The Role of Institutional Investors in Improving Board of Director Attributes around the World

Business Studies Department, University of Technology and Applied Sciences-Shinas, Al-Aqur, P.O. Box 77, Shinas 324, Oman

J. Risk Financial Manag. 2021, 14(4), 166; https://doi.org/10.3390/jrfm14040166

Submission received: 2 February 2021

/

Revised: 29 March 2021

/

Accepted: 29 March 2021

/

Published: 6 April 2021

(This article belongs to the Special Issue Corporate Governance and Its Impact on Accounting and Finance)

Abstract

:This paper investigates the role of institutional investors in the improvement of corporate governance for the companies in which they invest (investee companies) using evidence about the attributes of boards of directors across 15 countries. Furthermore, this paper examines the extent to which the activism of institutional investors is determined by the institutional environment, to include various economic conditions (pre-crisis, crisis and post-crisis), legal systems and ownership structures. Drawing from the agency theory and institutional theory, the results show that foreign institutional investors are the main promoters of board governance structures across the globe. This study also provides evidence that institutional investors promote the independence of a board and its audit and compensation sub-committees (but excluding its nomination committee). The study also demonstrates that institutional investors reduce board entrenchment, though it presents no evidence that institutional investors reduce board busyness. The results also suggest that institutional investors behave differently when operating within different economic conditions (pre-crisis, crisis and post-crisis), legal systems and ownership structures. This paper contributes to the growing literature on shareholder activism and comparative corporate governance mechanisms. The findings suggest that the activism of institutional investors is contingent on the institutional settings, to include economic conditions, legal systems and ownership structures.

1. Introduction

Institutional investors maintain a notable presence and exercise growing influence over global capital markets. The increasing growth of their worldwide investments affords them the potential to influence the behavior of investee firms through their monitoring activities (Aggarwal et al. 2011; Gillan and Starks 2003; Mallin 2016). Generally, institutional investors who are dissatisfied with company performance or with the governance structure of an organization may choose to sell their company shares (“exit”) or opt to engage with their investee firms (“voice”) (Ferreira and Matos 2008; Martin et al. 2007). Since the “exit” option is considered costly, large institutional investors choose to engage with their investee firms in order to change unfavorable governance structures and to correct undesirable performance (McCahery et al. 2015; McNulty and Nordberg 2016). The engagement between institutional investors and their investee firms can assume many forms, such as one-to-one meetings, voting, shareholder proposals and resolutions, focus lists and corporate governance rating systems (Mallin 2016; Martin et al. 2007). In addition, behind-the-scenes one-to-one meetings may be held; such meetings are considered an effective approach that is regularly used by institutional investors to enhance the governance structure of their investee firms (Holland 1998; McCahery et al. 2015). Moreover, the stewardship codes and guidelines issued by several institutions in various countries are a significant move towards improved interactions between institutional investors and their investee firms, as they aim to promote positive governance structures (Haxhi et al. 2013; McNulty and Nordberg 2016). More recently, several studies have also found that the institutional investors have the ability to play an effective role in enhancing corporate governance mechanism in a stakeholders-oriented corporate governance system like Japan (Sakawa and Watanabel 2020; Sakawa et al. 2021).

The corporate board is considered to be the main governing mechanism that mitigates the agency costs that arise from the separation of ownership and control (Fama and Jensen 1983). Given that the board exists as the nucleus of decision making processes, great attention has been paid to its attributes (Solomon 2010; Mallin 2016). Regarding the importance that the corporate board attributes hold for institutional investors, Useem et al. (1993) have provided evidence that the composition and functionality of the board are crucial considerations for US-based institutional investors. Furthermore, following a global survey of 200 institutional investors, Coombes and Watson (2000) have stated that most institutional investors consider the attributes of a corporate board to be as important as an organization’s financial performance. Furthermore, Chung and Zhang (2011) also found that institutional investors favor firms with higher board independence, thus indicating that these firms are associated with lower monitoring costs. As yet, few studies have examined the role of institutional investors in the improvement of corporate governance around the world (Goranova and Ryan 2014). However, single-country studies, largely based on US data, have found that institutional investors can influence antitakeover amendments (Brickley et al. 1988), CEO turnover decisions (Parrino et al. 2003; Helwege et al. 2012), the selection of auditing firms (Kane and Velury 2004), managerial compensation schemes (Hartzell and Starks 2003; Almazan et al. 2005), dividend pay-outs, operating performance and CEO turnover (Brav et al. 2008), earnings management (Hadani et al. 2011), CEO pay and the introduction of shareholder proposals (Chhaochharia et al. 2012), corporate risk taking (Sakawa et al. 2021). Of these studies, most focus on overall governance levels (Aggarwal et al. 2011), firm performance (De-la-Hoz and Pombo 2016; Ferreira and Matos 2008), and CEO compensation (Croci et al. 2012) and earnings management (Kim et al. 2016). Little is known about the role of institutional investors in the improvement of board governance structures across the globe. Therefore, this study aims to augment the recent work of Aggarwal et al. (2011) by considering the comprehensive characteristics—such as composition, entrenchment and busyness—of corporate boards and their key sub-committees using a cross-country sample.

Several corporate governance studies have highlighted the importance of national institutional factors in explaining corporate governance phenomena (Aguilera et al. 2008, 2012; Aslan and Kumar 2014; Iannotta et al. 2016; Kim and Ozdemir 2014). One such institutional factor is the economic condition of a country (Essen et al. 2013; McNulty et al. 2013). The weakness of corporate governance in many countries is largely considered to have been a main contributor to the onset of the recent financial crisis (Akbar et al. 2017). Several studies have suggested that both institutional investors and corporate boards are to blame for their inability to prevent that crisis from occurring (Conyon et al. 2011; Reisberg 2015). In response to such a devastating crisis, several countries introduced or revised their corporate governance codes in an attempt to strengthen their governance practices (Adams 2012; Cuomo et al. 2016). Moreover, in the wake of the recent financial crisis, several countries issued stewardship codes and guidelines (beginning with the UK in 2010) in an effort to encourage and enhance engagement between institutional investors and their investee firms (ICGN 2017). However, we still know little about the role played by institutional investors in efforts to improve corporate governance with respect to the recent financial crisis. Therefore, this study also aims to examine the role of institutional investors in the improvement of corporate board characteristics in light of various economic conditions (pre-crisis, crisis and post-crisis periods).

Additionally, the bundle perspective of comparative corporate governance (Aguilera et al. 2008, 2012; Kim and Ozdemir 2014) argues that differences between board attributes across countries cannot be studied without also considering at least two other governance characteristics—legal system and ownership structure—as each of these characteristics is contingent upon the strength and prevalence of the other. Previous studies have shown that the legal system of a country (i.e., common or civil law) affects its accepted levels of investor protection (strong versus weak) (La Porta et al. 1998, 2000). To this end, La Porta et al. (1998) argued that in countries where investor protection rights are weak, investors may seek other means of protection. As a board of directors is entrusted with the protection of shareholder interests, institutional investors can improve corporate board characteristics to a greater degree in countries where shareholder protections are weak. Thus, this study complements previous empirical findings (Aggarwal et al. 2011) by investigating the capacity of institutional investors to improve a wide range of board characteristics within various legal systems (common versus civil law systems).

Moreover, previous studies on this topic (see, for example, Aggarwal et al. 2011; Ferreira and Matos 2008) have failed to consider a firm’s controlling shareholders when examining the role of institutional investors in the improvement of corporate governance. However, ownership structures are an important component of the bundle perspective of global corporate governance practices (Aguilera et al. 2012). Corporate governance practices and outcomes cannot be properly investigated without also considering the pivotal function of a firm’s ownership structure (Aguilera and Crespi-Cladera 2016; Desender et al. 2013; Judge 2011, 2012; Sur et al. 2013). Indeed, ownership structures vary across countries; widely-held firms are more common in the US and the UK, while firms with concentrated ownership structures are more common in continental European countries (La Porta et al. 1999). On the one hand, the presence of controlling shareholders might be beneficial; this might be because they have the incentive to better monitor managers’ actions due to their ownership interests. On the other hand, controlling shareholders might expropriate the interests of minority shareholders in favor of their own (Shleifer and Vishny 1997). In such a context, this research aims to examine the role of institutional investors in improving the governance structures of companies with various ownership structures (concentrated or dispersed ownership systems).

Using a sample collected from 15 countries (Australia, Belgium, Canada, Denmark, Finland, France, India, Ireland, Italy, Netherlands, Norway, Spain, Sweden, Switzerland and the UK) for the period 2006 to 2012, the results suggest that the association between institutional ownership and board governance structure is positive and significant and that foreign institutional investors play a more crucial role in the improvement of board governance structures than do their domestic counterparts. Concerning the individual attributes of corporate boards and their key sub-committees, the study demonstrates that institutional investors are most effective in improving the composition of boards and their key sub-committees (with the exception of nomination committees). Furthermore, while institutional investors are found to reduce board entrenchment, they do not appear to reduce board busyness. The results also suggest that the role of institutional investors in the improvement of governance outcomes is dependent on economic conditions (pre-crisis, crisis and post-crisis), legal systems and ownership structures. In particular, the findings show that institutional investors take on larger and more effective roles when it comes to improving the governance structures of firms during and after a crisis period compared to their roles and influence before a crisis begins. This is also true referring to boards of directors’ attributes, such as the independence of audit committees. Furthermore, in civil law countries, institutional investors enhance the boards’ independence and that of their key sub-committees (though nomination committees seem to be an exception). In common law countries, instead, institutional investors have the effect of reducing boards’ levels of busyness. Despite these findings, the study found no evidence about the institutional investors’ role in reducing boards’ entrenchment in these legal systems. The results also reveal that institutional investors have the ability to improve boards’ attributes (such as their composition, entrenchment and busyness) but only in non-family firms. The results are robust after performing a variety of robustness checks for endogeneity and reverse causality.

This paper contributes to the existing literature in various ways. To begin, this study is—to the best of my knowledge—the first to investigate the role of institutional investors in the improvement of governance attributes via the consideration of a comprehensive range of characteristics (to include composition, entrenchment and busyness) that are related to boards of directors and their key sub-committees (audit, compensation and nomination). From the viewpoint of agency theory, larger institutional shareholdings are expected to improve board governance structure in order to mitigate the agency and asymmetric information problems (Jensen and Meckling 1976). Therefore, this study investigate to which extent institutional investors can improve board governance structure by considering the comprehensive characteristics—such as composition, entrenchment and busyness—of corporate boards and their key sub-committees, using international sample. Second, this study contributes to the growing body of literature on comparative governance mechanisms (Aguilera et al. 2008; Kim and Ozdemir 2014). From the perspective of institutional theory, the external environment surrounding the entities and organizations may affect the way they behave (Scott 2004). In particular, this study explores the role of institutional investors in the improvement of board governance structures by examining various institutional settings, to include several economic conditions (pre-crisis, crisis and post-crisis periods), legal systems and ownership structures.

This paper is structured as follows. The first section discusses the literature and the hypothesis development. I then illustrate the study’s methodology, present the empirical analysis and summarize my findings. In the final section of this paper, I discuss the research implications and present potential avenues for future research.

2. Literature Review and Hypothesis Development

2.1. Institutional Investors and Corporate Governance

The increasing trend towards cross-border investment, as well as the financial crisis that occurred in many parts of the world, has led institutional investors to look more carefully at the corporate governance structures of their investee firms (Mallin 2016). Highly skilled institutional investors have increased investment growth over the past few decades and have created the expectation that good corporate governance practices should be established in their investee firms (OECD 2011). McCahery et al. (2015) have reported that corporate governance is a significant factor for institutional investors who are seeking to establish a healthy portfolio; indeed, a number of such investors are willing to enter into a dialogue with their investee firms in order to improve the governance structure. More recently, using sample from Japanese listed firms between 2007 and 2019, Sakawa et al. (2021) found that foreign institutional investors play a role in enhancing corporate risk. Furthermore, there has been increasing pressure from governments and various global stockholders for institutional investors to engage with their investee firms (Mallin 2016). Due to the high monitoring costs associated with the collection and analysis of information, as well as the costs associated with acting on the resulting findings (Fich et al. 2015), institutional investors are better able to provide active monitoring of investee firms than their smaller-investing counterparts. This is due to the fact that large owners can bear the high cost of monitoring because the potential returns associated with monitoring exceed the attendant costs (Gillan and Starks 2000). In this study, a corporate board is considered to be the main internal governance mechanism that protects the shareholders’ interests (Fama and Jensen 1983); thus, I posit that institutional investors, through their engagement with investee firms, will improve the attributes of a corporate board.

Hypothesis 1 (H1).

The higher the presence of institutional investors, the better the board governance structure in their investee firms.

2.2. Board Composition and Independence

As one function of board monitoring is the reduction of agency costs, great attention has been paid to the composition of corporate boards (Fama and Jensen 1983). The monitoring quality of a corporate board is determined by the effectiveness of its independent directors (Adams and Ferreira 2007). From the perspective of agency theory, a board and its key sub-committees (audit, compensation and nomination) should possess a majority composition of independent directors, as these members are considered to be the key figures of a corporate board and are responsible for monitoring the actions of managers in the firm (Hermalin and Weisbach 2003).

Board composition is also regarded as a central issue related to corporate governance codes around the world. According to Mallin (2016), national and international corporate governance bodies across the globe recommend that a board be largely composed of independent directors and board key sub-committees (audit, compensation and nomination) be largely (or even entirely) composed of independent directors. Using a sample of US-based insurance companies between 1992 and 1993, Beasley and Petroni (2001) have found that the greater a board’s independence, the higher the likelihood that the firm will be audited by one of the Big 6 accounting firms; this indicates that an auditing company that is independent from an organization’s management system is more likely to be hired if the board demonstrates greater independence. Osma (2008) has provided evidence that independent directors reduce the likelihood of accounting accruals manipulation; an examination of all UK-based non-financial firms between 1989 and 2002 led Osma to conclude that independent directors have the expertise and competence to efficiently monitor earnings management. Additionally, Ben-Amar and Zeghal (2011) have reported that board independence is associated with improved information disclosure concerning the compensation of executives in Canadian-listed firms.

Considering the composition of a board’s key sub-committees (audit, compensation and nomination), academic studies have shown that independence can contribute to the effectiveness of decisions issued by the corporate board as a whole (Anderson and Reeb 2004). Examining a sample of US-listed firms in operation between 1999 and 2003, Persons (2009) has found that firms with a greater number of independent directors on their audit committees are associated with earlier voluntary ethics disclosures and are less likely to be engaged in financial reporting fraud. Investigating a selection of 500 firms listed in the major US stock exchanges, Abbott and Parker (2000) have found that firms with a greater level of independence among their audit committee members are more likely to select large auditing firms to carry out their annual audits. A study of 492 US firms in 2001 by Abbott et al. (2003) has uncovered an inverse relationship between audit committee independence and financial restatement. Additionally, Klein (2002) has provided evidence that a higher level of independence among boards and audit committees results in decreased earnings management in US-based firms; this illustrates the argument that independent directors play a significant role in scrutinizing the process of financial reporting. Using US Fortune firms as a sample, Newman and Mozes (1999) have provided evidence that a CEO is likely to receive an excessive compensation package at the expense of shareholders when insiders dominate the compensation committee; this result calls for a greater number of independent directors to sit on compensation committees in order to facilitate the proper monitoring of compensation schemes. It is also the case that when a nomination committee is dominated by independent directors, the board is more likely to appoint more skillful independent directors who are able to better monitor managers and enhance the decisions issued by the board (Vafeas 1999). Therefore, given the importance of independent directors in corporate boards and their key sub-committees, I posit the following two hypotheses:

Hypothesis 2a (H2a).

The higher the presence of institutional investors, the higher the independence of the board.

Hypothesis 2b (H2b).

The higher the presence of institutional investors, the higher the independence of the board’s key sub-committees.

2.3. Board Entrenchment (Tenure)

The period of time during which a director serves on a board has received significant attention in the literature; so far the study of director tenure has resulted in mixed evidence in terms of board effectiveness and functionality. Given the experience perspective, for instance, Vafeas (2003) has proposed that directors who enjoy a long period of service on a board are better informed about the firm and the environment in which the company operates, resulting in greater levels of commitment and allowing the members to become more effective monitors of management. This view is consistent with the findings of Dou et al. (2015), who have discovered that long-serving directors are associated with improved board meeting attendance, greater committee membership and lower CEO pay in US firms. Furthermore, Beasley’s (1996) study of 150 public US firms has indicated that as the tenure of an outside director increases, the occurrence of financial statement fraud decreases; this demonstrates that long-serving directors possess a greater ability to scrutinize the actions of top management than do their newer counterparts.

In contrast to this view, other studies have revealed that long serving directors are more likely to have established friendships with managers; this may limit their ability to properly monitor the actions of management and to protect shareholders’ interests. For example, Boone et al. (2002) examined a sample, taken over 25 years, of the five largest newspaper companies in the Netherlands and have presented evidence that long-tenured directors restrict the appointment of new directors to the board, which results in a lack of diversity and ineffective decision making. Based on a study of various S&P 1500 firms, Berberich and Niu (2011) have found that director tenure is positively associated with governance problems, thus indicating a need to limit directors’ length of service. Barroso et al. (2011) have provided evidence that a long-tenured board does not support firm diversification in Spanish organizations, suggesting that long-serving directors are likely to operate according to routines that are formed over time; thus, such directors are limited to specific environments, which makes their knowledge less valuable as the years progress. Consulting a sample of US-listed firms taken from 2001–2006, Jia (2017) has found that organizations with a higher percentage of directors with extended tenure are associated with lower innovation productivity. She has also argued that when the proportion of long-tenured directors decreases due to director deaths, higher innovation performance ensues.

Aside from board tenure, CEO tenure has also received much attention which suggests that it plays an important role in influencing the decisions delivered by the board (Hambrick and Fukutomi 1991). Entrenched managers may establish certain strategies that enable them to increase their own benefits while neglecting the interests of shareholders. Miller (1991) has claimed that CEO tenure may lead to deviation from the firm environment, which adversely affects organizational performance. Furthermore, a long-serving CEO may influence the director selection process, as such figures are more likely to have established close relationships with other directors on the board (Finkelstein and Hambrick 1996; Cook and Burress 2013). Based on a sample of US firms drawn from 1993–2004, Bebchuk et al. (2011) have reported that the exercise of CEO power leads to lower firm performance, which in turn contributes to increased agency costs. Following a study of US public firm performance between 1993 and 1999, Grinstein and Hribar (2004) have found that CEOs who exert greater power tend to negotiate larger merger deals; thus, their acquisition announcements send negative signals to the market. In the context of imposing term limits on the members of a board of directors, a growing number of countries have adopted tenure related guidelines. In the UK, for instance, the Corporate Governance Code published in 2010 (revised more recently in 2016) requires that firms annually illustrate their rationale for determining that a director who has served more than nine years still qualifies as an independent director (Financial Reporting Council 2010). Given the above argument on long-tenured directors, I posit that institutional investors play a role in reducing directors’ entrenchment.

Hypothesis 3 (H3).

The higher the presence of institutional investors, the lower the board entrenchment.

2.4. Board Busyness

Board busyness refers to a situation in which a director holds multiple appointments to several boards. Fama and Jensen (1983) have stated that service on a large number of boards is a sign of director reputation and quality. They have argued that directors who hold multiple appointments may be better advisors and can monitor management more efficiently than their counterparts. These characteristics also enable them to build their reputations and acquire additional directorships in the future (Shivdasani and Yermack 1999). A number of studies support the idea that there are significant benefits associated with the holding of multiple directorships (Ferris et al. 2003; Field et al. 2013; Rosenstein and Wyatt 1994). Conversely, other studies have argued that board busyness brings unfavorable results that negatively affect the performance and governance structure of a firm. For instance, Jiraporn et al. (2009) studied the relationship between board busyness and board meeting attendance in US listed firms from 1998–2003 and found that directors with multiple board appointments are more likely to be absent from board meetings. These results are also supported by the work of Masulis and Mobbs (2014), who studied a sample of S&P 1500 firms from 1997–2006 and found that busy directors choose to spend their time and energy inequitably, granting unequal attention to each firm for whom they sit on a board. They found that busy directors attend more meetings and offer better monitoring for the firm that carries greater prestige and thus captures their time and energy. Using a sample of the largest firms listed in the Forbes 500 between 1989 and 2005, Fich and Shivdasani (2006) have examined the effect of board busyness on firm performance and have shown that busy boards result in poor governance, weaker profitability and a lower sensitivity of CEO turnover to firm performance. They have also reported that when busy outside directors depart from a board, positive abnormal returns are noticed. Core et al. (1999) have reported that busy outside board directors are positively associated with greater CEO compensation in US public firms, resulting in higher agency costs. I posit that overcommitted directors have a reduced ability to monitor their boards and are more likely to suffer from ineffective decision making. Therefore, I expect that institutional investors will decrease the number of directorships in their investee firms. Thus, I hypothesise that:

Hypothesis 4 (H4).

The higher the presence of institutional investors, the lower the board busyness.

3. Methodology and Data Description

3.1. Data and Sample

My sample consists of firms listed in the major stock indices in 15 countries around the world (see Appendix A). Following in the vein of previous studies, my sample includes non-financial firms (i.e., Ferreira and Matos 2008), yielding a total of 517 firms (totalling 2586 firm observations). I collected the data using several resources, including BoardEX, Worldscope, Thomson One, World Bank and corporate governance annual reports. This study covers the years between 2006 and 2012; this period was chosen in order to fully capture the role of institutional investors in the improvement of corporate governance according to various economic conditions (pre-crisis, crisis and post-crisis). Following in the manner of previous studies, this study used the decline of GDP as an indicator of crisis in each country (Dimitras et al. 2015). This process resulted in a total of 959 firm observations during the pre-crisis period, 1156 firm observations during the crisis, and 471 firm observations during the post-crisis period. Likewise, in order to investigate the role of institutional investors in the promotion of governance structures in various shareholder rights environments, I divided my sample into two groups; following the example of La Porta et al. (2000), these classifications were made based on the legal regimes of the countries. This process resulted in a total of 1364 firm observations in civil law countries and 1222 firm observations in common law countries. To test whether ownership structures affect the roles of institutional investors in the improvement of governance outcomes, I classified my sample into two categories—family and non-family owned firms. I also used interaction variables between institutional investors and controlling shareholders (for both family and non-family owned firms) to account for the influence of institutional investors in the promotion of governance structures under different ownership structures (Croci et al. 2012).

3.2. Dependent Variables: Board Governance

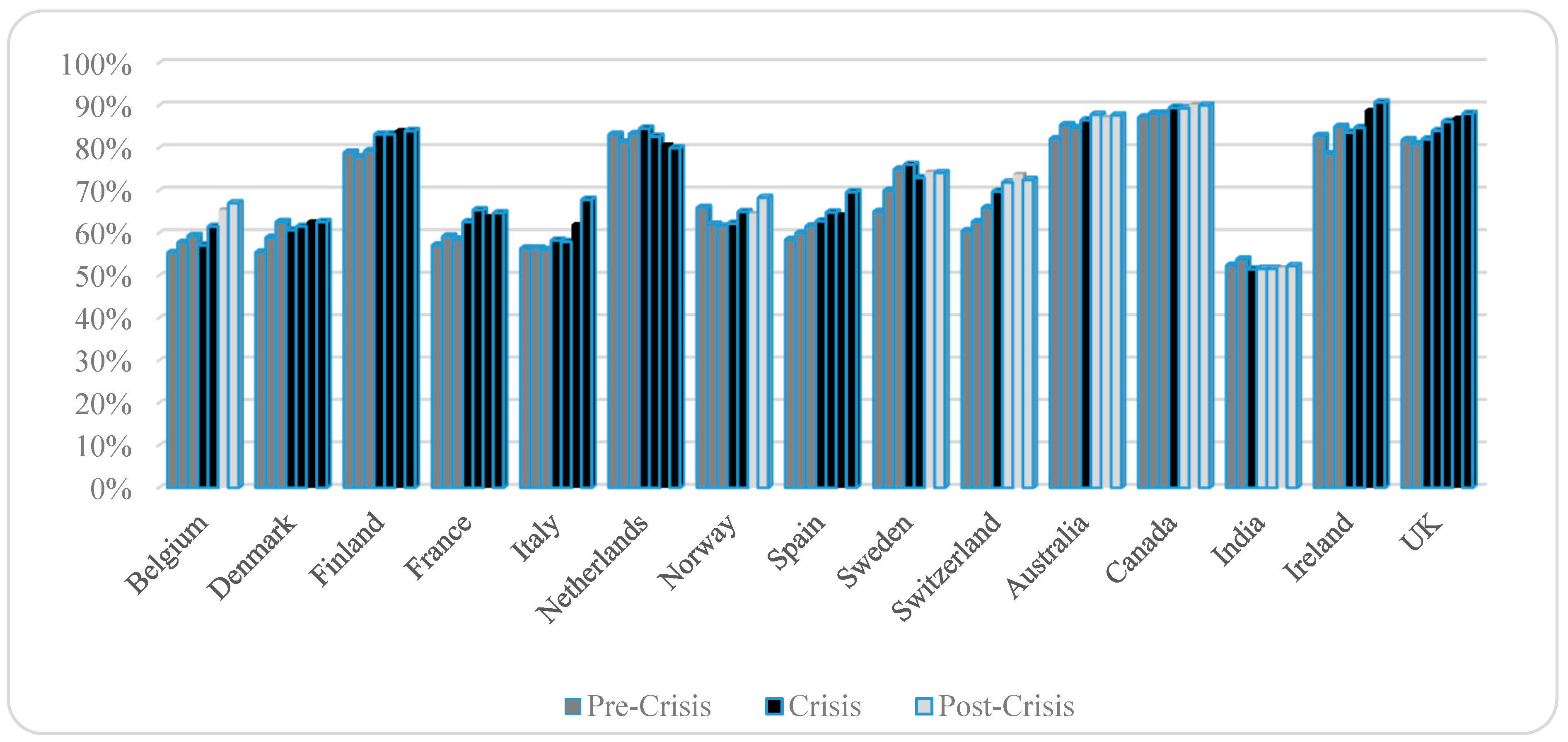

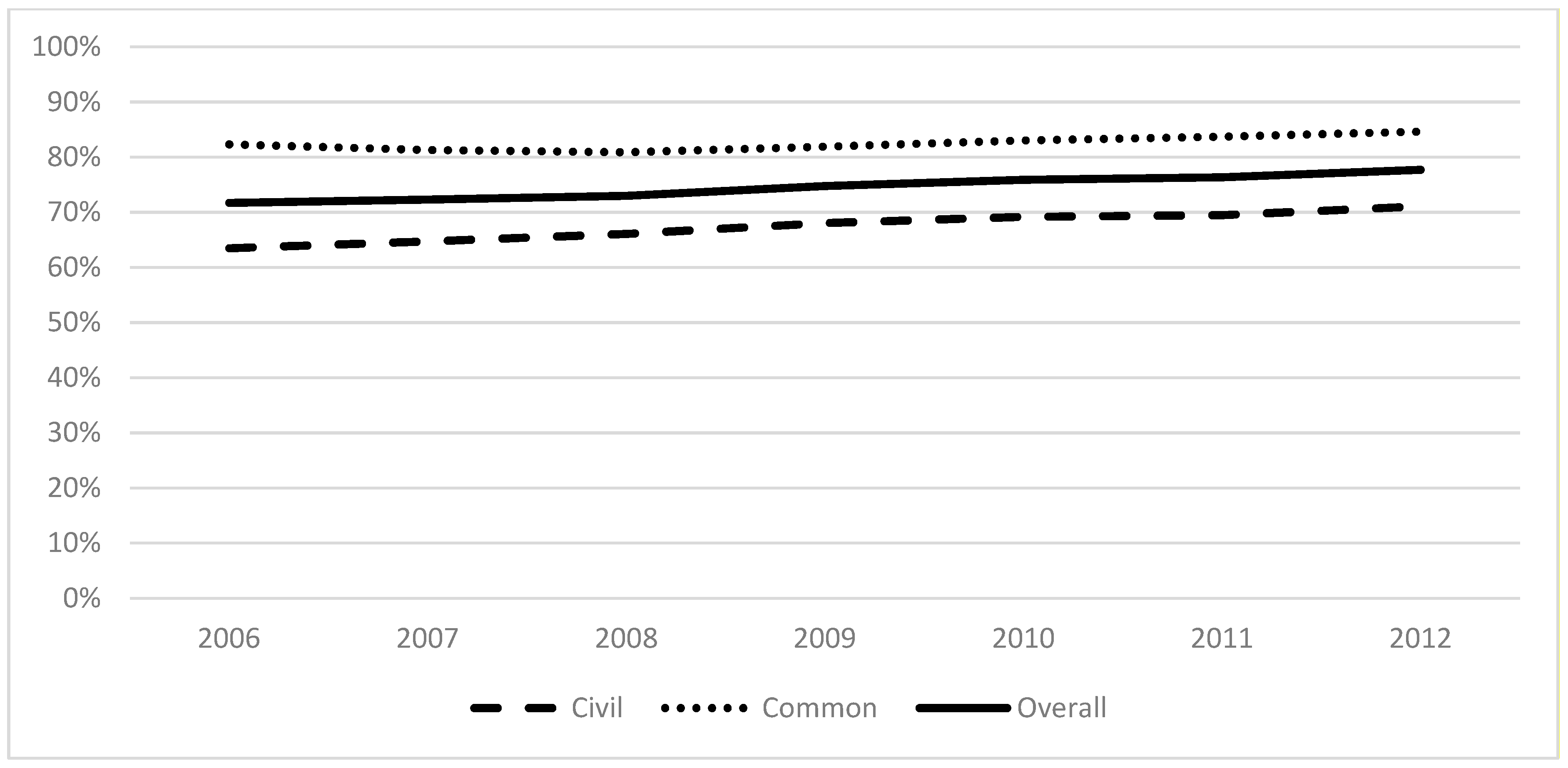

In my sample, I used several attributes to serve as proxies for good board governance. I first used the board attributes index (GOV14), which covers the main attributes related to the structure and function of a corporate board and its key sub-committees (see Appendix B). The index assigns a value of one to each of the 14 attributes, provided that the company meets the guidelines of each attribute, or zero if it does not. These attributes were mainly adapted from the index used by Aggarwal et al. (2011). Figure 1 shows that on average, the countries with the highest GOV14 score in 2012 are Ireland (90.8%), Canada (90.0%), the U.K (88.1%), Australia (87.7%) and Finland (84.0%). The countries with the lowest GOV14 score are India (52.3%), Denmark (62.6%), France (64.7%), Belgium (67.0%) and Italy (67.9%). Figure 2 displays the weighted averages of the board attributes index (GOV14) for firms located in both civil law countries and common law countries. Overall, the figure illustrates that, on average, common law countries have better board attributes (GOV14) than do their civil law counterparts.

Following the example of other studies that have criticised the corporate governance index (see, for example, Daines et al. 2010), I also used individual attributes to cover various aspects of a corporate board and its key sub-committees. These attributes include: board and key sub-committee composition (the independence of a board and of its key sub-committees), board entrenchment (CEO tenure and the average of board tenure) and board busyness (the average number of directorships held by independent non-executive directors (INEDs) and the percentage of INEDs who are busy).

3.3. Independent Variables: Institutional Ownership

The independent variable in this study, institutional ownership, was classified into five types according to Aggarwal et al. (2011): total, foreign, domestic, common law and civil law.

3.4. Control Variables: Firm and Country Characteristics

In addition to the main explanatory variables, I also used a set of firm and country control variables. Following the example of Aggarwal et al. (2011), all regression models used control variables related to firm characteristics; these variables were firm size, sales growth, leverage, cash, capital expenditure, market-to-book value, return on assets, property, plant and equipment, analyst coverage, cross-listing. Furthermore, following Faccio and Lang (2002), I controlled for the ultimate owner of a firm using a 20% cut-off; firms were classified as either family owned (FAMILY), state owned (STATE), institutional investor owned (IO), or widely held (WIDELY). I also control for the rule of law and various economic conditions in each country (pre-crisis, crisis and post-crisis), following Essen et al. (2013). All variables are defined in Appendix C.

4. Empirical Analysis

This section outlines the findings of my empirical analysis. First, Table 1 summarizes the descriptive statistics and the correlation matrix of the main variables. The results demonstrate that the board attributes index (GOV14) has an average score of 10, while the independence of a board and its key sub-committees (audit, compensation and nomination) have average values of 64%, 85%, 80% and 71%, respectively. For the entire sample, CEO tenure has an average value of 5 years, while the average score for board tenure is 6 years. Furthermore, the average number of directorships held by each director in my sample is 2.6, and an average of 43% of the boards in my sample are busy. Table 1 also demonstrates that the average values for institutional ownership (total, foreign, domestic, common and civil) are 36%, 20%, 16%, 28% and 8%, respectively. The results also show that none of the independent variables are significantly correlated (above 0.80) (Gujarati 2003), with the exception of IO Total and IO Common. However, these two variables are not combined in any of the regressions in my analysis.

Turning to the regression results, I applied firm fixed effects panel regressions to investigate the role of institutional ownership in corporate governance (see Table 2). Models 1 and 2 of Table 2 illustrate that there is a positive and significant association between total and foreign institutional ownership and the board attributes index (GOV14) at 5% and 1%, respectively (with coefficient = 0.006 and 0.009, p-value = 0.033 and 0.008, and R-Squared value = 0.098 and 0.101, respectively). However, Models 3, 4 and 5 demonstrate that the coefficients are mixed and insignificant for domestic, common and civil institutions (with coefficient = −0.001, 0.005 and 0.008, p-value = 0.758, 0.110 and 0.313, and R-Squared value = 0.095, 0.097 and 0.096, respectively). Overall, the results are partially consistent with H1 and are consistent with the agency theory. The findings particularly contribute to the literature of corporate governance that corporate board attributes are important for the institutional investors and that they enhance these attributes when they engage with their investee firms, with the foreign institutional investors playing a lead role in the improvement of board attributes. The results also imply that attributes of the corporate board are deemed to be crucial for the institutional investors, as the attributes of the corporate board reflect its effectiveness in the reduction of agency cost and in fulfilling its duties (Zahra and Pearce 1989; Aguilera et al. 2012; Mallin 2016).

Notably, these results were wholly consistent with the findings of Aggarwal et al. (2011), who argued that foreign institutional investors promote favorable governance outcomes as compared to their domestic counterparts. This also reflects previous studies (e.g., Gillan and Starks 2003; Ferreira and Matos 2008; Beuselinck et al. 2017; Luong et al. 2017) that contended that foreign institutional investors have fewer ties to their investee firms 6because of their independent positions and therefore are expected to exert greater pressure over the management of an investee firm in an effort to establish a strong governance structure. The results are also consistent with the previous studies which stated that foreign institutional investors can effectively promote growth opportunities (Sakawa and Watanabel 2020) and corporate risk taking (Sakawa et al. 2021) in a stakeholders-oriented corporate governance system like Japan.

Table 2 also shows that the role of institutional investors operating within various economic conditions is significant only during crisis and post-crisis periods, but not during pre-crisis periods (see Table 2, Panels B–D). This is consistent with previous studies that claim that institutional investors took excessive risks before the crisis (Erkens et al. 2012; Díez-Esteban et al. 2016). This may also explain why institutional investors did not enhance board attributes (GOV14) in their investee firms prior to the financial crisis. Adams (2012) also found that the governance structure of non-financial firms is weaker compared to their financial counterparts prior to the recent financial crisis. Several scholars have blamed both the institutional investors and the corporate boards alike for their inability to mitigate the aforementioned crisis (Conyon et al. 2011; Reisberg 2015). The results also reveal that during crisis periods, only foreign institutions have a positive and significant relationship at 10% (with coefficient = 0.010, p-value = 0.072, and R-Squared value = 0.111). After the crisis passes, however, all types of institutional investors have positive and significant associations with the board attributes index, with the exception of foreign institutional investors (with coefficient = 0.022, 0.015, 0.033, 0.018 and 0.070, p-value = 0.005, 0.112, 0.012, 0.059, 0.000, and R-Squared value = 0.090, 0.072, 0.083, 0.076 and 0.100, respectively). Overall, the results are consistent with the institutional theory, and they indicate the institutional investors’ awareness of the importance of corporate board attributes after the recent financial crisis. Following the crisis, the OECD published a report on governance lessons learned from the recent financial crisis that clearly illustrates that the weaknesses of corporate governance was one of the key reasons the crisis occurred (Kirkpatrick 2009).

Furthermore, Table 2 reports the results of the firm fixed effects regression of the board attributes index (GOV14); these results indicate that the role of institutional investors in the improvement of governance structures is dependent on the legal system of the country in which a firm is listed (see Table 2, Panel E). In common law countries, total and foreign institutional investors have positive and significant relationships at the 10% and 1% significance levels, respectively (with coefficient = 0.005 and 0.011, p-value = 0.069 and 0.001, and R-Squared value = 0.146 and 0.154, respectively). Conversely, in civil law countries, these associations are mixed but insignificant. Drawing from the institutional theory, the results complement the other studies that ascertained that the legal system should be considered when investigating the adoption of corporate governance practices across countries (Aguilera et al. 2008; Aguilera et al. 2012; Kim and Ozdemir 2014). In particular, the findings reveal that the activism of institutional investors towards improving board attributes in their investee firms is also attributed to the legal system of a particular country. The results also show that total and foreign institutions have positive and significant associations at 1% in non-family owned firms (with coefficient = 0.008 and 0.013, and p-value = 0.008 and 0.000, respectively); this result does not stand for family owned firms, however (see Table 2, Panel F). Drawing from the institutional theory, these results also complement the other studies that emphasized the contingency of ownership structure when investigating the adoption of corporate governance mechanisms in a particular firm (Desender et al. 2013; Judge 2011, 2012; Sur et al. 2013) by showing that the role of institutional investors in improving board attributes is determined by the ownership structure (family vs. non-family-controlled firms).

In Table 3, Table 4 and Table 5, I repeat the same analysis by considering the composition of a corporate board and of its key sub-committees, board entrenchment and board busyness. In this study, the independence of the board is measured by the proportion of independent directors on the board (Osma 2008; Sharma 2011). The results indicate a positive and significant association between board independence and total institutional ownership at the 5% significance level (with coefficient = 0.001, p-value = 0.036 and R-Squared value = 0.077). Drawing from the agency theory, the results are consistent with those who ascertained that institutional investors are attracted by firms whose board independence is high (Useem et al. 1993; Chung and Zhang 2011). Several scholars emphasised the importance of corporate board independence in the reduction of the agency costs (Anderson and Reeb 2004; Bebchuk and Weisbach 2010). However, this coefficient is positive but insignificant for foreign and domestic institutions (see Table 3, Panel A). I also find that total institutional ownership promotes the improved independence of audit and compensation committees (with coefficient = 0.001 and 0.001, p-value = 0.003 and 0.002, and R-Squared value = 0.054 and 0.039, respectively). Conversely, total institutional ownership has a negative but insignificant relationship with nomination committee independence. Results also reveal that domestic and foreign institutions promote the independence of audit committees (with coefficient = 0.001 and 0.001, p-value = 0.082 and 0.027, and R-Squared value = 0.049 and 0.051, respectively), while foreign institutions promote the independence of compensation committees (with coefficient = 0.001, p-value = 0.009 and R-Squared = 0.038). Both types of institutional investors (domestic and foreign) have an insignificant association with the independence of the nomination committee (see Table 3, Panel A), however. Collectively, these results support the agency theory and are consistent with H2a and H2b. Given the monitoring role of institutional investors, these results reflect other studies that emphasized the importance of the composition of audit and compensation committees in mitigating the agency costs (Newman and Mozes 1999; Abbott and Parker 2000; Klein 2002; Abbott et al. 2003; Zaman et al. 2011).

The study further finds that during pre-crisis periods, institutional investors have mixed but insignificant influence over the independence of a board and its key-sub-committees. However, during times of crisis, total institutional investors have positive and significant relationships with the independence of audit committees at 5% (with coefficient = 0.001, p-value = 0.020 and R-Squared = 0.071), and negative and significant relationships with the independence of nomination committees at 1% (with coefficient = −0.001, p-value = 0.068 and R-Squared = 0.067). Furthermore, foreign institutional investors have positive and significant associations with the independence of a board and its audit committee at 10% and 5%, respectively (with coefficient = 0.001 and 0.002, p-value = 0.054 and 0.014 and R-Squared = 0.080 and 0.075, respectively). The results support the institutional theory and are consistent with those who found that board independence may bring fruitful governance outcomes during crises. For instance, Francis et al. (2012) and Yeh et al. (2011) found that board independence and audit committee independence improved firm performance during the time of the crisis, respectively. Finally, the results indicate that during post-crisis periods, only domestic institutional investors have positive and significant associations with the independence of audit and nomination committees at 5% and 10%, respectively (with coefficient = 0.004 and 0.003 p-value = 0.030 and 0.092 and R-Squared = 0.123 and 0.108, respectively).

With regard to whether legal systems affect the role of institutional investors in improving the composition of a board and that of its key sub-committees (see Table 3, Panels E and F), the results show that institutional investors promote the improved composition of boards and their key sub-committees (with the exception of nomination committees) in civil law countries, but not in common law countries. The results revealed that total institutional investors have a positive and significant association with the independence of the board and audit and compensation committees at a 5% significance level (with coefficient = 0.001, 0.002 and 0.002, p-value = 0.020, 0.016 and 0.016, and R-Squared value = 0.101, 0.089 and 0.062, respectively). The findings are explained by the institutional theory perspective, in that institutional investors improve the composition of the board and its key subcommittees in civil law countries in order to mitigate the weak shareholder protections in civil law countries compared to their common law counterparts (La Porta et al. 1998). Gaitán et al. (2018) showed that board independence is among the factors leading to firm productivity in civil law countries. This is consistent with Yeh et al. (2011), who argued that the influence of the audit committee’s independence on firm performance is greater in civil law countries compared to their common law counterparts. The results also indicate that institutional investors can indeed improve the composition of a board and of its key sub-committees (with the exception of the nomination committee) in non-family owned firms. In family owned firms, however, the results illustrate that institutional investors (foreign and total) improve the independence of audit committees only (see Table 3, Panel G).

Concerning board entrenchment, the results indicate that total, foreign and domestic institutional investors have positive but insignificant relationships with CEO tenure. In contrast, institutional investors (total, foreign and domestic) have negative associations with board tenure; this association, however, is only significant with respect to domestic institutions at the 10% significance level (with coefficient = −0.011, p-value = 0.053, and R-Squared = 0.100), (see Table 4, Panel A). The findings, therefore, partially support H3. Drawing from the theoretical framework of agency theory, the results are consistent with those who argued that long-tenured directors may become less effective in monitoring the firm, as they are likely to form friendships and become closer to the managers (Vafeas 2003; Barroso et al. 2011). Others also argued that firms with long-tenured boards are likely to be more resistant to change, and associated with a lower degree of international diversification, fewer patents and research and development (Musteen et al. 2006; Barroso et al. 2011; Jia 2017).

The results show that during pre-crisis periods, institutional investors (total and domestic) promote board entrenchment (CEO duality) (with coefficient = 0.063 and 0.172, p-value = 0.082, 0.069, and R-Squared value = 0.125 and 0.148, respectively); this aspect wanes, however, during crisis and post-crisis periods (see Table 4, Panels B, C and D). Upon a comparison of this relationship under different legal systems, the results indicate that institutional investors have mixed but insignificant associations with board entrenchment measures (CEO tenure and board tenure) in common law countries. In civil law countries, however, domestic institutional investors have negative and significant associations with board tenure at 5% (with coefficient = −0.026, p-value = 0.016, and R-Squared value = 0.133) (see Table 4, Panels E and F). Furthermore, the results reveal that the association between institutional investors and board entrenchment is mixed and insignificant in both family and non-family owned firms (see Table 4, Panel G). Finally, the findings indicate a negative and significant association between domestic institutions and board tenure at the 10% significance level in non-family owned firms (with coefficient = −0.010, and p-value = 0.090).

The study also investigated whether the institutional investors play a role in the reduction of board busyness. Board busyness is measured by two proxies; average directorships held by INEDs, and the proportion of INEDs who hold three or more directorship in public firms (Cashman et al. 2012). The results indicate that institutional investors (total, foreign and domestic) have mixed but insignificant associations with board busyness measures (see Table 5, Panel A). Therefore, H4 is rejected. Interestingly, results indicate that institutional investors behave differently according to different economic conditions. For example, total institutional investors promote board busyness in times of crisis in both measures (with coefficient = 0.004 and 0.001, p-value = 0.039 and 0.061, and R-Squared value = 0.077 and 0.060, respectively), while during pre-crisis and post-crisis periods, this influence is not evident (see Table 5, Panels B, C and D). The results are consistent with those who found that busy directors may be beneficial to the firm, as their experience and connection with other firms makes them competent compared to their non-busy counterparts on the board. For instance, firms with a busy board have been found to perform better (Pombo and Gutiérrez 2011; Field et al. 2013), bargain better deals and acquisitions of other firms (Benson et al. 2015; Harris and Shimizu 2004), and meet at a higher frequency (Baccouche et al. 2014). As far as legal systems are concerned, the results illustrate that the tendency of institutional investors to reduce board busyness is mixed and insignificant within both systems (see Table 5, Panels E and F); however, total institutional investors have negative and significant associations in common law countries at 10%. The results also suggest that the role of institutional investors in reducing board busyness is shaped by the ownership structure of a given firm. The results reveal that foreign institutional investors reduce board busyness in non-family firms as the relationship with foreign institutions is negative and significant at 10% (with coefficient value = −0.003 and −0.001, and p-value = 0.064 and 0.057, respectively) (see Table 5, Panel G).

5. Robustness Check

Considering the above results, I conclude that the relationships between institutional investors and various board attributes might not be driven by the efforts of institutional investors to improve these attributes—indeed, there is also the possibility that institutional investors may be attracted to firms with good board structures (see Aggarwal et al. 2011). In short, it is possible that endogeneity drives these primary results; therefore, I conducted four robustness tests to confirm my central findings. These tests included (1) a reverse causality analysis, (2) alternative measures, (3) a dynamic panel generalized methods of moments (GMM) and (4) a propensity score matching analysis. Overall, the results of the robustness tests are consistent with my main findings. These results are not included in this paper; they are, however, available in the internet Appendix.

6. Summary and Discussion

Employing a panel data analysis of 517 firms across 15 countries between 2006 and 2012, the study investigated the role of institutional investors in the promotion of board governance structures in their investee firms. Additionally, the study examined the role of institutional investors in the improvement of board governance structure within a range of settings, to include various economic conditions (pre-crisis, crisis and post-crisis), legal systems and ownership structures. Consistent with previous studies (Aggarwal et al. 2011; Ferreira and Matos 2008), the findings illustrated empirical evidence that global institutional investors are the main promoters of corporate governance around the world. The study also provided evidence that institutional investors inspire greater independence of a board and its key sub-committees (with the exception of nomination committees). Furthermore, the results suggest that institutional investors reduce board entrenchment, though the findings detected no evidence that they likewise reduce board busyness.

The results also indicate that institutional investors operate differently in different economic conditions (pre-crisis, crisis and post-crisis periods). Overall, the study found that the institutional investors minimized their influence over governance choices during the pre-crisis period. On the other hand, their role in improving the governance structure increased during the crisis and post-crisis periods. This trend was also evidenced for the independence of audit committees but not that of compensation and nomination committees, nor for board independence. In the context of board entrenchment and board busyness, the study found that institutional investors behave differently under different economic conditions. The study also found that institutional investors promote higher board entrenchment in the pre-crisis period, although this influence was not captured in crisis and post-crisis periods. Similarly, they promote higher board busyness during the crisis period. However, once the crisis passes, this influence is not significant. This result may imply that during the crisis period, busy directors may bring to the table the knowledge and expertise that they have gained from other boards as the emphasis is more on advising than on monitoring (Francis et al. 2012); therefore, board busyness may be promoted by institutional investors during a time of crisis in an attempt to help the firm to ride out the crisis.

The results also imply that the shareholder rights established by the country wherein the investee firm is located can affect the role of institutional investors in the promotion of board governance structure. Overall, the study found that institutional investors promote better board attributes in common law countries as compared to their civil law counterparts. However, when considering individual attributes, institutional investors are found to promote better independence of the board and its key sub-committees in civil law countries; this result does not stand in common law countries. This finding is consistent with the work of La Porta et al. (1998), who have argued that investors in countries with weak shareholder protections may seek out other means of protecting their investments.

The results also imply that the role of institutional investors in the improvement of governance outcomes is dependent on the ownership structure of the firm. Overall, the results indicate that institutional investors can improve the governance outcomes in non-family owned firms to a greater extent compared to their influence on family owned firms. The results provide evidence that institutional investors can promote the greater independence of a corporate board and its sub-committees (with the exception of nomination committees) and can reduce board entrenchment and busyness in non-family owned firms. These results are also in line with other studies that emphasize the contingency of ownership structure when investigating the adoption of corporate governance mechanisms in a particular firm (Desender et al. 2013; Judge 2011, 2012; Sur et al. 2013).

7. Conclusions

The rise in institutional investments is a key trend in the realm of global economics. As such, researchers have been inspired to explore the role that institutional investors play in the improvement of governance structures. In this study, the role of institutional investors in the improvement of board governance structure was examined using evidence relating to a number of board attributes from 15 countries across the globe. The results indicate that foreign institutional investors have a lead role in the improvement and convergence of corporate governance practices around the world. The findings have demonstrated that institutional investors promote the greater independence of boards and their key sub-committees (with the exception of nomination committees). Furthermore, while institutional investors reduce board entrenchment, no evidence was found that they reduce board busyness. The results also imply that a firm’s prevalent national institutional environment (i.e., prevailing economic conditions, legal systems and ownership structures) should be considered during attempts to study the activism of institutional investors.

The implications of this study are particularly meaningful to policymakers. On the one hand, the findings suggest that institutional investors play a meaningful and effective role in the improvement of governance structures within their investee firms. Thus, policymakers around the world are encouraged to continue to issue stewardship and corporate governance codes in order to increase awareness and encourage wider engagement between institutional investors and their investee firms in the future. On the other hand, the results highlight the importance of several institutional settings when studying the role of institutional investors in improving the governance structure in their investee firms. These settings include different economic conditions (pre-crisis, crisis and post-crisis periods), legal systems and ownership structures.

It is important to note that this study has several limitations. First, the data analysis was constrained by the limited availability of data concerning several emerging and developing markets. Future studies might attempt to overcome this limitation as more data becomes available for such countries so that the activism of institutional investors can be examined in a variety of market settings. Second, future research should also consider the introduction of additional corporate board attributes, such as board diversity and activity. Third, future studies might consider culture variances among countries, as culture can influence the level of governance in investee firms (Li and Harrison 2008). This will allow researchers to gain insight into the topic of whether culture variances between countries can influence the role of institutional investors in the improvement of corporate governance structures.

Funding

This research received no external funding.

Institutional Review Board Statement

Not Applicable.

Informed Consent Statement

Not Applicable.

Data Availability Statement

The source of data supporting reported results are shown in Section 3.1.

Acknowledgments

This paper is based on my Ph.D. thesis (Institutional Investors and Corporate Governance) from the University of East Anglia; UK. The thesis was supervised by Christine Mallin and Francesca Cuomo. I would like to thank both of them for their insightful comments, continuous guidance, unlimited support and invaluable encouragement during my study period at the University.

Conflicts of Interest

The author declares no conflict of interest.

Appendix A

{kind=link}

{kind=link}

Table A1.

Sample Description.

| SN | Country | Index Name | Number of Firms Per Year | Total Unique Firms | Total Observations | ||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| 2006 | 2007 | 2008 | 2009 | 2010 | 2011 | 2012 | |||||

| Civil Law Countries | |||||||||||

| 1 | Belgium | BEL 20 | 12 | 12 | 13 | 13 | 13 | 12 | 13 | 16 | 88 |

| 2 | Denmark | OMX COPENHAGEN 20 | 13 | 12 | 13 | 12 | 13 | 13 | 13 | 18 | 89 |

| 3 | Finland | OMX Helsinki 25 | 19 | 21 | 20 | 20 | 23 | 22 | 21 | 26 | 146 |

| 4 | France | CAC 40 | 32 | 31 | 31 | 30 | 31 | 33 | 34 | 38 | 222 |

| 5 | Italy | FTSE MIB | 19 | 20 | 20 | 19 | 18 | 19 | 18 | 25 | 133 |

| 6 | Netherland | AEX | 17 | 18 | 18 | 19 | 19 | 20 | 20 | 26 | 131 |

| 7 | Norway | OBX | 17 | 19 | 21 | 21 | 20 | 22 | 23 | 32 | 143 |

| 8 | Spain | IBEX 35 | 22 | 23 | 24 | 24 | 24 | 26 | 24 | 34 | 167 |

| 9 | Sweden | OMX STOCKHOLM 30 | 19 | 20 | 22 | 23 | 23 | 22 | 21 | 25 | 150 |

| 10 | Switzerland | SMI | 17 | 13 | 13 | 13 | 14 | 12 | 13 | 20 | 95 |

| Common Law Countries | |||||||||||

| 11 | Australia | S&P/ASX 50 | 24 | 25 | 30 | 35 | 30 | 29 | 29 | 42 | 202 |

| 12 | Canada | S&P/TSX 60 | 42 | 45 | 44 | 44 | 45 | 49 | 48 | 61 | 317 |

| 13 | India | BSE 30 | 6 | 13 | 19 | 22 | 22 | 23 | 22 | 31 | 127 |

| 14 | Ireland | ISEQ | 10 | 10 | 10 | 14 | 15 | 16 | 17 | 20 | 92 |

| 15 | United Kingdom | FTSE100 | 63 | 66 | 67 | 68 | 74 | 70 | 76 | 103 | 484 |

| Total | 332 | 348 | 365 | 377 | 384 | 388 | 392 | 517 | 2586 | ||

Appendix B

Table A2.

Board Attributes Index (GOV14).

| 1. Board size is greater than five but less than 16. |

| 2. Board is controlled by more than 50% independent outside directors. |

| 3. Board-approved succession plan in place for the CEO. |

| 4. Board performance is reviewed annually. |

| 5. Audit committee composed solely of independent directors. |

| 6. Compensation committee composed solely of independent directors. |

| 7. The majority of members of nomination committee are independent directors. |

| 8. All directors attended 75% of board meetings. |

| 9. Chair and CEO positions are separated or there is lead director. |

| 10. CEO is not serving on nomination committee. |

| 11. Chair is INED. |

| 12. Board is not busy (at least half of the INEDs hold ≤ two directorships in public companies). |

| 13. CEO is not busy (CEO holds ≤ two directorships in public companies). |

| 14. Chair is not busy (Chair holds ≤ two directorships in public companies). |

Appendix C

Table A3.

List of Variables.

| Variables | Variables Definition | Source |

|---|---|---|

| Dependent Variables: Board Attributes | ||

| Board attributes index (GOV14) | Firm level governance measured by the main attributes related to the structure and function of the corporate board and key committees. | BoardEX |

| Board independence (INED BOARD) | The proportion of independent directors on the board. | BoardEX |

| AC independence (INED AC) | The proportion of independent directors on the audit committee. | BoardEX |

| CC independence (INED CC) | The proportion of independent directors on the compensation committee. | BoardEX |

| NC independence (INED NC) | The proportion of independent directors on the nomination committee. | BoardEX |

| CEO tenure (CEO TENURE) | Total number of years that CEO has served on the board. | BoardEX |

| Board tenure (BOARD TENURE) | Total number of years that board members have served on the board divided by total number of board members. | BoardEX |

| Busy board (BUSY BOARD) | Average directorships held by INEDs. | BoardEX |

| Busy board% (BUSY BOARD%) | Proportion of the INEDs who hold three or more directorship in public firms. | BoardEX |

| Independent Variables: Institutional Ownership | ||

| Total IO (IO TOTAL) | Holdings by all institutions as a fraction of market capitalization. | ThomsonOne |

| Foreign IO (IO FOR) | Holdings by institutions located in a different country from where the stock is listed as a fraction of market capitalization. | ThomsonOne |

| Domestic IO (IO DOM) | Holdings by institutions located in the same country where the stock is listed as a fraction of market capitalization. | ThomsonOne |

| Common-law IO (IO COMMON) | Holdings by institutions located in common-law countries as a fraction of market capitalization. | ThomsonOne |

| Civil-law IO (IO CIVIL) | Holdings by institutions located in civil-law countries as a fraction of market capitalization. | ThomsonOne |

| Control Variables: Firm and Country Characteristics | ||

| Firm size (SIZE) | Log of total assets in thousands of U.S. dollars (WS02999). | Worldscope |

| Sales growth (GROWTH) | Two-year geometric average of annual growth rate in net sales in U.S. dollars (WS01001). | Worldscope |

| Leverage (LEV) | Total debt (WS03255) divided by total assets (WS02999). | Worldscope |

| Cash ( CASH) | Cash and short-term investments (WS02001) divided by total assets (WS02999). | Worldscope |

| Capital expenditures (CAPEX) | Capital expenditures (WS 04601) divided by total assets (WS02999). | Worldscope |

| Market-to-book (MB) | Market value of equity (WS item 08001) divided by book value of equity (WS03501). | Worldscope |

| Return on assets (ROA) | Ratio of net income before extraordinary items (WS01551) plus interest expenses (WS01151) to total assets (WS02999). | Worldscope |

| Property, plant and equipment (PPE) | Property, plant, and equipment (WS02501) divided by total assets (WS02999). | Worldscope |

| Analyst coverage (ANALYST) | Number of analysts following a firm (IBES). | IBES |

| Cross-listing dummy (ADR) | Dummy that equals one if a firm is cross-listed on a U.S. exchange through a level 2–3 ADR or direct listing of ordinary shares, and zero otherwise. | Major Depositary institutions |

| Rule of law (RULE) | Index measures the extent to which the agent has confidence in and abide by the rules of the society in a particular country. | World Bank |

| Pre-crisis dummy (PRE-CRISIS) | Dummy that equals one if the observation falls into pre- crisis period, and zero otherwise. | World Bank |

| Crisis dummy (CRISIS) | Dummy that equals one if the observation falls into crisis period, and zero otherwise. | World Bank |

| Post-crisis dummy (POST-CRISIS) | Dummy that equals one if the observation falls into post- crisis period, and zero otherwise. | World Bank |

| Family controlling 20% (FAMILY) | Dummy that equals one if the ultimate owner is family and owns greater than 20%, and zero otherwise. | ThomsonOne & Annual Reports |

| State controlling 20% (STATE) | Dummy that equals one if the ultimate owner is state and owns greater than 20%, and zero otherwise. | ThomsonOne & Annual Reports |

| Institutional owner controlling 20% (IO) | Dummy that equals one if the ultimate owner is institutional investor and owns greater than 20%, and zero otherwise. | ThomsonOne & Annual Reports |

| Widely held at 20% (WIDLEY) | Dummy that equals one if the firm is widely held at 20%, and zero otherwise. | ThomsonOne & Annual Reports |

References

- Abbott, Lawrence, and Susan Parker. 2000. Audit committee characteristics and auditor selection. Auditing: A Journal of Practice and Theory 19: 47–66. [Google Scholar] [CrossRef]

- Abbott, Lawrence, Susan Parker, Gray Peters, and Kannan Raghunandan. 2003. The association between audit committee characteristics and audit fees. Auditing: A Journal of Practice and Theory 22: 17–32. [Google Scholar] [CrossRef]

- Adams, Renée. 2012. Governance and the financial crisis. International Review of Finance 12: 7–38. [Google Scholar] [CrossRef]

- Adams, Renée, and Daniel Ferreira. 2007. A theory of friendly boards. The Journal of Finance 62: 217–50. [Google Scholar] [CrossRef]

- Aggarwal, Reena, Isil Erel, Miguel Ferreira, and Pedro Matos. 2011. Does governance travel around the world? Evidence from institutional investors. Journal of Financial Economics 100: 154–81. [Google Scholar] [CrossRef]

- Aguilera, Ruth, and Rafel Crespi-Cladera. 2016. Global corporate governance: On the relevance of firms’ ownership structure. Journal of World Business 51: 50–57. [Google Scholar] [CrossRef]

- Aguilera, Ruth, Igor Filatotchev, Howard Gospel, and Gregory Jackson. 2008. An organizational approach to comparative corporate governance: Costs, contingencies, and complementarities. Organization Science 19: 475–92. [Google Scholar] [CrossRef] [Green Version]

- Aguilera, Ruth, Kurt Desender, and Kabbach de Castro. 2012. A Bundle Perspective to Comparative Corporate Governance. In The Sage Handbook of Corporate Governance. Edited by Clarke Thomas and Douglas Branson. New York: Sage Publications, pp. 379–405. [Google Scholar]

- Akbar, Saeed, Buthiena Kharabsheh, Jannine Poletti-Hughes, and Syed Zulfiqar Ali Shah. 2017. Board structure and corporate risk taking in the UK financial sector. International Review of Financial Analysis 50: 101–10. [Google Scholar] [CrossRef] [Green Version]

- Almazan, Andres, Jay Hartzell, and Laura Starks. 2005. Active institutional shareholders and costs of monitoring: Evidence from executive compensation. Financial Management 34: 5–34. [Google Scholar] [CrossRef]

- Anderson, Ronald, and David Reeb. 2004. Board composition: Balancing family influence in S&P 500 firms. Administrative Science Quarterly 49: 209–37. [Google Scholar]

- Aslan, Hadiye, and Praveen Kumar. 2014. National governance bundles and corporate agency costs: A cross-country analysis. Corporate Governance: An International Review 22: 230–51. [Google Scholar] [CrossRef]

- Baccouche, S., Manel Hadriche, and A. Omri. 2014. Multiple directorships and board meeting frequency: Evidence from France. Applied Financial Economics 24: 983–92. [Google Scholar] [CrossRef]

- Barroso, Carmen, Ma Mar Villegas, and Leticia Pérez-Calero. 2011. Board influence on a firm’s internationalization. Corporate Governance: An International Review 19: 351–67. [Google Scholar] [CrossRef]

- Beasley, Mark. 1996. An Empirical Analysis of the relation between board of director composition and financial statement fraud. Accounting Review 71: 443–65. [Google Scholar]

- Beasley, Mark, and Kathy Petroni. 2001. Board independence and audit-firm type. Auditing: A Journal of Practice and Theory 20: 97–114. [Google Scholar] [CrossRef]

- Bebchuk, Lucian, and Michael Weisbach. 2010. The state of corporate governance research. The Review of Financial Studies 23: 939–61. [Google Scholar] [CrossRef]

- Bebchuk, Lucian, Martijn Cremers, and Urs Peyer. 2011. The CEO pay slice. Journal of Financial Economics 102: 199–221. [Google Scholar] [CrossRef]

- Ben-Amar, Walid, and Daniel Zeghal. 2011. Board of directors’ independence and executive compensation disclosure transparency: Canadian evidence. Journal of Applied Accounting Research 12: 43–60. [Google Scholar] [CrossRef]

- Benson, Bradley, Wallace Davidson III, Travis Davidson, and Hongxia Wang. 2015. Do busy directors and CEOs shirk their responsibilities? Evidence from mergers and acquisitions. The Quarterly Review of Economics and Finance 55: 1–19. [Google Scholar] [CrossRef]

- Berberich, Greg, and Flora Niu. 2011. Director busyness, director tenure and the likelihood of encountering corporate governance problems. Paper Presented at CAAA Annual Conference, Toronto, ON, Canada, May 26–29; pp. 1–23. [Google Scholar]

- Beuselinck, Cristof, Belen Blanco, and García Lara. 2017. The role of foreign shareholders in disciplining financial reporting. Journal of Business Finance and Accounting 44: 558–92. [Google Scholar] [CrossRef]

- Boone, Christoph, Bert De Brabander, Woody Van Olffen, and Arjen Van Witteloostuijn. 2002. The genesis of top management team diversity: Selective turnover among management teams in the Dutch Newspaper Publisher Market. Paper Presented at EURAM Conference Proceedings, Stockholm, Sweden, May 9–11; pp. 1–33. [Google Scholar]

- Brav, Alon, Wei Jiang, Frank Partnoy, and Randall Thomas. 2008. Hedge fund activism, corporate governance, and firm performance. The Journal of Finance 63: 1729–75. [Google Scholar] [CrossRef] [Green Version]

- Brickley, James, Ronald Lease, and Clifford Smith. 1988. Ownership structure and voting on antitakeover amendments. Journal of Financial Economics 20: 267–91. [Google Scholar] [CrossRef]

- Cashman, George, Stuart Gillan, and Chulhee Jun. 2012. Going overboard? On busy directors and firm value. Journal of Banking and Finance 36: 3248–59. [Google Scholar] [CrossRef] [Green Version]

- Chhaochharia, Vidhi, Alok Kumar, and Alexandra Niessen-Ruenzi. 2012. Local investors and corporate governance. Journal of Accounting and Economics 54: 42–67. [Google Scholar] [CrossRef]

- Chung, Kee, and Hao Zhang. 2011. Corporate governance and institutional ownership. Journal of Financial and Quantitative Analysis 46: 247–73. [Google Scholar] [CrossRef]

- Conyon, Martin, William Judge, and Michael Useem. 2011. Corporate governance and the 2008–09 financial crisis. Corporate Governance: An International Review 19: 399–404. [Google Scholar] [CrossRef] [Green Version]

- Cook, Michael, and Mully Burress. 2013. The impact of CEO tenure on cooperative governance. Managerial and Decision Economics 34: 218–29. [Google Scholar] [CrossRef]

- Coombes, Paul, and Mark Watson. 2000. Three surveys of corporate governance. McKinsey Quarterly 4: 74–77. [Google Scholar]

- Core, John, Robert Holthausen, and David Larcker. 1999. Corporate governance, chief executive officer compensation, and firm performance. Journal of Financial Economics 51: 371–406. [Google Scholar] [CrossRef]

- Croci, Ettore, Halit Gonenc, and Neslihan Ozkan. 2012. CEO compensation, family control, and institutional investors in Continental Europe. Journal of Banking and Finance 36: 3318–35. [Google Scholar] [CrossRef]

- Cuomo, Francesca, Christine Mallin, and Alessandro Zattoni. 2016. Corporate governance codes: A review and research agenda. Corporate Governance: An International Review 24: 222–41. [Google Scholar] [CrossRef]

- Daines, Robert, Ian Gow, and David Larcker. 2010. Rating the ratings: How good are commercial governance ratings? Journal of Financial Economics 98: 439–61. [Google Scholar] [CrossRef]

- De-la-Hoz, Maria Camila, and Carlos Pombo. 2016. Institutional investor heterogeneity and firm valuation: Evidence from Latin America. Emerging Markets Review 26: 197–221. [Google Scholar] [CrossRef]

- Desender, Kurt, Ruth Aguilera, Rafel Crespi, and Miguel García-Cestona. 2013. When does ownership matter? Board characteristics and behavior. Strategic Management Journal 34: 823–42. [Google Scholar] [CrossRef]

- Díez-Esteban, José María, Jorge Bento Farinha, and Conrado Diego García-Gómez. 2016. The role of institutional investors in propagating the 2007 financial crisis in Southern Europe. Research in International Business and Finance 38: 439–54. [Google Scholar] [CrossRef]

- Dimitras, Augustinos, Maria Kyriakou, and George Iatridis. 2015. Financial crisis, GDP variation and earnings management in Europe. Research in International Business and Finance 34: 338–54. [Google Scholar] [CrossRef]

- Dou, Ying, Sidharth Sahgal, and Emma Jincheng Zhang. 2015. Should independent directors have term limits? The role of experience in corporate governance. Financial Management 44: 583–621. [Google Scholar] [CrossRef]

- Erkens, David, Mingyi Hung, and Pedro Matos. 2012. Corporate governance in the 2007–08 financial crisis: Evidence from financial institutions worldwide. Journal of Corporate Finance 18: 389–411. [Google Scholar] [CrossRef]

- Essen, Marc, Peter-Jan Engelen, and Michael Carney. 2013. Does “good” corporate governance help in a crisis? The impact of country-and firm-level governance mechanisms in the European financial crisis. Corporate Governance: An International Review 21: 201–24. [Google Scholar] [CrossRef] [Green Version]

- Faccio, Maria, and Larry Lang. 2002. The ultimate ownership of Western European corporations. Journal of Financial Economics 65: 365–95. [Google Scholar] [CrossRef]

- Fama, Eugene, and Michael Jensen. 1983. Separation of ownership and control. The Journal of Law and Economics 26: 301–25. [Google Scholar] [CrossRef]

- Ferreira, Miguel, and Pedro Matos. 2008. The colors of investors’ money: The role of institutional investors around the world. Journal of Financial Economics 88: 499–533. [Google Scholar] [CrossRef]

- Ferris, Stephen, Murali Jagannathan, and Adam Pritchard. 2003. Too busy to mind the business? Monitoring by directors with multiple board appointments. The Journal of Finance 58: 1087–111. [Google Scholar] [CrossRef] [Green Version]

- Fich, Eliezer, and Anil Shivdasani. 2006. Are busy boards effective monitors? The Journal of Finance 61: 689–724. [Google Scholar] [CrossRef]

- Fich, Eliezer, Jarrad Harford, and Anh Tran. 2015. Motivated monitors: The importance of institutional investors’ portfolio weights. Journal of Financial Economics 118: 21–48. [Google Scholar] [CrossRef] [Green Version]

- Field, Laura, Michelle Lowry, and Anahit Mkrtchyan. 2013. Are busy boards detrimental? Journal of Financial Economics 109: 63–82. [Google Scholar] [CrossRef]

- Financial Reporting Council. 2010. The UK Corporate Governance Code. Available online: http://www.ecgi.org/codes/code.php?code_id=297 (accessed on 15 June 2017).

- Finkelstein, Sydney, and Donald Hambrick. 1996. Strategic Leadership: Top Executives and Their Effects on Organizations. St. Paul: West Educational Publishing. [Google Scholar]

- Francis, Bill, Iftekhar Hasan, and Qiang Wu. 2012. Do corporate boards matter during the current financial crisis? Review of Financial Economics 21: 39–52. [Google Scholar] [CrossRef]

- Gaitán, Sandra, Hernán Herrera-Echeverri, and Eduardo Pablo. 2018. How corporate governance affects productivity in civil-law business environments: Evidence from Latin America. Global Finance Journal 37: 173–85. [Google Scholar] [CrossRef]

- Gillan, Stuart, and Laura Starks. 2000. Corporate governance proposals and shareholder activism: The role of institutional investors. Journal of Financial Economics 57: 275–305. [Google Scholar] [CrossRef]

- Gillan, Stuart, and Laura Starks. 2003. Corporate governance, corporate ownership, and the role of institutional investors: A global perspective. Journal of Applied Finance 13: 4–22. [Google Scholar] [CrossRef] [Green Version]

- Goranova, Maria, and Lori Ryan. 2014. Shareholder activism a multidisciplinary review. Journal of Management 40: 1230–68. [Google Scholar] [CrossRef] [Green Version]

- Grinstein, Yaniv, and Paul Hribar. 2004. CEO compensation and incentives: Evidence from M&A bonuses. Journal of Financial Economics 73: 119–43. [Google Scholar]

- Gujarati, Damodar. 2003. Basic Econometrics, 4th ed. New York: McGraw-Hill. [Google Scholar]