rolling window. Journal of Monetary Economics, 41(3), 455–474.

Taipalus, K. (2006). A global house price bubble? Evaluation based on a new rent-price approach. Bank of Finland Discussion Papers 29, Helsinki, Finland.

Tomal, M. (2019). The impact of macro factors on apartment prices in Polish counties: A two-stage quantile spatial regression approach. Real Estate Management and Valuation, 27(4), 1–14.

Tomal, M. (2021). Identification of house price bubbles using robust methodology: evidence from Polish provincial capitals. Journal of Housing and the Built Environment. https://doi.org/10.1007/s10901-021-09903-3

Tomal, M. (2021). Testing for overall and cluster convergence of housing rents using robust methodology: evidence from Polish provincial capitals. Empirical Economics. https://doi.org/10.1007/s00181-021-02080-w

Tomal, M., & Helbich, M. (2022). The private rental housing market before and during the COVID-19 pandemic: A submarket analysis in Cracow, Poland. Urban Analytics and City Science. https://doi.org/10.1177/23998083211062907

Trojanek, R. (2012). An analysis of changes in dwelling prices in the biggest cities of Poland in 2008–2012 conducted with the application of the hedonic method. Actual Problems of Economics, 7(2), 5–14.

Tsai, I. C. (2019). Dynamic price–volume causality in the American housing market: A signal of market conditions. The North American Journal of Economics and Finance, 48, 385–400.

Tsai, I. C., & Peng, C. W. (2011). Bubbles in the Taiwan housing market: The determinants and effects. Habitat International, 35(2), 379–390.

Tyc, W. (2013). Modele Idealizacyjne Baniek Cenowych. Przegląd Zachodniopomorski, 3(1), 339–356.

Van Norden, S., & Schaller, H. (1993). The predictability of stock market regime: Evidence from the Toronto Stock Exchange. The Review of Economics and Statistics, 75(3), 505–510.

Vishwakarma, V. K., & Paskelian, O. G. (2012). Bubble in the Indian real estate markets: Identification using regime-switching methodology. International Journal of Business & Finance Research, 6(3), 27–40.

Waddell, P. (2000). A behavioural simulation model for metropolitan policy analysis and planning: Residential location and housing market components of UrbanSim. Environment and Planning b: Planning and Design, 27(2), 247–263.

Wang, F. T., & Zorn, P. M. (1997). Estimating house price growth with repeat sales data: What’s the aim of the game? Journal of Housing Economics, 6(2), 93–118.

Wang, J., Koblyakova, A., Tiwari, P., & Croucher, J. S. (2018). Is the Australian housing market in a bubble? International Journal of Housing Markets and Analysis, 13(1), 77–95.

Widłak, M. (2010). Dostosowanie indeksów cenowych do zmian jakości. Metoda wyznaczania hedonicznych indeksów cen i możliwości ich zastosowania dla rynku mieszkaniowego. Narodowy Bank Polski, Warsaw.

Widlak, M., Waszczuk, J., & Olszewski, K. (2015). Spatial and hedonic analysis of house price dynamics in Warsaw. National Bank of Poland Working Paper, 197.

Widłak, M., & Tomczyk, E. (2010). Measuring price dynamics: evidence from the Warsaw housing market. Journal of European Real Estate Research, 3(3), 203–227.

Wu, Y., Wei, Y. D., & Li, H. (2020). Analyzing spatial heterogeneity of housing prices using large datasets. Applied Spatial Analysis and Policy, 13(1), 223–256.

Xu, T. (2008). Heterogeneity in housing attribute prices. International Journal of Housing Markets and Analysis, 1(2), 166–181.

Żelazowski, K. (2007). Zjawisko bańki cenowej w kontekście zmian na polskim rynku mieszkaniowym. Studia i Materiały Towarzystwa Naukowego Nieruchomosci, 15(102), 139–148.

Żelazowski, K. (2008). Zjawisko baniek cenowych na rynkach nieruchomości. Studia i Materiały Towarzystwa Naukowego Nieruchomości, 16(4), 99–108.

Zhi, T., Li, Z., Jiang, Z., Wei, L., & Sornette, D. (2019). Is there a housing bubble in China? Emerging Markets Review, 39, 120–132.

Źróbek, S., Kovalyshyn, O., Renigier-Biłozor, M., Kovalyshyn, S., & Kovalyshyn, O. (2020). Fuzzy logic method of valuation supporting sustainable development of the agricultural land market. Sustainable Development, 28, 1094–1105.

Zyga, J. (2015). Search for dissimilarity factors for nominally indiscernible facilities. Real Estate Management and Valuation, 23(3), 65–72.

Zyga, J. (2019). Dissimilarity as a component of the property price model. Real Estate Management and Valuation, 27(3), 124–132.

Author information

Authors and Affiliations

Corresponding author

Ethics declarations

Conflict of interest

The authors declare that they have no conflict of interest.

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

The speculative frame method was originally described in author’s doctoral dissertation. The dissertation has not been published and is not scheduled for publication. The dissertation is written in Polish (original language).

Rights and permissions

About this article

{kind=link}

Cite this article

Brzezicka, J., Wisniewski, R. The applicability of the speculative frame method for detecting disturbances on the real estate market: evidence from Poland. J Hous and the Built Environ 38, 467–495 (2023). https://doi.org/10.1007/s10901-022-09954-0

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s10901-022-09954-0