Abstract

Exchange rate fluctuations could influence economic activity not only via the standard trade channel, but also through a financial channel, which operates through the impact of exchange rate fluctuations on borrowers’ balance sheets and lenders’ risk-taking capacity. This paper explores the “triangular” relationship between (1) the strength of the US dollar, (2) cross-border bank flows and (3) real investment. We conduct two sets of empirical exercises—a macro (country-level) study and a micro (firm-level) study. We find that a stronger dollar is associated with lower growth in dollar-denominated cross-border bank flows and lower real investment in emerging market economies. An important policy implication of our findings is that a stronger US dollar has real macroeconomic effects that go in the opposite direction to the standard trade channel.

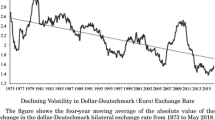

Source: IMF International Financial Statistics and World Economic Outlook; national data; BIS locational banking statistics; Capital IQ; Bloomberg; authors’ calculations

Source: IMF International Financial Statistics and World Economic Outlook; national data; BIS locational banking statistics; authors’ calculations

Source: IMF International Financial Statistics and World Economic Outlook; national data; BIS locational banking statistics; Capital IQ; Bloomberg; authors’ calculations

Source: IMF International Financial Statistics and World Economic Outlook; national data; BIS locational banking statistics; Capital IQ; Bloomberg; authors’ calculations

Similar content being viewed by others

Notes

On the theoretical side, several models with financial frictions predict that exchange rate fluctuations have a balance-sheet effect and generate results according to which depreciation is contractionary if firms have foreign currency-denominated liabilities on their balance sheets (for example, Krugman 1999; Céspedes et al. 2004).

All endogenous variables enter in first differences or growth rates, except for the VIX, which enters in log-levels.

“Appendix A” provides a list of all country groups used in our macro- and micro-level empirical analyses. Panel A of Table 4 contains descriptive statistics of all variables used in our benchmark analysis.

As we demonstrate later in this section, our main results are robust to alternative variables orderings (and, in particular, to moving the exchange rate variable in second position). What is more, most of our key results actually strengthen under those alternative variable orderings.

Panel B of Table 4 contains a summary for the variables used in the micro-level analysis.

Non-tradable sectors include all the industries except the following two-digit SIC codes: 1–14 (agriculture, oil and mining), 20–39 (manufacturing). The classification of the countries’ exchange rate regimes is from the IMF Annual Report on Exchange Arrangements and Exchange Restrictions.

In addition to the specifications presented in this section, we also estimate a number of alternative firm-level specifications in order to test the robustness of our results. More concretely, we demonstrate that our key results are robust to reversing the orthogonalisation procedure for the broad US dollar index and the bilateral exchange rate as well as to controlling for a number of additional country-level variables (GDP per capita, inflation, market capitalization, gross national savings, the share of bank debt) and global variables (US interest rates and the VIX), and. All of those additional results are available upon request.

References

Abrigo, M., and I. Love. 2015. Estimation of Panel Vector Autoregression in Stata: A Package of Programs. University of Hawaii Working Paper.

Arellano, M., and S. Bond. 1991. Some Tests of Specification for Panel Data: Monte Carlo Evidence and an Application to Employment Equations. Review of Economic Studies 58(2): 277–297.

Avdjiev, S., and E. Takats. 2018. Monetary policy spillovers and currency networks in cross-border bank lending: lessons from the 2013 Fed Taper Tantrum. Review of Finance. https://doi.org/10.1093/rof/rfy030.

Avdjiev, S., W. Du, C. Koch, and H.S. Shin. The Dollar, Bank Leverage and the Deviation from Covered Interest Parity. American Economic Review: Insights (forthcoming).

Avdjiev, S., Z. Kuti, and E Takáts. 2012. The Euro Area Crisis and Cross-Border Bank Lending to Emerging Markets. BIS Quarterly Review, December, 37–47.

Bank for International Settlements. 2015. Introduction to BIS Statistics. BIS Quarterly Review, September, 35–51.

Bebczuk, R., A. Galindo, and U. Panizza. 2010. An Evaluation of the Contractionary Devaluation Hypothesis. In Economic Development in Latin America, Palgrave Macmillan, London. 102–117.

Beck, T. 2014. Cross-Border Banking and Financial Deepening: The African Experience. Journal of African Economies 24: 32–45.

Bruno, V., and H.S. Shin. 2015a. Capital Flows and the Risk-Taking Channel of Monetary Policy. Journal of Monetary Economics 71: 119–132.

Bruno, V., and H.S. Shin. 2015b. Cross-Border Banking and Global Liquidity. Review of Economic Studies 82(2): 535–564.

Casas, C., F. Diez, G. Gopinath, and P.-O. Gourinchas. 2016. Dominant Currency Paradigm. NBER Working Paper, 22943.

Cerutti, E., S. Claessens, and L. Ratnovski. 2017. Global Liquidity and Drivers of Cross-Border Bank Flows. Economic Policy 32(89): 81–125.

Céspedes, L.J., R. Chang, and A. Velasco. 2004. Balance Sheets and Exchange Rate Policy. The American Economic Review 94(4): 1183–1193.

Cetorelli, N., and L. Goldberg. 2011. Global Banks and International Shock Transmission: Evidence from the Crisis. IMF Economic Review 59(1): 41–76.

Claessens, S., H. Tong, and I. Zuccardi. 2015. Saving the Euro: Mitigating Financial or Trade Spillovers? Journal of Money, Credit and Banking 47(7): 1369–1402.

Druck, P., N. Magud, and R. Mariscal. 2018. Collateral Damage: Dollar Strength and Emerging Markets’ Growth. The North American Journal of Economics and Finance 43: 97–117.

Du, W., and J. Schreger. 2016. Local Currency Sovereign Risk. Journal of Finance 71(3): 1027–1070.

Eichengreen, B., and H. Tong. 2015. Effects of Renminbi Appreciation on Foreign Firms: The Role of Processing Exports. Journal of Development Economics 116(C): 146–157.

Forbes, K.J., and F. Warnock. 2012. Capital Flow Waves: Surges, Stops, Flight, and Retrenchment. Journal of International Economics 88: 235–251.

Goldberg, L., and S. Krogstrup. 2018. International Capital Flow Pressures. NBER Working Paper, 24286.

Goldberg, L., and C. Tille. 2008. Vehicle Currency Use in International Trade. Journal of International Economics 76(2): 177–192.

Gopinath, G. 2015. The International Price System. In Jackson Hole Symposium, vol. 27. Kansas City Federal Reserve.

Hofmann, B., I. Shim, and H.S. Shin. 2016. Sovereign Yields and the Risk-Taking Channel of Currency Appreciation. BIS Working Papers No. 538.

Kearns, J., and N. Patel. 2016. Does the Financial Channel of Exchange Rates Offset the Trade Channel? BIS Quarterly Review, December 2016, 95–113.

Kim, Y.J., L. Tesar, and J. Zhang. 2015. The Impact of Foreign Liabilities on Small Firms: Firm-Level Evidence from the Korean Crisis. Journal of International Economics 97: 209–230.

Kohn, D., F. Leibovici, and M. Szkup. 2017. Financial Frictions and Export Dynamics in Large Devaluations. Working Paper 2017-013A, Federal Reserve Bank of St. Louis.

Krippner, L. 2015. Zero Lower Bound Term Structure Modeling: A Practitioner’s Guide. Berlin: Springer.

Krugman, P. 1999. Balance Sheets, the Transfer Problem, and Financial Crises. International Tax and Public Finance 6(4): 459–472.

Lütkepohl, H. 2007. New Introduction to Multiple Time Series Analysis. Berlin: Springer.

McCauley, R., McGuire, P. and V. Sushko. 2015. Global dollar credit: links to US monetary policy and leverage. Economic Policy 30(82): 187–229.

McGuire, P., and N. Tarashev. 2008. Bank Health and Lending to Emerging Markets. BIS Quarterly Review, December, 67–80.

Miranda-Agrippino, S., and H. Rey. 2012. World Asset Markets and the Global Financial Cycle. NBER Working Paper, 21722.

Nickel, S. 1981. Biases in Dynamic Models with Fixed Effects. Econometrica 49(6): 1417–1426.

Niepmann, F., and T. Schmidt-Eisenlohr. 2017. Foreign Currency Loans and Credit Risk: Evidence from U.S. Banks. CESifo Working Paper, 67002017.

Peek, J., and E. Rosengren. 1997. The International Transmission of Financial Shocks: The Case of Japan. The American Economic Review 87(4): 495–505.

Peek, J., and E. Rosengren. 2000. Collateral Damage: Effects of the Japanese Bank Crisis on Real Activity in the United States. The American Economic Review 90(1): 30–45.

Rajan, R., and L. Zingales. 1998. Financial Dependence and Growth. The American Economic Review 88: 559–586.

Rey, H. 2015. Dilemma not Trilemma: The Global Financial Cycle and Monetary Policy Independence. NBER Working Paper, 21162.

Schmitt-Grohé, S., and M. Uribe. 2017. Liquidity traps and jobless recoveries. American Economic Journal: Macroeconomics 9(1): 165–204.

Schnabl, P. 2012. The International Transmission of Bank Liquidity Shocks: Evidence from an Emerging Market. Journal of Finance 67(3): 897–932.

Takáts, E. 2010. Was it Credit Supply? Cross-Border Bank Lending to Emerging Market Economies During the Financial Crisis. BIS Quarterly Review, June, 49–56.

Uribe, M. and V. Yue. 2006. Country spreads and emerging countries: Who drives whom? Journal of International Economics 69(1): 6–36.

Acknowledgements

We thank Signe Krogstrup, Amal Mattoo, Linda Tesar, three anonymous referees, participants at the IMF 18th Jacques Polak Annual Research Conference and seminar participants at the Federal Reserve Board for valuable comments and suggestions. Bat-el Berger and Zuzana Filková provided excellent research assistance. The views expressed are those of the authors and not necessarily those of the Bank for International Settlements.

Author information

Authors and Affiliations

Corresponding author

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Paper prepared for the IMF's 18th Jacques Polak Annual Research Conference.

Appendices

Appendix A: Country Groups

1.1 Set of EMEs Used in the Macro (Country-Level) Study

Argentina, Azerbaijan, Brazil, Bulgaria, Chile, Chinese Taipei, Colombia, Costa Rica, Croatia, Czech Republic, Ecuador, Georgia, Hungary, India, Indonesia, Iran, Israel, Korea, Kazakhstan, Malaysia, Mexico, Nigeria, Peru, Philippines, Poland, Romania, Russia, Saudi Arabia, Serbia, Sri Lanka, South Africa, Thailand, Turkey, and Ukraine.

1.2 Set of EMEs Used in the Micro (Firm-Level) Study

Argentina, Azerbaijan, Bulgaria, Brazil, Chile, China, Colombia, Costa Rica, Croatia, Czech Republic, Georgia, Hungary, India, Indonesia, Israel, Korea, Kazakhstan, Malaysia, Mexico, Peru, Philippines, Poland, Romania, Russia, Serbia, South Africa, Thailand, Turkey, Ukraine, Uruguay, Venezuela, and Vietnam.

1.3 Set of EMEs Used in the Micro (Firm-Level) Study with Floating Exchange Rate Regimes

Argentina, Brazil, Chile, Colombia, Czech Republic, Georgia, Hungary, India, Indonesia, Israel, Korea, Malaysia, Mexico, Peru, Philippines, Poland, Romania, Russia, Serbia, South Africa, Thailand, Turkey, Ukraine, and Uruguay.

Appendix B: Data Summary

See Table 4.

Rights and permissions

About this article

Cite this article

Avdjiev, S., Bruno, V., Koch, C. et al. The Dollar Exchange Rate as a Global Risk Factor: Evidence from Investment. IMF Econ Rev 67, 151–173 (2019). https://doi.org/10.1057/s41308-019-00074-4

Published:

Issue Date:

DOI: https://doi.org/10.1057/s41308-019-00074-4