Application of Taylor Rule Fundamentals in Forecasting Exchange Rates

Faculty of Business, Economics and Social Sciences, Christian-Albrechts-University of Kiel, Olshausenstr. 40, D-24118 Kiel, Germany

Economies 2021, 9(2), 93; https://doi.org/10.3390/economies9020093

Submission received: 20 May 2021

/

Revised: 10 June 2021

/

Accepted: 15 June 2021

/

Published: 21 June 2021

(This article belongs to the Special Issue International Financial Markets and Monetary Policy)

Abstract

:This paper examines the effectiveness of the Taylor rule in contemporary times by investigating the exchange rate forecastability of selected four Organisation for Economic Co-operation and Development (OECD) member countries vis-à-vis the U.S. It employs various Taylor rule models with a non-drift random walk using monthly data from 1995 to 2019. The efficacy of the model is demonstrated by analyzing the pre- and post-financial crisis periods for forecasting exchange rates. The out-of-sample forecast results reveal that the best performing model is the symmetric model with no interest rate smoothing, heterogeneous coefficients and a constant. In particular, the results show that for the pre-financial crisis period, the Taylor rule was effective. However, the post-financial crisis period shows that the Taylor rule is ineffective in forecasting exchange rates. In addition, the sensitivity analysis suggests that a small window size outperforms a larger window size.

1. Introduction

Exchange rates have been a prime concern of the central banks, financial services firms and governments because they control the movements of the markets. They are also said to be a determinant of a country’s fundamentals. This makes it imperative to forecast exchange rates. Generally, one could ask, is there any benefit in accurately forecasting the exchange rates? Ideally, there is no intrinsic benefit to accurate forecasts; they are made to enhance the resulting decision making of policymakers (Hendry et al. 2019).

One of the popular investigations into the exchange rate movements was made by Meese and Rogoff (1983). In their paper, they perform the out-of-sample exchange rates forecast during the post-Bretton Woods era. They found that the random walk model performs better with the exchange rate forecast than the economic fundamentals. This was the Meese–Rogoff puzzle. Subsequently, researchers have challenged the Meese and Rogoff findings. Mark (1995) uses the fundamental values to show the long-run predictability of the exchange rate. Clarida and Taylor (1997) use the interest rate differential to forecast spot exchange rates. Mark and Sul (2001) also find evidence of predictability for 13 out of 18 exchange rates using the monetary models.

In 1993, John B. Taylor presented monetary policy rules that describe the interest rate decisions of the Federal Reserve’s Federal Open Market Committee (FOMC). In most literature, this has been named the Taylor rule. Taylor (1993) stipulates that the central bank regulates the short-run interest rate in response to changes in the inflation rate and the output gap (interest rate reaction function). This has become a monetary policy rule which the Federal Reserve (Fed) and other central banks have incorporated into their decision making (Taylor 2018). The Taylor rule principle is used in this study due to its effectiveness in monetary policy. It is superior to the traditional models as it combines the uncovered interest rate parity, the purchasing power parity and the other monetary variables for forecasting exchange rates. This makes it a more robust method for forecasting the exchange rates. The Taylor rule monetary policy operates well in countries that practice floating exchange rates with an inflation-targeting framework.

Economists have derived two versions of the Taylor rule to forecast the exchange rate. These include Taylor rule differentials and Taylor rule fundamentals. Engel et al. (2008) developed the Taylor rule differentials model by subtracting the Taylor rule of the domestic country from that of the foreign country. Instead of using the estimated parameters, they apply the postulated parameters into the forecasting regression to perform the test. They perform out-of-sample predictability of the exchange rate and find that the Taylor rule differentials models perform better than the random walk in the long horizon compared to the short horizon. Other literature including Engel et al. (2009) provides supporting evidence of the Taylor rule models in predicting the exchange rate.

The Taylor rule fundamentals model was first established by Molodtsova and Papell (2009). They deducted the Taylor rule of the foreign country from the domestic country and the variables contained in the Taylor rule equation are directly utilized to perform an out-of-sample prediction for the exchange rate. Rossi (2013) surveys the exchange rate forecast models in most literature and finds strong evidence in favor of the Taylor rule fundamentals by Molodtsova and Papell (2009). However, in reaction to the global financial crisis, the major central banks set short-term interest rates to a zero lower bound (ZLB) which renders the conventional monetary policies ineffective. This has led to a debate among thought leaders on the efficacy of the Taylor rule.

The objective of this study is to check the effectiveness of the Taylor rule monetary policy in contemporary times by applying the Taylor rule fundamentals to forecast the exchange rates using current data and a new set of currency pairs. The research, therefore, contributes to the existing literature by investigating the usefulness of the Taylor rule-based exchange rate forecast in the pre- and post-crisis periods. More so, the study examines the sensitivity of the window size on the performance of the Taylor rule fundamentals. The research paper applies to four (4) OECD countries, namely, Norway, Chile, New Zealand and Mexico vis-à-vis the United States (U.S.). These countries adopt floating exchange rates with an inflation-targeting framework.

The impetus for selecting these countries includes the fact that Norway is one of the long-standing trading partners of the United States. Norway invests about 35% of its government pension fund in the U.S. Bloomberg (2019) reported that Norway plans to increase its wealth fund by USD 100 billion in U.S. stocks1. This shows that their economies and the exchange rate could be affected by the Taylor rule policy. However, the Norwegian exchange rate has received less research. Chile and Mexico were selected for this research because they are among the seven largest economies in Latin America that are emerging economies and have a floating exchange rate and inflation target framework. These countries contribute to the research by depicting how the Taylor rule monetary policy affects the exchange rates of the emerging economies in Latin America. New Zealand is the first country to implement the inflation-targeting framework in the early 1990s. Therefore, the Reserve Bank of New Zealand would exhibit a greater experience of the Taylor rule policy. These countries have chronological market relations regarding trading with the U.S. Their economies rely very much on the importation and exportation of goods and services.

Moreover, the Triennial Survey by the Bank for International Settlements (BIS) (2019) shows that the U.S. dollar is the most traded currency and the U.S. has been the center for international trading over the years. In 2019, the U.S. dollar contributed 88.3% of the total foreign exchange market volume. In 2019, the New Zealand dollar was ranked 11th among the global currencies trading, adding about 2.1% to the foreign exchange market volume. In the same currencies rankings, the Norwegian krone ranks 15th and the Mexican peso ranks 16th for contributing 1.8% and 1.7%, respectively. The U.S., Norway, Chile and New Zealand are noted as having “commodity currencies”2 which influence the exchange rate changes (Chen et al. 2010). These features contribute to the choice of selecting the countries for this research.

The domestic country considered in this study is the U.S. An out-of-sample forecast is performed in the short horizon for the Norwegian krone, Chilean peso, New Zealand dollar and Mexican peso exchange rates with the U.S. dollar. The benchmark model is the random walk. A linear model is used in this work since it is shown to be the most efficacious exchange rate forecastability in the literature (Rossi 2013). The forecast would be evaluated by using the mean squared forecast error. For the forecast comparison, Molodtsova and Papell (2009) state that the linear model is nested; therefore, Clark and West’s (2006, 2007) model is used to perform the significant test3. In this paper, similar models and specifications by Molodtsova and Papell (2009) are used.

It is important to stress that this study does not show which models beat the random walk but rather aims to show how accurately, significantly and reliably the Taylor rule fundamentals could forecast the exchange rate movements. Accuracy means that the forecasts are close to the values of the exchange rate. This follows a claim by Engel and West (2005) that the random walk performance is not a surprise but a result of rational expectations. This means that the exchange rate acts as a near-random walk and the random walk is not easy to beat (Diebold 2017).

The study seeks to shed light on these research questions: Can the Taylor rule fundamentals models accurately forecast currency exchange rates? How significant are the Taylor rule fundamentals in forecasting the exchange rate during the global financial crisis and great recession? Has the Taylor rule been effective in describing the exchange rate changes after the financial crisis? Can the exchange rate directions be forecasted by the Taylor rule fundamentals? In this paper, it is observed that the Taylor rule fundamentals could effectively describe and forecast the exchange rates until the financial crisis. In contrast, the Taylor rule fundamentals have been insignificant in forecasting exchange rates in the post-financial crisis. In addition, the choice of window size selection affects the forecast outcome of the models. The study shows that the smaller window size (60 observations) influences the Taylor rule fundamentals models to forecast the exchange rate better than the larger window size (120 observations).

The remainder of the study is structured as follows: Section 1.1 gives some literature reviews on the topic. Section 2 provides a theoretical framework, and details of the Taylor rule fundamentals are essential to this study. Section 3 describes the models and specifications for the forecast. Section 4 discusses the empirical framework, which also contains the data. Section 5 contains the main empirical test result, and Section 6 provides some economic analysis of the results. Section 7 concludes the study.

1.1. Literature Review

Recent research studies in the exchange rate forecast have advanced our knowledge of the exchange rate movement in the market. Some of the literature explains how Taylor rule fundamentals are used to forecast the exchange rate in different countries and with diversified approaches.

Molodtsova and Papell (2009) performed one month ahead of out-of-sample prediction of the exchange rate with the Taylor rule fundamentals for 12 OECD countries vis-à-vis the U.S. for the post-Bretton Woods period (from 1973 to 2006). Quasi-real-time data were used in their paper. Out of 16 specifications generated, they found a 5% level significant evidence of exchange rate forecast for 11 out of the 12 OECD Countries. Their strongest evidence results from the symmetric Taylor rule model with heterogeneous coefficients, interest rate smoothing and a constant. In addition, the paper finds strong evidence of exchange rate predictability with the Taylor rule fundamental models as compared to the conventional interest rates parity, purchasing power parity (PPP) and monetary models.

In addition, Molodtsova et al. (2011) used real-time quarterly data to find proof of out-of-sample predictability of the USD/EUR exchange rate based on the Taylor rule fundamentals. Another research by Molodtsova and Papell (2012) finds evidence of USD/EUR exchange rate predictability with the Taylor rule fundamentals during the financial crisis and the great recession.

Moreover, Ince (2014) applied real-time data to evaluate the out-of-sample forecast of the exchange rate with PPP and Taylor rule fundamentals using single-equation and panel methods. Using bootstrapped out-of-sample test statistics, Ince found that the Taylor rule fundamentals better forecast the exchange rate at the one-quarter-ahead. However, the Taylor rule fundamentals forecast performance is not improved with the panel estimation. Contrary to the Taylor rule fundamentals, the researcher found that the PPP model was better at forecasting the exchange rate in the longer horizon (16-quarter). Its forecast performance increases in the panel model relative to a single-equation estimation.

Byrne et al. (2016) contributed to the study by forecasting the exchange rates using the Taylor rule fundamentals and inculcating Bayesian models of time-varying parameters. They incorporated the financial crisis into their work and found that the Taylor rule fundamentals have the power to predict the exchange rate. Ince et al. (2016) extended the work by Molodtsova and Papell (2009) and demonstrated short-run out-of-sample predictability of the exchange rate with the two versions of the Taylor rule model for eight exchange rates vis-à-vis the U.S. dollar. Their research found strong evidence of exchange rate predictability with the Taylor rule fundamental model as compared to the Taylor rule differential and much stronger proof than the traditional exchange rate predictors. Cheung et al. (2019) performed exchange rate prediction redux and found the Taylor rule fundamentals outperform the random walk when the models’ performances are measured with the mean squared prediction errors. However, they did not find statistically significant performance when the DMW test was conducted.

In addition to the basic linear model, Caporale et al. (2018) investigated the Taylor rule in five emerging economies through an augmented rule including exchange rates and a nonlinear threshold specification, which was estimated by the generalized method of moments. They found an overall performance of the augmented nonlinear Taylor rule to describe the actions of monetary authorities in these five countries.

Furthermore, Zhang and Hamori (2020) performed exchange rate prediction by combining modern machine learning methodologies (neural network models, random forest and support vector machine) with four fundamentals that include the Taylor rule models, uncovered interest rate, purchasing power parity and monetary model. Their root mean squared error and Diebold–Mariano test results prove that the fundamental models together with the machine learning perform better than the random walk.

2. Taylor Rule Fundamentals

Researchers have discovered that macroeconomics policies that center on the price level (inflation) and real output directly perform better than other policies such as money supply targeting. In 1993, John B. Taylor proposed that for a flexible exchange rate regime, the central bank adjusts its short-term interest rate target in response to changes in the price level (inflation rate) and real output (output gap) from a target as given in Equation (1):

where it† is the target for the short-term nominal interest rate. and † are the inflation rate and target level of inflation, respectively4. yt is the output gap (percent deviation of actual real gross domestic product (GDP) from an estimate of its potential level) and r† is the equilibrium level of the real interest rate. The parameters are the weights representing the central bank’s reactions to the changes in the inflation rate and the output gap. Taylor assumes that inflation and output have the same weight of reaction (0.5 parameters each). Both the inflation target and the real interest rate are 2% at equilibrium. According to Taylor (1993), the short-term nominal interest rate would be raised by the Fed if the inflation rises over the target inflation level or the realized output is above the potential output and vice versa.

Molodtsova and Papell (2009) proposed fundamentals on the account of the Taylor rule monetary policy. The Taylor rule fundamentals suggest that when two economies fix their interest rates based on the Taylor rule, their interests would influence the exchange rate through the concept of uncovered interest rate parity. Now, following the asymmetric model by Clarida et al. (1998), the real exchange rate is added to the Taylor rule for the foreign countries. The idea is that the Fed sets the target level of the exchange rate to make PPP hold. That is, the nominal interest rate rises or falls if the exchange rate depreciates or appreciates from the PPP. This is expressed in Equation (2) below:

where zt is the real exchange rate and is the coefficient.

Also by the Clarida et al. (1998) smoothing model, Molodtsova and Papell (2009) assume in Equation (3) that the U.S. actual nominal interest rate adjusts to its target rate and lagged value. The lagged value is added since, in decision making, the central bank could not observe the ex-post-realized nominal interest rate. Hence, the lag value helps to account for delay adjustment.

where is the coefficient of lag interest rate. Putting Equation (2) into (3) gives the interest rate reaction function of the U.S.

where = 0 for the U.S. if the real exchange rate approaches equilibrium. Molodtsova and Papell (2009) derive the Taylor rule fundamentals-based forecasting equation by subtracting the interest rate reaction function of the foreign country from the U.S. This results in an interest rate differential function represented in Equation (5).

where * denotes foreign variables, the constants are: = (1 − )(1 + ), y = (1 − ), z = (1 − ), and = (1 − )(* + r*), and vt is the shock term.

The observation from Equation (5) is that, if the inflation rate rises over the target in the U.S. economy, the Fed responds to it by increasing the interest rate. It is worth noting that the monetary model of exchange rate implies an opposite relationship between interest rates and exchange rate, with higher domestic interest rate leading to an exchange rate depreciation. If uncovered interest rate parity (UIRP) holds, Dornbusch (1976) proposes that overshooting causes the U.S. dollar (USD) to later depreciate. It is empirically proven in most literature (Chinn and Quayyum 2012) that UIRP does not hold in the short run; hence, following Gourinchas and Tornell (2004), Molodtsova and Papell (2009) shows that the interest rate increment leads to a continuous rise in the USD.

According to the Taylor rule (1993), the appreciation of the USD causes the inflation rate in foreign countries to rise. Applying the symmetric model, the foreign central banks respond by increasing the foreign interest rate. Investors begin to move their capital from the U.S. to foreign countries, since there would be higher returns on foreign investment. The demand for the USD diminishes, the exchange rate immediately appreciates up to the point where the interest rate differential equals the expected depreciation, and the dollar starts to depreciate (forward premium).

Another reaction from the Taylor rule (1993) is that if the U.S. output gap increases, the Fed raises the Federal funds rate by αy, causing the USD to appreciate. By contrast, if the foreign country’s output gap increases and follows the Taylor rule, its central bank raises its interest rate, causing the USD depreciation. Moreover, the foreign central bank raises its interest rate when it observes a fall in its real exchange rate. This leads to a fall in the demand for the USD and immediate or forecasted depreciation. If the countries practice the smoothing model, a higher lagged interest rate increases current and expected future interest rates, which leads to an immediate and sustained USD appreciation. However, a higher lagged foreign interest rate causes a current or expected fall in the U.S. interest rate, and the USD is predicted to depreciate. From the rational expectations and the predictions explained above, it is observed that interest rate shocks that cause the central banks to respond to interest rate adjustment also have an impact on the exchange rate. Combining the analyses from Equation (5), the Taylor-rule-based exchange rate forecasting equation is developed as:

where st is the log of the U.S. dollar nominal exchange rate taken as the domestic price of foreign currency and t+1 is the change in the nominal exchange rate. i represent the parameters of the forecasting equation.

3. Model Description

Rossi (2013) explains how successful the linear equation model has been in forecasting the exchange rate. Therefore, a single-equation linear model as represented in Equation (6) is analyzed in this research. The same specifications proposed by Molodtsova and Papell (2009) would be used in this paper. Firstly, as proposed in Taylor (1993), there is a symmetric model (βz* = 0) if the Fed and the foreign central banks follow the same rule to set the nominal interest rate based on current inflation, inflation gap (actual–target inflation), the output gap (actual–potential GDP) and equilibrium real interest rate. If the foreign central bank adds the real exchange rate to its Taylor rule (βz* ≠ 0), it is described as an asymmetric model (Clarida et al. 1998).

Secondly, smoothing is considered, which is the interest rate expressed on its lag variable (βi ≠ 0, βi* ≠ 0). Contrary, without interest rate lag it is termed as no smoothing (βi = 0, βi* = 0). The third model used in Molodtsova and Papell (2009) is homogeneous. This occurs when the domestic and foreign central banks have the same parameter in their Taylor rule fundamental variables (βπ = βπ*, βy = βy*, βi = βi*). However, if their response parameters are not the same, the heterogeneous model would be constructed for it (βπ ≠ βπ*, βy ≠ βy*, βi ≠ βi*). Constant (β ≠ 0) and no constant (β = 0) are constructed as the fourth model. If the domestic and foreign central banks do not have the same target inflation rates and equilibrium real interest rates, a constant is added to the right-hand side of the equation and vice versa. The specifications by Molodtsova and Papell (2009) are modified to construct 16 models for this research as below:

- Model 1:

- Symmetric, Smoothing, Homogeneous Coefficients and a Constant{β πt − πt * yt − yt* it−1 − it−1*}

- Model 2:

- Symmetric, Smoothing, Homogeneous Coefficients and no Constant{πt − πt * yt − yt* it−1 − it−1*}

- Model 3:

- Symmetric, Smoothing, Heterogeneous Coefficients and a Constant{β πt πt * yt yt* it−1 it−1*}

- Model 4:

- Symmetric, Smoothing, Heterogeneous Coefficients and no Constant{πt πt * yt yt* it−1 it−1*}

- Model 5:

- Symmetric, no Smoothing, Homogeneous Coefficients and a Constant{β πt − πt * yt − yt*}

- Model 6:

- Symmetric, no Smoothing, Homogeneous Coefficients and no Constant{πt − πt * yt − yt*}

- Model 7:

- Symmetric, no Smoothing, Heterogeneous Coefficients and a Constant{β πt πt * yt yt*}

- Model 8:

- Symmetric, no Smoothing, Heterogeneous Coefficients and no Constant{πt πt * yt yt*}

- Model 9:

- Asymmetric, Smoothing, Homogeneous Coefficients and a Constant{β πt − πt * yt − yt* it−1 − it−1* zt*}

- Model 10:

- Asymmetric, Smoothing, Homogeneous Coefficients and no constant{πt − πt * yt − yt* it−1 − it−1* zt*}

- Model 11:

- Asymmetric, Smoothing, Heterogeneous Coefficients and a constant{β πt πt * yt yt* it−1 it−1* zt*}

- Model 12:

- Asymmetric, Smoothing, Heterogeneous Coefficients and no Constant{πt πt * yt yt* it−1 it−1* zt*}

- Model 13:

- Asymmetric, no Smoothing, Homogeneous Coefficients and constant{β πt − πt * yt − yt* zt*}

- Model 14:

- Asymmetric, no Smoothing, Homogeneous Coefficients and no Constant{πt − πt * yt − yt* zt*}

- Model 15:

- Asymmetric, no Smoothing, Heterogeneous Coefficients and Constant{β πt πt * yt yt* zt*}

- Model 16:

- Asymmetric, no Smoothing, Heterogeneous Coefficients and no Constant{πt πt * yt yt* zt*}

4. Empirical Framework

4.1. Benchmark Model and Window Sensitivity Selection

The choice of benchmark and window size usually has an impact on the forecast results. After Meese and Rogoff (1983), it has been widely debated in most studies that the exchange rate follows a random walk. This implies that the exchange rate has a minimal chance of forecasting. There are two forms of random walk models discussed by Rossi (2013). These include a random walk without drift: t+1 = 0. This is a martingale difference, which means that the current exchange rate steps from the previous exchange rate observation. Another form of a random walk considered in the literature is a random walk with drift. This is shown as t+1 = δt, where δt is a drift term included in the random walk. The drift can be thought of as determining a trend in the exchange rate. The exchange rate forecast surveyed by Rossi (2013) affirms that random walk without drift as a benchmark performs better than with drift. Therefore, in this paper, the random walk without drift is used as the benchmark.

Inoue and Rossi (2012) have shown that rolling windows of small size are more helpful to check predictive power. Although larger window size reduces the effect of outliers, Elliott and Timmermann (2016) explain that larger window size sometimes includes past data which are not important for current prediction. Hendry et al. (2019) add that a smaller window size excludes irrelevant information that might cause forecast failure. In this study, the empirical analysis is performed with a fixed-length rolling window with a 60 window size for the estimation.

4.2. Data Description

The countries under study include Norway, Chile, New Zealand and Mexico vis-à-vis the United States of America. The currencies include U.S. dollar (USD), Norwegian krone (NOK), Chilean peso (CLP), New Zealand dollar (NZD) and Mexican peso (MXN). Considering the indirect quotation of the exchange rate data, the USD is used as the base currency in this study. Monthly data of each country from 1995M1 to 2019M12 are applied to the estimation and forecasting of the exchange rate and includes a key financial phenomenon such as the 2008 global financial crisis which affected the foreign exchange movement. The raw data used include the foreign exchange rates (St), interest rate (it), income (output) (yt) and prices (pt)5. The consumer price index (CPI) is used to measure the price level in the economy. The federal funds rate is used as a short-term interest for the U.S. The money market rates are used as the short-run interest rate for Norway, New Zealand and Mexico. The deposit rates are used as the short-run interest rate for Chile since there were no available money market rate data. The industrial production (IP) index is used to replace countries’ national income because GDP data are not consistently published.

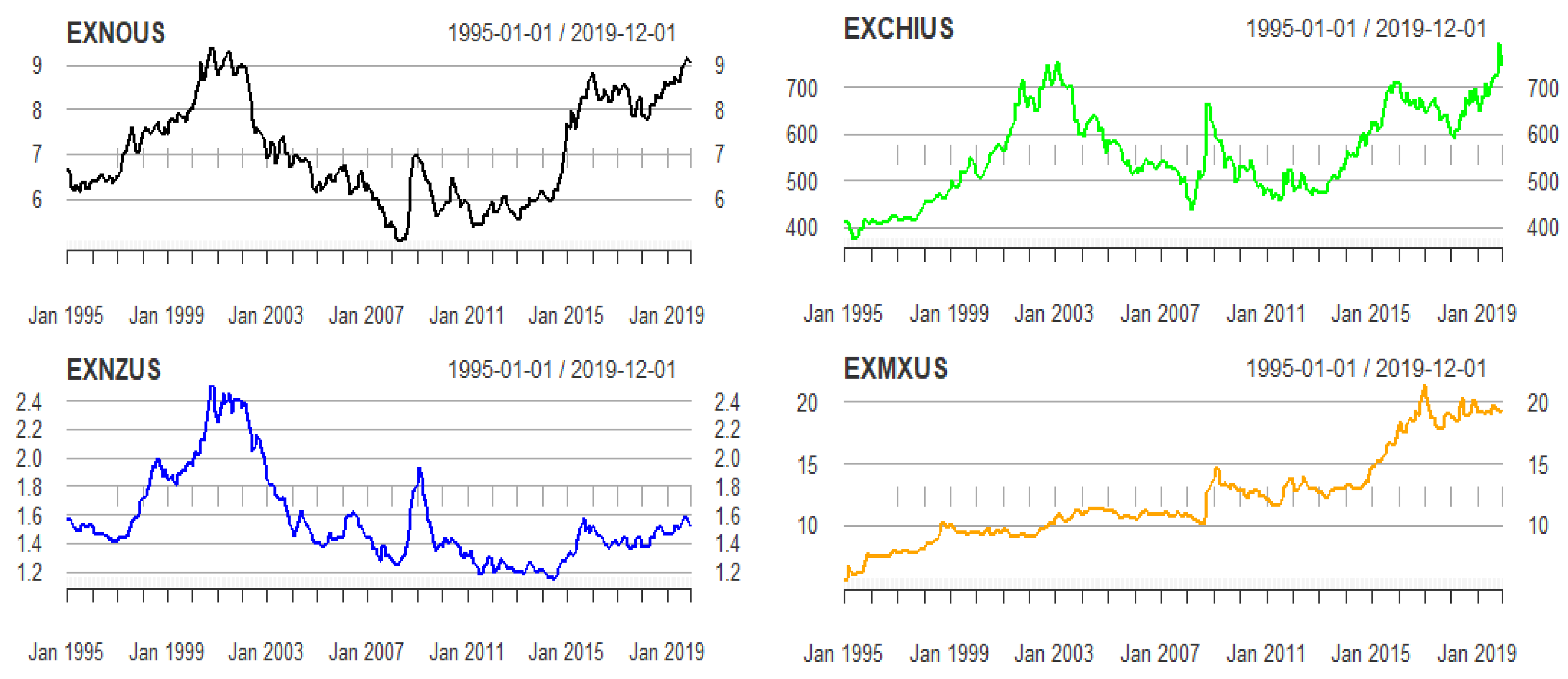

From 1995, enormous fluctuations in the exchange rates have been experienced in the countries. The dot-com boom between 2000 and 2001 led to economic growth in the U.S. As a result, the NOK, CLP, NZD and MXN currencies depreciated against the USD. Norway introduced inflation targeting in 2001 after the NOK depreciated highly in 2000 and the USD/NOK exchange rate reached 9.65. During the 2007–2008 financial crisis, the USD depreciated, and the NOK, CLP, NZD and MXN appreciated. This caused their exchange rates against the USD to fall. For instance, in 2008, the USD/NOK declined to about 4.94. The exchange rates immediately increased in 2009 when the USD appreciated against the other currencies. However, commodity currencies such as NOK, CLP and NZD quickly appreciated due to a boom in commodities prices in 2009. The depreciation of the NOK, CLP, NZD and MXN against the USD was observed in 2019. The MXN has especially been on an incessant path of depreciation against the USD due to loss of productivity in Mexico comparative to the U.S. (see Figure 1 for details).

The output gap (yt) in this paper is measured as the percentage deviation of actual output from a Hodrick and Prescott (1997) (HP) generated trend6. This is because there is no standard description of potential GDP used in the central banks’ interest rate reaction function. There are other alternatives measures of the output gap for example percentage deviations of actual output from a linear time trend or a quadratic time trend. However, the HP trend is proven to be a more accurate measure than the other two measures (Ince and Papell 2013). All variables except interest rates are in logarithms. The raw data are combined to construct data for the forecast models7.

4.3. Estimation and Out-of-Sample Forecasting

From one to three months-ahead out-of-sample forecast for USD/NOK, USD/CLP, USD/NZD and USD/MXN exchange rates are generated. The reason for the multistep is to check how the models forecast the exchange rates as the forecast horizon increases. The 16 models in Section 3 are estimated by the ordinary least squared (OLS) using rolling windows (Molodtsova and Papell 2009). In the time-series data, periods 1995M1 to 1999M12 are used for the estimation and the remaining for the out-sample forecast. Thus, the first 60 observations of the time-series data are used to perform the first-month out-of-sample forecast in observation 61. The first data point is dropped, and observation 61 is added in the estimation sample and estimates the model over to forecast observation 62. The process is continued to extract the forecast error vector. A similar procedure is done for the 2 and 3 months-ahead out-of-sample forecast.

4.4. Forecast Assessment Approach

There are different loss functions used in evaluating the out-of-sample forecast. These include mean squared error (MSE), mean absolute error (MAE) and root mean squared error (RMSE) (Meese and Rogoff 1983). MAE is less affected by outliers. RMSE gives a positive root value and is easy to interpret. RMSE has a monotonic transformation and gives the same ordering as the MSE in even the asymptotic test. MSE has a measure of robustness. In this study, the MSE is best suitable for evaluating the forecast since the linear regression model is used. For simplicity, the MSE is referred to as mean squared forecast error (MSFE). This is calculated below:

where yt+τ is the realized value at time t+τ, which in this paper is known as (t+1). is the forecasted value. The difference gives us the error term. T + 1 and P equal the number of sample observations and the number of forecasts, respectively. According to Clark and West (2006), with a random walk, = 0. The exchange rate forecastability is evaluated with the Taylor rule fundamental for Norway, Chile, New Zealand and Mexico by calculating the relative MSFEs (ratio of MSFE). That is, the MSFE of the random walk without drift is divided by the MSFE of the Taylor rule fundamentals model. If the result is greater than 1, then it implies that the Taylor rule fundamentals forecast model has a lower loss function than the random walk. Therefore, the Taylor rule fundamentals could perform better in exchange rate forecasts than the random walk.

4.5. Out-of-Sample Forecast Comparison Method

The significance test of the forecast accuracy of the linear model against the random walk model was proposed by Diebold and Mariano (1995) and West (1996). The DMW test tests for equal accuracy of the benchmark (random walk) and the alternative of linear forecastability (Taylor rule fundamentals) using the mean of their loss functions. This test is suitable for the non-nested models where the variables in one model are not contained in the other models. However, Molodtsova and Papell (2009) believe the forecast Equation (6) is nested and the DMW test could not appropriately be used. That is, if the DMW test is applied, the normal standard critical values would lead to few rejections of the random walk model since the MSFE of the random walk would be smaller than the alternative8. Therefore, Clark and West (2006, 2007) are applied to perform the significance test or the forecast accuracy (check Appendix A for details).

4.6. Directional Accuracy Test

Having tested the significance of the Taylor rule fundamental forecast model, it is important to investigate the directional accuracy of the model. Knowing the correct forecasts about signs of the exchange rate movement is profitable for investors and stock market traders. Moreover, it is of value for the central banks to comprehend the directional changes in the exchange rate to make prudent decisions. The directional accuracy of the forecast is tested in this study by applying the popular nonparametric test developed by Pesaran and Timmerman (1992). The statement of the hypothesis of the Pesaran and Timmerman (PT) test is given as the actual and the forecasted exchange rate values bearing no relationship among them. This implies that the actual and forecasted values are independently distributed; hence, the directional signs could not easily be predicted. The PT test statistics converge to a standard normal distribution. The test statistics have critical values of 1.64 (0.05 test) and 2.33 (0.01 test). Conferring to Brooks (1997) and Clark and West (2006), the forecast of the random walk is always zero; hence, only the directional sign of the Taylor rule fundamentals model is tested.

5. Empirical Test Results

5.1. Stationarity Test (Unit Root Test)

In forecasting, it is relevant to test for stationarity. The exchange rate and the macroeconomics variable or the economic fundamentals in Equation (6) can follow nonstationarity, which may lead to spurious regression. Hence, before the OLS estimation is computed, the Dickey and Fuller (1979) model was used to test for the unit root. The augmented Dickey–Fuller (ADF) test soaks up the autocorrelation so that the error term becomes independently identically distributed white noise. The null hypothesis is a unit root. The decision test is to reject the null hypothesis if the test statistic (z(t)) is less than the critical values. This implies that the regression is stationary and suitable for the model forecast.

In this paper, the unit root test is examined with three models. Model 1 is a time series without both constant and trend. Model 2 tests the unit root in a time series with constant and without trend, because some variables such as exchange rates are expected to be in equilibrium in the long run. In addition, some fundamentals such as the price level and the industrial production level in the forecast equation change with time. Therefore, the ADF tests are modeled with a constant and a time trend (model 3). In total, 35 cases are tested using 90% confidence intervals across the five countries. In 28 out of the 35 cases, the null hypothesis of the unit root is rejected, and in seven cases, the null hypothesis fails to be rejected. The results show that change in the exchange rate (st+1) is stationary in Norway, Chile, New Zealand and Mexico at a 1% significance level. The lag interest rate (it−1) under model 2 is stationary for Chile and Mexico at 5% and 1% significance level, respectively, while it is nonstationary for Norway, New Zealand and the U.S. The inflation rate () is stationary for all the countries with a trend, although the trend is not significant for most of the countries in which the constant happens to be significant.

Moreover, the output gap (yt) is stationary for all the countries at a 1% significant level except for the United States, which is nonstationary. With the real exchange rate (zt), the unit root fails to be rejected for all the countries. The homogeneous models, which are the lag interest rate difference, inflation rate difference and the output gap difference, are shown to be stationary for all the countries. The unit root with lag interest rate difference for New Zealand is rejected with a drift term. In summary, Norway and New Zealand have fundamental variables that have all been stationary except lag interest rate and real exchange rate. Chile and Mexico have fundamental variables that have all been stationary except real exchange, and the U.S. has only the inflation rate as stationary. The nonstationary variables are tested with their first difference, and they turned out to be stationary. However, applying the first difference creates challenges with the interpretation of the result9 (check Table A1 in Appendix B for details). There is enough evidence that the fundamental variables are stationary, and therefore the OLS estimation and forecasting could be performed.

5.2. Taylor Rule Fundamentals Model

The empirical results of the Taylor rule fundamentals models are summarized in Table 1 below, which contains accurate or significant models.

5.2.1. One Month-Ahead Forecast

A one month out-of-sample forecast is performed with the full sample data. A window size of 60 is used for the OLS estimation from 1995M1 to 1999M12. The remaining data are used for the forecasts10. In evaluating the forecast, the relative mean squared forecast error (R.MSFE) is constructed for the random walk without drift model and the Taylor rule fundamentals model. The results in Table A2 in Appendix C show that the R.MSFEs are less than one for the four countries. This means the random walk outperforms the Taylor rule fundamentals when their performances are evaluated with the loss function. This indicates that the exchange rate may be closer to a random walk, and forecast practitioners would not find it easy to beat the random walk (Diebold 2017; Hendry et al. 2019; Engel and West 2005). It is, therefore, imperative to judge forecast based on the model accuracy using the Clark and West (2006, 2007) statistics as discussed in Appendix A.

From Table 1 above, evidence of 11 models is found to accurately forecast the New Zealand exchange rate, seven models for Norway and two models for Mexico. There is no evidence of forecastability for Chile11. Table A2 in Appendix C gives the details of the forecast accuracy for the one month out-of-sample for the 16 models using CW statistics under a rolling window. Strong results are found for the exchange rate forecastability with the models using heterogeneous coefficients. Among the Taylor rule fundamentals, the study finds the strongest evidence of forecastability for symmetric with no interest rate smoothing, heterogeneous coefficients and with a constant (model 7). Model 7 constitutes the inflation rate and output gap as described in the original Taylor rule. Model 7 accurately or significantly outperforms the random walk (null hypothesis) in three out of four countries (Norway at a 1% significance level, New Zealand at a 5% significance level and Mexico at a 10% significance level).

When the real exchange rate is added, a strong performance is observed with its asymmetric model 16, which includes inflation rate, output gap and the real exchange rate. This model is significant for three out of four countries (Norway at a 1% significance level, New Zealand at a 5% significance level and Mexico at a 10% significance level). From Table 1 and Table A2, model 3 (symmetric with interest rate smoothing, heterogeneous coefficients with a constant) and model 12 (asymmetric with interest rate smoothing, heterogeneous coefficients without a constant) also significantly outperform the random walk model. These two models find evidence of the exchange rate forecast in two out of the four countries (Norway, New Zealand at a 1% significance level, respectively).

5.2.2. Until the Financial Crisis

This section answers the following research question: how significant are the Taylor rule fundamentals in forecasting the exchange rate during the global financial crisis and the great recession? The study ensured the findings are not only driven by the selection of the whole sample period. Therefore, the usefulness of the Taylor rule fundamentals for the pre- and post-crisis periods forecasting exchange rates is demonstrated.

To examine the effect of the financial crisis, the sample is adjusted to cover from 1995M1 to 2008M12 and performed the out-of-sample forecast using 60 window size.12 From Table 1, the persistence of the Taylor rule fundamentals forecast accuracy is observed for Norway, New Zealand and Mexico. Again, the Taylor rule models are not significant for Chile. During the period of the 2008 financial crisis, the number of significant models of the Taylor rule fundamentals increased to 14 models for New Zealand. The significant models increased to eight for Mexico, while it remained at seven models for Norway. This means that irrespective of the financial instability in 2008, the Taylor rule fundamentals model was more prescriptive of or more accurately forecasted the exchange rates than the random walk model13. Again, models 7 and 16 strongly outperform the random walk in Norway, New Zealand and Mexico. Even for the forecast evaluation by the relative MSFE, where it is hard to beat the random walk, results in Table A3 in Appendix C show that New Zealand with models (1, 5, 6, 7, and 14), Mexico with models (1, 2, 6, 7, 9, 10, 15, and 16) and Norway with models (2 and 6) perform better than the random walk during the financial crisis.

5.2.3. Post-Financial Crisis

The impact of the Taylor rule fundamentals model on the exchange rate forecasts in the post-financial crisis period is considered. The data sample ranges from 2009M1 to 2019, except for New Zealand which starts from 2009M1 to 2017 due to the unavailability of data14. Though the sample might not be enough for the forecast analysis, the summary result in Table 1 shows that the models have not been significant. There is no significant model for Norway and Chile, and only three models and two models show evidence of forecastability for New Zealand and Mexico, respectively. Details of the CW test statistics are presented in Table A4 in Appendix C. With the forecast evaluation, New Zealand has model 3 outperforming the random walk. While Chile has models 2 and 6 evaluated to perform better than the random walk, they turn out to be insignificant with the CW test. It could be observed that the performance of Taylor rule fundamentals in forecasting the exchange rates has not been effective after the financial crisis.

5.2.4. Two–Three Month’s Out-of-Sample Forecast

To this extent, a one month out-of-sample forecast was used to demonstrate the performance of the Taylor rule fundamentals models. It would be interesting to check how the Taylor rule could be applied to forecast the respective exchange rates in the multi-step ahead. The motivation for this section is to compare the effectiveness of the Taylor rule in forecasting the exchange rates as the forecast horizon increases. Because the paper investigates the short horizon, the analysis is extended to a 2 and 3 months-ahead out-of-sample forecast. However, as discussed in Appendix A, multistep-ahead forecast errors follow a moving average or a serial correlation (Clark and West 2007)15. For a robust regression, the Newey–West estimator with lag 4 is applied to compute the CW inference.

The CW statistics results of the 2 and 3 months-ahead forecasts represented in Table 1 show that none of the 16 models could significantly forecast the exchange rate in Chile and Mexico. Norway has only three significant models (models 7, 12, and 16) for the 2 months-ahead forecasts, and two models (models 7, 16) were significant at a 10% level for the 3 months-ahead forecasts. In addition, New Zealand has just 2 out of the 16 models (models 1 and 3) that were significantly accurate at a 5% level for the 2 months, and only model 3 was accurate at a 5% significant level for 3 months-ahead forecasts (check Table A5 and Table A6 in Appendix C). By and large, the results show that the Taylor rule fundamentals do not accurately forecast the exchange rates in the 2 and 3 months ahead16.

5.3. Directional Accuracy

The directional accuracy is tested using Pesaran and Timmerman (1992). This gives the percentage changes of the exchange rates that were accurately forecasted by the Taylor rule fundamentals models. The PT test is performed on only the one month-ahead forecast because the multistep-ahead forecasts are not significant. Using the full sample data, the PT test results in Table A7 (Appendix C) show that the models could not successfully forecast the directional change for both Norway and Chile exchange rates (only model 14 tests were significant for Norway at 10% level). However, 10 out of the 16 models (models 1, 3, 6, 7, 8, 10, 11, 12, 15, and 16) have strong evidence of forecasting the directional change for the New Zealand exchange rate. New Zealand has at least 50.47% of the directional sign of the exchange rate change accurately forecasted. In addition, for Mexico, four models (models 1, 3, 10, and 12) successfully forecast the directional change. The best performing models are the heterogeneous coefficients models.

To get a clear picture of the directional change of the exchange rates with our Taylor rule fundamentals model, the sample adjustment is considered. The data sample until the financial crisis is used just as it is done for the forecast accuracy. It is observed from the PT test results in Table A8 that the models’ performance in checking the directional change of the exchange rate improved until the financial crisis. At this period, the significance performance of the models for the USD/NZD exchange rate increased to 13 models (except models 4, 11, and 13). The minimum directional accuracy of the New Zealand exchange rate is 55.56%. There are five significant models (models 1, 2, 3, 10, and 12) for the USD/MXN exchange rate and three successful models (models 7, 14, and 16) for the USD/NOK exchange rates. However, the Taylor rule models are again not effective in forecasting the direction of the USD/CLP exchange rate.

From Table A9, the models have not been successful in forecasting the direction of the four exchange rate changes in the post-financial crisis period. The significant models for New Zealand decreased to four models. This shows that the Taylor rule models could not effectively predict the directional change of the exchange rates in the post-financial crisis period. By and large, considering the PT test results, the analysis concludes that the directional accuracy or sign change of the USD/NZD exchange rate could be forecasted by the Taylor rule fundamentals models. The results for the directional accuracy in the case of the USD/MXN exchange rate to some degree are inconclusive.

5.4. Window Sensitivity

Corresponding to Section 4.1, the rolling window size is changed from 60 to 120. That is, the period from 1995M1 to 2004M12 is used for the estimation and the remaining data for the out-of-sample forecast. This helps to investigate the impact of larger window size on the Taylor rule models out-of-sample forecast of the exchange rate. The CW statistics results are summarized in Table 2 below.

From Table 2, an overall reduction in the performance of the Taylor rule fundamentals in forecasting the exchange rates could be observed. When the one month-ahead forecast is performed for the full sample, there is no significant model found for Chile and Mexico. New Zealand has two significant models, and Norway has seven significant models. The best-performing models are heterogeneous coefficients and constants. The strongest evidence of the Taylor rule fundamentals models is model 7 (symmetric with no interest rate smoothing, heterogeneous coefficients and with a constant). This was the same model that performed best when the 60 window size was used for the estimation (check Table A10 in Appendix D for details).

The sample adjustment was examined with the 120 window size. The sample until the financial crisis is used and has no significant evidence of forecastability for Chile and New Zealand. This is interesting because 14 significant models were found for New Zealand with 60 window sizes. The significant models were reduced to five models for Norway and remained at seven models for Mexico (check Table A11 in Appendix D for detail). The post-financial crisis period was examined from 2009M1 to 2019M11. None of the models could significantly outperform the random walk for USD/NOK and USD/NZD exchange rates17. Mexico had two significant models. Chile had eight models significantly outperforming the random walk18 (see Table A12 for details).

The Taylor rule fundamentals out-of-sample forecast for the 2 and 3 months-ahead forecast with the 120 window size was performed. The results in Table A13 and Table A14 in Appendix D show that the models do not significantly outperform the random walk model. Only models 7 and 16 are accurate for the 2 months-ahead forecast for Norway. In addition, the PT test is performed and found no directional accuracy of the USD/CLP and USD/MXN exchange rates. However, four heterogeneous coefficient models show evidence of directional accuracy for the USD/NOK exchange rate at a 10% significant level. Four models significantly evaluate the directional sign of the USD/NZD exchange rate (check Table A15 for details). It gets tougher for the Taylor rule fundamentals model to forecast the directional change of the exchange rate when the larger window size is used. These analyses prove that the choice of window size selection affects the forecast outcome of the models. It is observed that the smaller window size (60 observations) influences the Taylor rule fundamentals models to forecast the exchange rate better than with the larger window size (120 observations).

6. Economic Analysis and Discussions

Taylor (1993) presents monetary policy rules that describe the interest rate decisions of the Federal Reserve’s Federal Open Market Committee (FOMC). The Taylor rule specifies the short-run interest rate response to changes in the inflation rate and the output gap. Molodtsova and Papell (2009) derived the Taylor rule fundamentals by subtracting the Taylor rule of the foreign countries from the Taylor rule of the domestic country (U.S.) with some model specifications. They had their strongest evidence coming from the specifications that included heterogeneous coefficients and interest rate smoothing.

In this paper, similar specifications were used with 16 different models to examine how the Taylor rule fundamentals could be applied to forecast the exchange rates. The study used four OECD countries (Norway, Chile, New Zealand and Mexico) vis-à-vis the U.S. When the out-of-sample forecast for the full sample with the loss function was evaluated, the Taylor rule fundamentals models could not outperform the random walk without drift. This is a stylized fact in a forecast in which the random walk is hard to beat (Diebold 2017; Hendry et al. 2019). It implies that the noise surrounding the Taylor models is little, but if the wrong model is selected for the out-of-sample forecast, it would produce a big error that would overcompensate the decreased size of the noise. Then, the random walk would perform better than the linear model. Therefore, the significance of the Taylor rule fundamentals models is investigated by testing their forecast accuracy with the Clark and West (2006, 2007) statistics.

The strongest evidence comes from the models with heterogeneous coefficients, which is consistent with the result of Molodtsova and Papell (2009). The most performing model based on the empirical result analysis is model 7, which incorporates symmetric with no interest rate smoothing and heterogeneous coefficients with a constant. This implies that the inflation rate and output gap influence the changes in the exchange rates. The heterogeneous coefficient means that the Fed and the foreign central banks respond differently to change in the inflation rate and the output gap. The constant shows that the central banks do not have the same target inflation rates and equilibrium real interest rates. In addition, the symmetric model explains that the Fed and the foreign central banks follow the same Taylor rule model. When the real exchange rate is added to the models (asymmetric), the performance was again boosted. This shows that the central banks react to the adjustment of PPP, which influences the exchange rate movements.

The financial crisis causes a structural break in the sample data. Therefore, the coefficients might not be constant over time, and the model could favor the short-run period. Nikolsko-Rzhevskyy et al. (2014) test for multiple structural changes to examine the economic performance of the Taylor rule. In this study, the sample data are adjusted to cover the financial crisis and the great recession and realized evidence of exchange rate forecastability with the Taylor rule fundamentals models19. The interest rate data show that until the 2008 financial crisis, the central banks adjusted their interest rates to control inflation. Hence, the monetary policy became very active as the central banks followed the Taylor rule descriptions.

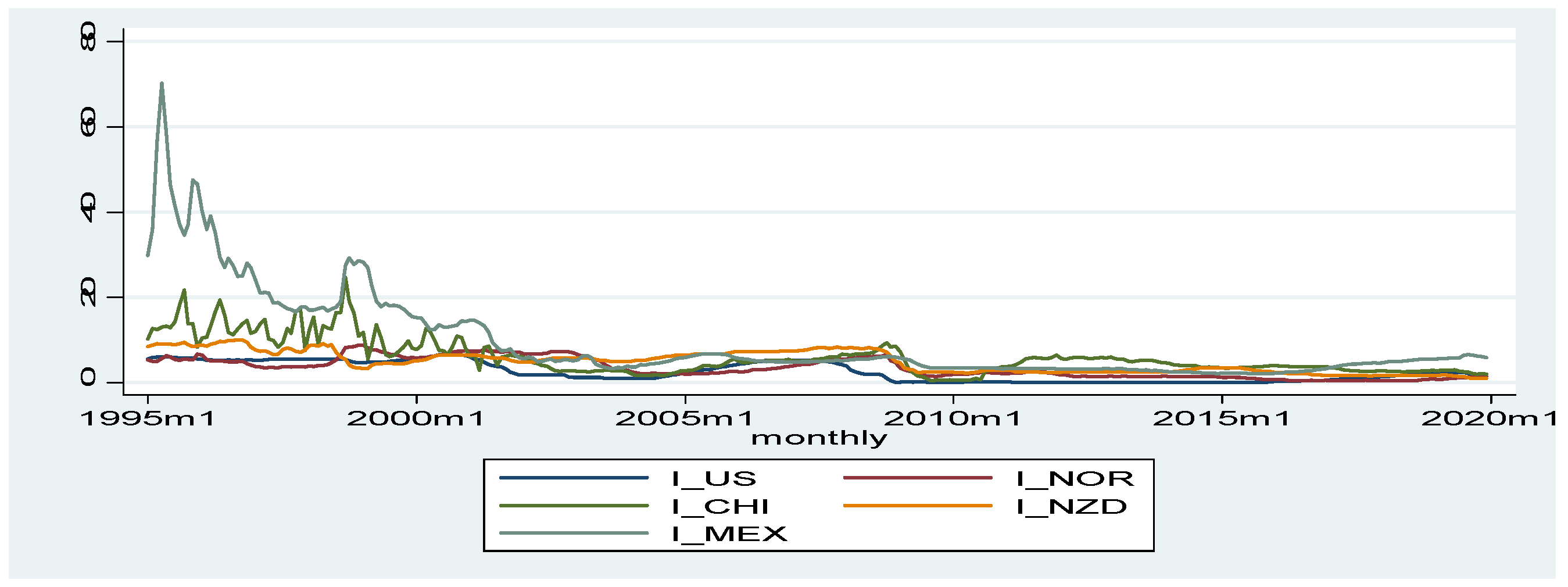

However, in the post-financial crisis period, the Taylor rule fundamentals could not forecast the exchange rate better than the random walk. The Fed lowered the interest rate to zero lower bound. Norway’s interest rate also decreased close to the lower bound. In 2019, New Zealand lowered the interest rate to 1%. Mexico experienced a 3% interest rate from 2013 to 2015, and it increased to 4.5% in 2019. Chile’s interest rate declined to 0.5% in 2009, increased after 2010 to 5% and then decreased after 2012 to 1.75% (check Figure 2). From the empirical analysis, the Taylor rule lost its efficacy in forecasting the exchange rates after the financial crisis because the interest rates hit the zero lower bound.

Taylor (2015) explained during the 2015 IMF conference that the Fed has not adhered to the prescription of the Taylor rule. This rendered the monetary policy as being passive. Most central banks set short-term interest rates to a zero lower bound (ZLB) in response to the financial crisis and have adopted quantitative easing or large-scale asset purchases (balance sheets) to pursue their policies. For the Taylor rule fundamentals to be more descriptive, the study suggests that the central banks control the interest rate lower bound. Following Ben S. Bernanke’s (2015) presentation at the 2015 IMF conference, the Fed could also devise a monetary policy that would increase the inflation target, targeting the price level and targeting the output gap. If these variables are controlled by the central banks, the models would forecast the exchange rate better in the post-financial crisis period. In addition, Bernanke (2015) suggests mix monetary and proactive fiscal policies as they would ideally control the zero lower bound interest rate.

The empirical results in this paper also depict that policymakers could not accurately apply the Taylor rule fundamentals to forecast the USD/NOK, USD/CLP, USD/NZD and USD/MXN in the 2 and 3 months ahead. The model is significant in only the one month-ahead out-of-sample forecast.

Furthermore, central banks and asset managers or investors are usually interested in knowing the directional signs of the exchange rate in the market, as it equips them to efficiently and strategically decide either to sell or buy a security. The exchange rate directional accuracy was tested by applying the Pesaran and Timmerman (1992) test. The results show that the Taylor rule fundamentals models could accurately forecast the directional change of the USD/NZD exchange rate. This means that, other things equal, investing in New Zealand is more profitable compared to the other three countries since investors could forecast the exchange rate changes. The success of the directional accuracy of the New Zealand exchange rate change has a minimum of 50.47%. Except after the financial crisis where the Taylor rule has not been effective, Mexico’s exchange rate has a potential for directional accuracy considering the PT test results. However, the PT test results for Norway and Chile depict difficulties in evaluating the directional exchange rate changes in these two economies.

7. Conclusions

In this research, the out-of-sample forecast is used to examine the application of the Taylor rule fundamentals in forecasting the exchange rates. To this end, an inference can be made that for the whole sample data, the Taylor rule fundamentals significantly forecast the exchange rates at the 1 month ahead using the Clark and West (2006, 2007) test. However, at the 2 and 3 months-ahead forecast horizon, weak evidence of exchange rates forecastability is realized with the Taylor rule fundamentals models against the random walk in the four countries. The best-performing model is symmetric with no interest rate smoothing and heterogeneous coefficients with a constant.

Taylor rule fundamentals models perform better in forecasting the exchange rates until the financial crisis. The Taylor rules’ performance is observed to be insignificant in the post-financial crisis. This could be attributed to interest rates approaching the zero lower bound. Moreover, the study showed that the models’ performance is sensitive to changes in the window size. The models perform better with small window size than with larger window size. New Zealand was the best-performing country and Chile the worst. It means that Chile slightly follows the Taylor rule for its monetary policy (Moura and de Carvalho 2010; Moura 2010). For directional accuracy, the PT test demonstrates results in favor of the USD/NZD and USD/MXN exchange rates.

By and large, this study provides evidence of exchange rate forecastability with the Taylor rule fundamentals using the CW test statistics. However, the Taylor rule fundamentals do not put the estimated coefficients on the Taylor rule variables. Rather, the models only examine out-of-sample forecastability (Ince et al. 2016). Therefore, further investigation into the connection between the Fed using the Taylor rule and the out-of-sample exchange rate forecastability is needed. Given the experience that the Taylor rule has not been effective since after the 2008 financial crisis, there is also a need for a broader approach such as the use of a balance sheet of the central banks.

Funding

This research received no external funding.

Data Availability Statement

The data presented in this study are available publicly. All sources are cited in the study.

Acknowledgments

The author appreciates Stefan Reitz for his indelible supervision and immeasurable support.

Conflicts of Interest

The author declares no conflict of interest.

Appendix A. Clark and West (CW) Test

The Clark and West (2006, 2007) test uses simulations to show the existence of linear forecastability in a given series, contrary to the null hypothesis that the series follows a martingale sequence or difference (also known as a random walk). They compare the out-of-sample MSFE of the random walk and the alternative of linear forecastability.

Model 1 is the parsimonious model (null model of random walk).

Model 2 is the nested large model (alternative model).

Given a linear regression as

where yt is a dependent variable whose interest we want to predict (expected nominal exchange rate); Xt’ is a vector of variables; and et is the error term. Clark and West state under the null hypothesis that β = 0 and under the alternative hypothesis that β 0. They assume that under both hypotheses a martingale difference exists. This gives the conditional expectations of the errors being zero: Et−1et E(et|Xt, et−1, Xt−1, et−2,…) = 0

yt = βXt’ + et

Let denotes the forecasts of model 1 at period t of .

Where denotes the forecasts of model 2 at period t of . is the forecast horizon, and is our actual value which is used as st+1 in our analysis.

Model 1 errors equal ( − ), and model 2 errors equal ( − )

Clark and West (2006, 2007) solve the nested problem associated with the DMW test by introducing an adjustment term (adj).

This gives the differences between the MSFE of the alternative hypothesis and the new adjustment term as (MSFE2 − adj). Hence, Clark and West test the null hypothesis of equal MSFE.

After some computations:

The mean then becomes:

Clark and West (2006) states that if the test is against a random walk, the forecast of model 1 is just a constant value of zero, such that equals zero. Therefore, the MSFE1 becomes the sample mean squared of the actual value (st+1). Thus, MSFE1 = P−1 2. After some computation,

We then arrive at the test statistics:

For the one month-ahead forecast, the normal OLS standard error could be applied, since the forecast errors are white noise. However, Clark and West (2006, 2007) state that as the forecast horizon increases, there would be overlapping in the data in forecasting —steps ahead. Therefore,

According to Clark and West, the time series follows a moving average ( − 1). That means there would be a serial correlation in the residuals. To solve this problem, Clark and West propose regressing a Newey–West robust variance estimator (Newey and West 1987) on. This results in t = 2yt(). The sample mean becomes.

Consistent sample variance,

Decision rule:

Clark and West’s statistics follow a one-sided test that captures only the upper tail. This implies that if the test statistic is greater than +1.282 (0.10 test) or +1.645 (0.05 test), we reject the null hypothesis of a random walk model.

Appendix B. Stationarity Test (Augmented Dickey–Fuller Test)

{kind=link}

{kind=link}

Table A1.

Unit root test with ADF.

| Norway | Chile | New Zealand | Mexico | U.S | ||||||

|---|---|---|---|---|---|---|---|---|---|---|

| M | T-Stat | M | T-Stat | M | T-Stat | M | T-Stat | M | T-Stat | |

| st+1 | 2 | −11.046 *** | 2 | −11.944 *** | 2 | −10.044 *** | 2 | −13.660 *** | - | - |

| it−1 | 2 | −1.394 | 2 | −3.188 ** | 2 | −1.536 | 2 | −3.533 *** | 2 | −1.616 |

| t | 3 | −5.497 *** | 3 | −3.348 * | 3 | −3.240 * | 3 | −3.503 ** | 3 | −5.073 *** |

| yt | 3 | −5.635 *** | 3 | −12.589 *** | 3 | −10.567 *** | 3 | −4.561 *** | 3 | −2.957 |

| zt | 2 | −1.713 | 2 | −1.830 | 2 | −1.546 | 2 | −2.568 | - | - |

| it−1 − it−1* | 1 | −1.972 * | 2 | −4.402 *** | Drift | −2.007 ** | 2 | −3.910 *** | - | - |

| t − πt* | 3 | −4.306 *** | 2 | −3.347 ** | 3 | −3.567 ** | 1 | −2.534 ** | - | - |

| yt − yt* | 3 | −6.109 *** | 3 | −13.307 *** | 3 | −10.118 *** | 3 | −5.091 *** | - | - |

| zt(D) | 2 | −11.240 *** | 2 | −12.579 *** | 2 | −10.727 *** | 2 | −11.807 *** | - | - |

| it−1(D) | 2 | −8.737 *** | 2 | −14.847 *** | 2 | −8.104 *** | 2 | −13.135 *** | 2 | −5.980 *** |

This table displays the stationarity results for the variables found in Equation (6). The augmented Dickey–Fuller is used to test the null hypothesis of a unit root (left-sided hypothesis). The decision test is that if the test statistic (zt) is less than the critical value at either 1%, 5% and 10% significant level, and the null hypothesis is rejected. ***, ** and * mean the variable is stationary at 1%, 5% and 10% significant levels, respectively. The columns with M represent the model used for the stationarity test. Testing with model 1 shows that no constant, and no trend is added to the regression equation. Constant but no trend in the regression is explained by model 2. This implies that the fundamental variables are expected to move to equilibrium in the long run. Model 3 shows that we run the ADF test with both constant and trend since some of the variables such as prices and industrial production can change over time. zt(D) and it−1(D) represent the first difference of the real exchange rate and the lag interest rate, respectively.

Appendix C. Out-of-Sample Forecast with 60 Window Size

Table A2.

One month-ahead forecasts using Taylor rule fundamentals with 60 window size.

| Model | Norway | Chile | New Zealand | Mexico | ||||

|---|---|---|---|---|---|---|---|---|

| R.MSFE | T-Stat | R.MSFE | T-Stat | R.MSFE | T-Stat | R.MSFE | T-Stat | |

| 1 | 0.8982 | 0.8192 | 0.8529 | −0.3793 | 0.9868 | 3.1196 *** | 0.9324 | 1.3117 * |

| 2 | 0.9244 | 0.9753 | 0.8904 | −0.6690 | 0.9163 | 0.7625 | 0.9221 | 0.0089 |

| 3 | 0.8834 | 2.5139 *** | 0.7563 | 0.5004 | 0.8964 | 3.5655 *** | 0.7891 | 0.9487 |

| 4 | 0.8329 | 1.3197 * | 0.7602 | −0.3995 | 0.8504 | 1.4779 * | 0.7849 | −1.0651 |

| 5 | 0.9247 | 0.6476 | 0.9434 | −0.4662 | 0.9507 | 0.8869 | 0.9273 | 0.0639 |

| 6 | 0.9649 | 0.9933 | 0.9617 | −0.5418 | 0.9779 | 1.3359 * | 0.9491 | −0.3468 |

| 7 | 0.9637 | 3.2694 *** | 0.8496 | 0.0465 | 0.9321 | 2.1055 ** | 0.9134 | 1.3351 * |

| 8 | 0.8715 | 0.6963 | 0.8526 | −0.9668 | 0.9105 | 1.4001 * | 0.8935 | −0.9495 |

| 9 | 0.8257 | −0.8020 | 0.8435 | −0.3542 | 0.9288 | 2.1614 ** | 0.9085 | 0.9310 |

| 10 | 0.8993 | 0.8944 | 0.8546 | −0.3696 | 0.9207 | 2.2608 ** | 0.9298 | 1.2328 |

| 11 | 0.8444 | 1.6622 ** | 0.7340 | −0.3737 | 0.8345 | 2.6262 *** | 0.7408 | 0.4761 |

| 12 | 0.8981 | 2.6203 *** | 0.7598 | 0.5393 | 0.8375 | 2.3610 *** | 0.7781 | 1.0582 |

| 13 | 0.8781 | −0.2905 | 0.8826 | −1.2108 | 0.8767 | −0.9117 | 0.9167 | 0.0532 |

| 14 | 0.9255 | 0.6613 | 0.9429 | −0.4715 | 0.9517 | 0.9092 | 0.9265 | 0.0717 |

| 15 | 0.9065 | 2.0943 ** | 0.8003 | −1.1445 | 0.8441 | 0.9267 | 0.8821 | 0.3895 |

| 16 | 0.9656 | 3.2811 *** | 0.8505 | 0.0575 | 0.8948 | 1.9619 ** | 0.9161 | 1.3074 * |

Table A2 presents the relative mean squared forecast error (R.MSFE) and the test statistics of Clark and West statistics for a 1 month-ahead out-of-sample forecast for the full sample from 1995 M1 to 2019M11. The random walk without drift is used as the null hypothesis where the alternative hypothesis is a linear model with the Taylor rule fundamentals. The OLS estimation is performed using a rolling regression with 60 window size from 1995 M1 to 1999 M12 and the remaining sample for the out-of-sample forecast. For Norway, Chile and Mexico, the number of observations (T + 1) is 299, and the number of forecasts (P) is 239. However, due to the unavailability of data for New Zealand, (T + 1) = 274 and P = 214. R.MSFE above 1 indicates that the alternative model outperforms the random walk. CW is a standard normal with a one-sided test, and it tests the significance and accuracy of the alternative model. ***, ** and * show that the random walk is rejected at 1%, 5% and 10% significance level, respectively.

Table A3.

Taylor rule fundamentals forecast until the financial crisis with 60 window size.

| Model | Norway | Chile | New Zealand | Mexico | ||||

|---|---|---|---|---|---|---|---|---|

| R.MSFE | T-Stat | R.MSFE | T-Stat | R.MSFE | T-Stat | R.MSFE | T-Stat | |

| 1 | 0.9130 | 0.8512 | 0.8389 | −0.0752 | 1.0111 | 2.3596 *** | 1.0087 | 1.9035 ** |

| 2 | 1.0129 | 1.8783 ** | 0.8536 | −0.5864 | 0.9819 | 1.9450 ** | 1.0355 | 2.0877 ** |

| 3 | 0.9449 | 1.6752 ** | 0.7362 | 0.1460 | 0.9616 | 2.0835 ** | 0.9746 | 1.6280 * |

| 4 | 0.8462 | 1.0371 | 0.6939 | −0.1092 | 0.9352 | 1.8031 ** | 0.9606 | 0.8050 |

| 5 | 0.9354 | 0.7297 | 0.9147 | −0.4414 | 1.0144 | 2.2626 ** | 0.9956 | 0.8469 |

| 6 | 1.0066 | 1.7160 ** | 0.9398 | −0.6915 | 1.0465 | 2.8568 *** | 1.0390 | 1.5825 * |

| 7 | 0.9861 | 2.3374 *** | 0.7856 | −1.2723 | 1.0178 | 1.8237 ** | 1.0109 | 1.8679 ** |

| 8 | 0.9010 | 1.1180 | 0.7763 | −0.9972 | 0.9571 | 2.0061 ** | 0.9705 | 0.6645 |

| 9 | 0.8530 | −0.6033 | 0.9342 | −0.0923 | 0.9407 | 1.4517 * | 1.0245 | 1.1560 |

| 10 | 0.9139 | 0.8741 | 0.8406 | −0.0605 | 0.9853 | 2.1143 ** | 1.0100 | 1.9186 ** |

| 11 | 0.9389 | 1.1637 | 0.7254 | −1.1851 | 0.8903 | 1.2233 | 0.9328 | 0.6491 |

| 12 | 0.9793 | 1.8889 ** | 0.7406 | 0.1703 | 0.8890 | 1.4653 * | 0.9842 | 1.7114 ** |

| 13 | 0.9159 | 0.0625 | 0.8477 | −1.5401 | 0.9282 | 0.4731 | 0.9871 | 0.3743 |

| 14 | 0.9361 | 0.7205 | 0.9142 | −0.4438 | 1.0163 | 2.2849 ** | 0.9961 | 0.8554 |

| 15 | 0.9638 | 1.4798 * | 0.7407 | −2.4105 | 0.9787 | 1.3009 * | 1.0178 | 1.0772 |

| 16 | 0.9928 | 2.3920 *** | 0.7864 | −1.2923 | 0.9434 | 1.4581 * | 1.0200 | 1.8680 ** |

This table presents the relative mean squared forecast error (R.MSFE) and the test statistics of Clark and West (CW) statistics for a 1 month-ahead out-of-sample forecast for the period until the financial crisis and the great recession. The sample covers from 1995 M1 to 2008 M12. The random walk without drift is used as the null hypothesis where the alternative hypothesis is a linear model with the Taylor rule fundamentals. The OLS estimation is performed using a rolling regression with 60 window size from 1995 M1 to 1999 M12 and the remaining sample for the out-of-sample forecast. For Norway, Chile, New Zealand and Mexico, the number of observations (T + 1) is 168, and the number of forecasts (P) is 108. R.MSFE above 1 indicates that the alternative model outperforms the random walk. CW is a standard normal with a one-sided test, and it tests the significance and accuracy of the alternative model. ***, ** and * show that the random walk is rejected at 1%, 5% and 10% significance level, respectively.

Table A4.

Taylor rule fundamentals forecast in the post-financial crisis with 60 window size.

| Model | Norway | Chile | New Zealand | Mexico | ||||

|---|---|---|---|---|---|---|---|---|

| R.MSFE | T-Stat | R.MSFE | T-Stat | R.MSFE | T-Stat | R.MSFE | T-Stat | |

| 1 | 0.8985 | −0.0223 | 0.8684 | −0.6357 | 0.9087 | 1.6652 ** | 0.9811 | 1.4600 * |

| 2 | 0.8756 | −0.9647 | 1.0034 | 0.9318 | 0.9215 | −1.9769 | 0.8728 | −1.0589 |

| 3 | 0.7832 | 0.5816 | 0.7355 | −0.8177 | 1.1478 | 2.8820 *** | 0.7222 | 0.4526 |

| 4 | 0.8367 | 0.0172 | 0.8238 | −0.719 | 0.8205 | 0.6305 | 0.6978 | −1.7000 |

| 5 | 0.9562 | 0.5537 | 0.9890 | 0.6090 | 0.9158 | −1.6638 | 0.9187 | −0.1533 |

| 6 | 0.9629 | −0.9979 | 1.0016 | 0.9312 | 0.9553 | −0.7282 | 0.9290 | −1.083 |

| 7 | 0.8754 | −0.1025 | 0.9388 | −0.3689 | 0.8219 | −1.4401 | 0.9228 | 0.7682 |

| 8 | 0.9059 | 0.4585 | 0.9470 | −0.2228 | 0.9272 | −0.0414 | 0.8678 | −2.6233 |

| 9 | 0.7626 | −0.5391 | 0.8774 | −0.6870 | 0.7730 | 0.6323 | 0.8473 | 0.2281 |

| 10 | 0.9004 | 0.1153 | 0.8720 | −0.6895 | 0.8014 | −0.1290 | 0.9733 | 1.3052 * |

| 11 | 0.7272 | −0.3102 | 0.7325 | -0.5015 | 0.9318 | 1.8273 ** | 0.6055 | 0.1523 |

| 12 | 0.7873 | 0.6003 | 0.7391 | −0.8850 | 0.8374 | 1.2645 | 0.6898 | 0.4658 |

| 13 | 0.8285 | −0.0407 | 0.8794 | −0.2763 | 0.7878 | −2.2377 | 0.8658 | −0.3735 |

| 14 | 0.9530 | 0.5297 | 0.9879 | 0.5823 | 0.9245 | −1.4380 | 0.9172 | −0.1245 |

| 15 | 0.8084 | −0.1346 | 0.8172 | −0.5581 | 0.6991 | −2.2012 | 0.8026 | −0.5160 |

| 16 | 0.8670 | −0.1669 | 0.9365 | −0.4199 | 0.8463 | −1.1448 | 0.9185 | 0.6142 |

This table reports the relative mean squared forecast error (R.MSFE) and the test statistics of Clark and West statistics for a 1 month-ahead out-of-sample forecast for the period after the financial crisis. The sample runs from 2009 M1 to 2019M11. The random walk without drift is used as the null hypothesis where the alternative hypothesis is a linear model with the Taylor rule fundamentals. The OLS estimation is performed using a rolling regression with 60 window size from 2009 M1 to 2013 M12 and the remaining sample for the out-of-sample forecast. For Norway, Chile and Mexico, the number of observations (T + 1) is 131, and the number of forecasts (P) is 71. However, due to the unavailability of data for New Zealand, (T + 1) = 106 and P = 46. R.MSFE above 1 indicates that the alternative model outperforms the random walk. CW is a standard normal with a one-sided test, and it tests the significance and accuracy of the alternative model. ***, ** and * show that the random walk is rejected at 1%, 5% and 10% significance level, respectively.

Table A5.

Two months-ahead forecasts using Taylor rule fundamentals with 60 window size.

| Model | Norway | Chile | New Zealand | Mexico | ||||

|---|---|---|---|---|---|---|---|---|

| R.MSFE | T-Stat | R.MSFE | T-Stat | R.MSFE | T-Stat | R.MSFE | T-Stat | |

| 1 | 0.8095 | −0.9226 | 0.7973 | −1.0027 | 0.9152 | 1.7413 ** | 0.8888 | 0.5754 |

| 2 | 0.8692 | −0.0550 | 0.8420 | −1.2095 | 0.8583 | −0.2475 | 0.8922 | −0.6344 |

| 3 | 0.7399 | 1.0431 | 0.6466 | −0.1134 | 0.7361 | 1.9249 ** | 0.6468 | −0.8145 |

| 4 | 0.7056 | −0.9817 | 0.6342 | −1.3666 | 0.7275 | 0.0013 | 0.7016 | −2.4359 |

| 5 | 0.8601 | −0.5850 | 0.9169 | −1.0181 | 0.8989 | −0.1538 | 0.8972 | −0.6623 |

| 6 | 0.9354 | 0.3380 | 0.9394 | −1.1774 | 0.9388 | 0.4637 | 0.9300 | −0.7510 |

| 7 | 0.8710 | 1.7787 ** | 0.7573 | −1.0310 | 0.8217 | 0.6960 | 0.8389 | −0.3220 |

| 8 | 0.7893 | −1.0326 | 0.7677 | −1.4836 | 0.7995 | 0.0367 | 0.8543 | −1.7698 |

| 9 | 0.7268 | −2.5201 | 0.7641 | −0.4412 | 0.8270 | 0.4461 | 0.8469 | 0.1555 |

| 10 | 0.8095 | −0.8510 | 0.7998 | −0.9923 | 0.8392 | 0.9762 | 0.8875 | 0.5153 |

| 11 | 0.6732 | 0.2553 | 0.5868 | −0.4163 | 0.6428 | 1.0762 | 0.5635 | −1.2967 |

| 12 | 0.7526 | 1.2942 * | 0.6519 | −0.0551 | 0.6598 | 0.5047 | 0.6255 | −0.7125 |

| 13 | 0.7938 | −1.7760 | 0.8391 | −1.2078 | 0.8034 | −1.8932 | 0.8677 | −0.8523 |

| 14 | 0.8615 | −0.5556 | 0.9164 | −1.0272 | 0.9000 | −0.1150 | 0.8968 | −0.6373 |

| 15 | 0.7857 | 1.0447 | 0.7010 | −1.3586 | 0.7087 | −0.3285 | 0.7921 | −1.4813 |

| 16 | 0.8728 | 1.8382 ** | 0.7587 | −1.0201 | 0.7782 | 0.4674 | 0.8404 | −0.3776 |

This table presents the relative mean squared forecast error (R.MSFE) and the test statistics of Clark and West statistics for a 2 months-ahead out-of-sample forecast for the full sample from 1995 M1 to 2019M11. The random walk without drift is used as the null hypothesis where the alternative hypothesis is a linear model with the Taylor rule fundamentals. The estimation is performed using a rolling regression with 60 window size from 1995 M1 to 1999 M12 and the remaining sample for the out-of-sample forecast. The serial correlation is checked using the Newey–West estimator with lag 4. For Norway, Chile and Mexico, the number of observations (T + 1) is 299, and the number of forecasts (P) is 239. However, due to the unavailability of data for New Zealand, (T + 1) = 274 and P = 214. R.MSFE above 1 indicates that the alternative model outperforms the random walk. CW is a standard normal with a one-sided test, and it tests the significance and accuracy of the alternative model. ** and * show that the random walk is rejected at 5% and 10% significance level, respectively.

Table A6.

Three months-ahead forecasts using Taylor rule fundamentals with 60 window size.

| Model | Norway | Chile | New Zealand | Mexico | ||||

|---|---|---|---|---|---|---|---|---|

| R.MSFE | T-Stat | R.MSFE | T-Stat | R.MSFE | T-Stat | R.MSFE | T-Stat | |

| 1 | 0.7936 | −1.0581 | 0.7825 | −0.9523 | 0.8749 | 1.2196 | 0.9050 | 1.2010 |

| 2 | 0.8558 | −0.3015 | 0.8308 | −1.1224 | 0.8181 | −0.8687 | 0.9050 | −0.2514 |

| 3 | 0.7061 | 0.6939 | 0.5964 | −0.0274 | 0.6735 | 1.9382 ** | 0.6213 | 0.1006 |

| 4 | 0.6741 | −1.2309 | 0.5927 | −1.3343 | 0.6825 | −0.3268 | 0.7119 | −1.6080 |

| 5 | 0.8400 | −0.8240 | 0.9112 | −1.1327 | 0.8695 | −0.6967 | 0.9062 | −0.3429 |

| 6 | 0.9278 | 0.2569 | 0.9366 | −1.2529 | 0.9185 | 0.0806 | 0.9372 | −0.4941 |

| 7 | 0.8426 | 1.4340 * | 0.7316 | −1.1514 | 0.7888 | 0.3984 | 0.8457 | 0.1092 |

| 8 | 0.7664 | −1.1463 | 0.7419 | −1.6913 | 0.7639 | −0.1768 | 0.8774 | −1.2281 |

| 9 | 0.7011 | −2.3364 | 0.7799 | 0.3491 | 0.7788 | −0.2020 | 0.8672 | 1.2043 |

| 10 | 0.7932 | −0.9875 | 0.7876 | −0.9218 | 0.7909 | 0.3491 | 0.9043 | 1.1360 |

| 11 | 0.6040 | 0.0915 | 0.5238 | −0.3922 | 0.5386 | 0.7354 | 0.5170 | −0.1280 |

| 12 | 0.7165 | 0.9625 | 0.6044 | 0.0806 | 0.5860 | −0.0114 | 0.5910 | 0.1893 |

| 13 | 0.7667 | −1.7693 | 0.8304 | −1.1784 | 0.7675 | −2.0489 | 0.8869 | 0.1127 |

| 14 | 0.8420 | −0.7888 | 0.9103 | −1.1429 | 0.8705 | −0.6441 | 0.9065 | −0.3069 |

| 15 | 0.7315 | 0.7575 | 0.6639 | −1.1044 | 0.6324 | −0.7536 | 0.8108 | −0.1792 |

| 16 | 0.8440 | 1.5029 * | 0.7320 | −1.1299 | 0.7409 | 0.1582 | 0.8487 | 0.1066 |

This table presents the relative mean squared forecast error (R.MSFE) and the test statistics of Clark and West statistics for a 3 months-ahead out-of-sample forecast for the full sample from 1995 M1 to 2019M11. The random walk without drift is used as the null hypothesis where the alternative hypothesis is a linear model with the Taylor rule fundamentals. The estimation is performed using a rolling regression with 60 window size from 1995 M1 to 1999 M12 and the remaining sample for the out-of-sample forecast. The serial correlation is checked using the Newey–West estimator with lag 4. For Norway, Chile and Mexico, the number of observations (T + 1) is 299, and the number of forecasts (P) is 239. However, due to the unavailability of data for New Zealand, (T + 1) = 274 and P = 214. R.MSFE above 1 indicate that the alternative model outperforms the random walk. CW is a standard normal with a one-sided test, and it tests the significance and accuracy of the alternative model. ** and * show that the random walk is rejected at 5% and 10% significance level, respectively.

Table A7.

Directional accuracy test using Taylor rule fundamentals with 60 window size.

| Model | Norway | Chile | New Zealand | Mexico | ||||

|---|---|---|---|---|---|---|---|---|

| PT p-Value | Directional Accuracy | PT p-Value | Directional Accuracy | PT p-Value | Directional Accuracy | PT p-Value | Directional Accuracy | |

| 1 | 0.3523 | 51.05% | 0.4806 | 50.21% | 0.0020 | 59.81% *** | 0.0255 | 55.65% ** |

| 2 | 0.7992 | 47.28% | 0.4813 | 50.21% | 0.1592 | 53.27% | 0.4249 | 50.63% |

| 3 | 0.6699 | 48.54% | 0.4226 | 50.63% | 0.0002 | 62.15% *** | 0.0080 | 57.74% *** |

| 4 | 0.1386 | 53.56% | 0.5817 | 49.37% | 0.1364 | 53.74% | 0.3751 | 51.05% |

| 5 | 0.1384 | 5356% | 0.5282 | 49.79% | 0.1782 | 53.27% | 0.5926 | 49.37% |

| 6 | 0.4239 | 50.63% | 0.4753 | 50.21% | 0.0341 | 56.07% ** | 0.8404 | 46.86% |