Abstract

Protectionist sentiments have been rising globally in recent years. The consequences of a surge in protectionist measures present policy challenges for emerging markets (EMs), which have become increasingly exposed to global trade. This paper serves two main purposes. First, we collect several stylized facts that characterize EMs’ role in the new geography of trade. We focus on differences between advanced economies (AEs) and EMs in trade linkages, production structures, and factor supplies. Second, we build a dynamic, general equilibrium, quantitative trade model featuring multiple countries, sectors, and factors of production. The model is motivated by and geared to jointly match the facts we present. We use the model to estimate the long-run global impacts of rising trade barriers on EMs—both direct impacts and spillovers through third-country effects. Heterogeneity in openness, production structure, trade linkages, and factor supplies leads to large differences between the impacts on AEs versus EMs. We find that variations in both technological comparative advantage and factor supplies play key roles in shaping these differences.

Similar content being viewed by others

Notes

Végh (2013) presents and discusses the typical macroeconomic approach to studying EMs.

One exception without a focus on EMs is Charbonneau and Landry (2018).

See, for example, Caliendo and Parro (2015).

Timmer et al. (2014) also point out some recent features of trade in value added for EMs. However, their focus is not on this set of countries in particular.

Only 20 AEs and 13 EMs are available for the factor analysis.

Feenstra and Taylor (2017) contains many more details on the growth of China in particular.

Specifically, letting i, h index countries, denoting EMs by \({\mathcal {E}}\) and AEs by \({\mathcal {A}}\), our measures of intra- and inter-group trade are computed as follows.

-

1.

Intra-group trade:

$$\begin{aligned} \frac{{\sum _{h\in {\mathcal {A}}} \sum _{i \in {\mathcal {A}}}X_{ih,t}} +{\sum _{h\in {\mathcal {E}}} \sum _{i \in {\mathcal {E}}}X_{ih,t}} }{\sum _{h\in {\mathcal {I}}} \sum _{i \in {\mathcal {I}}}X_{ih,t}}. \end{aligned}$$ -

2.

Inter-group trade:

$$\begin{aligned} \frac{{\sum _{h\in {\mathcal {A}}} \sum _{i \in {\mathcal {E}}}X_{ih,t}} +{\sum _{h\in {\mathcal {A}}} \sum _{i \in {\mathcal {E}}} X_{ih,t}} }{\sum _{h\in {\mathcal {I}}} \sum _{i \in {\mathcal {I}}}X_{ih,t}}. \end{aligned}$$

-

1.

Excluding China has little impact: the intra-EM share grows from 4 to 9 percent.

See ‘Appendix 2’ for the breakdown of each category. Among these two categories, intermediate goods trade accounts for more than half—56 percent in 2016—of total goods trade, whereas capital goods account for 17 percent. The BEC classification also includes consumption goods trade as a separate category. The patterns are similar to those documented for intermediate and capital goods.

See ‘Appendix 2’ for the breakdown of each category.

We use data from the WIOD 2012 release, as the more recent release does not report data for different skills.

Our model does not consider the possibility of endogenous changes in relative skills through investment in human capital after a shock to trade barriers. We consider this as a relevant channel of adjustment in the very long run, but do not incorporate it to keep our model tractable.

We model these costs following Neumeyer and Perri (2005). We choose this route to introduce trade imbalances in steady state because it introduces stationarity into the model. This feature simplifies the computation of counterfactual equilibria in steady state considerably, as we further discuss in Sect. 6. See Reyes-Heroles (2016) for a similar, but non-stationary model.

Note that we do not consider capital adjustment costs. This assumption is inconsequential for the comparison of steady states; however, such costs matter for the determination of transitional dynamics.

This shifter will be very helpful when we take the model to the data in Sect. 4.

Following the standard quantitative trade literature, we assume perfect competition throughout the main text. The literature is geared toward a long-run view, where competition and entry may be less important for understanding the impacts of trade (see Arkolakis et al. (2018) for a full discussion). Nevertheless, if markets adjust slowly, evolving market structure may be important for transition dynamics (e.g., Amiti et al. (2019) found that tariffs were fully passed through to American consumers during 2018 US–China trade war). Thus, we see our baseline assumption as a shortcoming of the current framework, and an important avenue for the future research.

Specifically, \(\varkappa _{i}^{j} = \left( \nu _{i}^{j} \right) ^{-\nu _{i}^{j}}\left( \left( 1-\nu _{i}^{j} \right) \prod _{m=1}^{J}(\alpha _{i}^{j,k})^{\alpha _{i}^{j,m}}) \right) ^{-\left( 1-\nu _{i}^{j}\right) }\).

Letting \(\varrho ^{j}\left( x^{j}|t\right) \) denote the conditional joint density of the sector-specific vector of productivity draws for all countries, \(x^{j}=\left( x_{1,t}^{j},\ldots ,x_{I,t}^{j}\right) \), these variables are defined for \(G\in \{U,S,K\}\) and \(g\in \{u,s,k\}\) as

$$\begin{aligned} F_{i,t}^{j} =\int _{{\mathbb {R}}_{+}^{I}}f_{i,t}^{j}\left( x^{j}\right) \varrho ^{j}\left( x^{j}|t\right) \text { and } D_{i,t}^{j,m} =\int _{{\mathbb {R}}_{+}^{I}}D_{i,t}^{j,m}\left( x^{j}\right) \varrho ^{j}\left( x^{j}|t\right) {\mathrm{d}}x^{j}. \end{aligned}$$In particular, \(\Gamma ^j=(\Gamma (1+\frac{\left( 1-\eta \right) }{\theta ^j}))^{\frac{1}{1-\eta }}\), where \(\Gamma \left( \cdot \right) \) denotes the Gamma function evaluated for \(z>0\). Note that this equation implies that parameters have to be such that \(\eta -1<\theta \).

We focus on the case of trade barriers even though the model can be equally useful to examine the effects of changes in other types of parameters like productivities or efficiency shifters.

The procedure follows closely that in Reyes-Heroles (2016).

Non-tradable sectors in the model are simply those in which trade barriers across countries are set to infinity. The sets of countries and sectors we consider are described in ‘Appendix 1.’

Details on the data and estimation procedures are provided in ‘Appendix 1.’

The parameter \(\psi \) is not included in the table because this parameter is irrelevant in the steady state of the model.

See Bussière et al. (2013) for other work related to this issue.

Regressing the difference in sectoral shares, \(\Delta y_{i}^j = \chi _i^j - \mu _i^j\) on the foreign trade share, \(x_{i}^j = 1 - \pi _{ii}^j\), and controlling for country fixed effects, yields a statistically significant positive (0.03) coefficient on the foreign trade share.

Given that the model matches the production structure, trade flows, and factor supplies, it delivers measures of factor content of trade that are in line with measures computed without adjusting for trade in inputs.

These negations will cover a UK–EU trade deal but given the short negotiation period and the UK’s stated unwillingness to extend the transition period, there is a significant risk that the UK may leave the EU without a trade deal in place at the beginning of 2021. If this scenario materializes, trade between both parties would no longer be subject to zero tariffs but rather would increase to WTO tariffs.

For example, in 2016, imports and exports by the Netherlands from and to the UK represented about 3 and 6 percent of Dutch GDP, respectively. As a comparison, for Germany, imports and exports from and to the UK represented about 1 and 2.7 percent of German GDP, respectively.

As part of the phase one trade agreement, which went into effect on February 14 of 2020, the USA halved its tariff rate increase from 15 to 7.5 percent on about $100 billion of Chinese goods. China reduced its tariff rate increase from 10 to 5 percent and from 5 to 2.5 percent on about $30 billion of US goods.

See ‘Appendix 1’ for more detail on the construction of the implemented tariffs.

Recent work by Flaaen and Pirce (2019) shows that the US tariffs are associated with relative reductions in manufacturing employment and relative increases in producer prices through rising input costs.

Nevertheless, Bagwell and Staiger do find that some countries would benefit from a trade war over current tariffs. This is a particularly interesting finding in light of current politics.

We choose the median technology in each country as the representative aggregate technology.

As a reference, world exports as a share of world GDP is 17.8 in our data.

The degree of heterogeneity in the full calibration of our model implies that globally solving for transitions is computationally very intensive.

These assumptions are implemented by defining \(u_{i,t}\) as total labor and setting \(\varphi _i^j=1\) for all i and j, \(\sigma =1\), and \(\nu _i^j=\nu _i^{j'}\) for all \(j,j'\), and i.

In the absence of costs associated to NIFA positions, solving for the steady state of the model after a given shock to trade barriers requires knowledge of final NIFA positions. Given that this object is determined by countries’ intertemporal budget constraints, recovering it requires the computation of full transitions. This requirement generates computational challenges as the new steady state of the model becomes endogenous to the relevant shock and initial conditions. An exception would be a model without capital accumulation in which the economy would reach the new steady state immediately after a shock.

Most of these works consider a limited number of sectors (four at the most) (Eaton et al. 2016; Reyes-Heroles 2016; Ravikumar et al. 2019; Mix 2019) rather than the 40 in our baseline calibration; at the most two factors of production and therefore no capital–skill complementarity; a no international financial markets (Caliendo et al. 2019).

The 30 countries include Argentina, Australia, Austria, Brazil, Canada, Chile, China, Denmark, Finland, France, Germany, Greece, Hungary, India, Indonesia, Ireland, Italy, Japan, Mexico, the Netherlands, New Zealand, Norway, Portugal, South Africa, South Korea, Spain, Sweden, Turkey, the UK, and the USA.

References

Aguiar, Mark, and Gita Gopinath. 2007. Emerging Market Business Cycles: The Cycle is the Trend. Journal of Political Economy 115 (1): 69–102.

Alvarez, Fernando. 2017. Capital Accumulation and International Trade. Journal of Monetary Economics 91: 1–18.

Alvarez, Fernando, and Robert Jr Lucas. 2007. General Equilibrium Analysis of the Eaton–Kortum Model of International Trade. Journal of Monetary Economics 54 (6): 1726–1768.

Amiti, Mary, Stephen J. Redding, and David E. Weinstein. 2019. The Impact of the 2018 Tariffs on Prices and Welfare. Journal of Economic Perspectives 33 (4): 187–210.

Arkolakis, Costas, Arnaud Costinot, Dave Donaldson, and Andrés Rodríguez-Clare. 2018. The Elusive Pro-Competitive Effects of Trade. The Review of Economic Studies 86 (1): 46–80.

Bagwell, Kyle, Robert W. Staiger, and Ali Yurukoglu. 2018. Quantitative Analysis of Multi-party Tariff Negotiations, NBER Working Papers 24273, National Bureau of Economic Research, Inc.

Burstein, Ariel, and Jonathan Vogel. 2017. International Trade, Technology, and the Skill Premium. Journal of Political Economy 125 (5): 1356–1412.

Burstein, Ariel, Eduardo Morales, and Jonathan Vogel. 2019. Changes in Between-Group Inequality: Computers, Occupations, and International Trade. American Economic Journal: Macroeconomics 11 (2): 348–400.

Bussière, Matthieu, Giovanni Callegari, Fabio Ghironi, Giulia Sestieri, and Norihiko Yamano. 2013. Estimating Trade Elasticities: Demand Composition and the Trade Collapse of 2008–2009. American Economic Journal: Macroeconomics 5 (3): 118–51.

Caliendo, Lorenzo, and Fernando Parro. 2015. Estimates of the Trade and Welfare Effects of NAFTA. The Review of Economic Studies 82 (1): 1–44.

Caliendo, Lorenzo, Maximiliano Dvorkin, and Fernando Parro. 2019. Trade and Labor Market Dynamics: General Equilibrium Analysis of the China Trade Shock. Econometrica 87 (3): 741–835.

Charbonneau, Karyne B. and Anthony Landry. 2018. The Trade War in Numbers, Technical Report, Bank of Canada Staff Working Paper 2018-57.

Costinot, Arnaud, Dave Donaldson, Jonathan Vogel, and Iván Werning. 2015. Comparative Advantage and Optimal Trade Policy. The Quarterly Journal of Economics 130 (2): 659–702.

Cravino, Javier, and Sebastian Sotelo. 2019. Trade-Induced Structural Change and the Skill Premium. American Economic Journal: Macroeconomics 11 (3): 289–326.

Davis, Donald R., and David E. Weinstein. 2001. An Account of Global Factor Trade. American Economic Review 91 (5): 1423–1453.

Eaton, Jonathan, and Samuel Kortum. 2001. Trade in Capital Goods. European Economic Review 45 (7): 1195–1235. International Seminar On Macroeconomics.

Eaton, Jonathan, and Samuel Kortum. 2002. Technology, Geography, and Trade. Econometrica 70 (5): 1741–1779.

Eaton, Jonathan, Samuel Kortum, Brent Neiman, and John Romalis. 2016. Trade and the Global Recession. American Economic Review 106 (11): 3401–38.

Feenstra, Robert C., and Alan M., Taylor. 2017. International Economics.

Flaaen, Arron, and Justin Pirce. 2019. Disentangling the Effects of the 2018–2019 Tariffs on a Globally Connected U.S. Manufacturing Sector, Finance and Economics Discussion Series Divisions of Research & Statistics and Monetary Affairs Working Paper-086.

García-Cicco, Javier, Roberto Pancrazi, and Martín Uribe. 2010. Real Business Cycles in Emerging Countries? American Economic Review 100 (5): 2510–31.

Grant, Matthew. 2019. Why Special Economic Zones? Using Trade Policy to Discriminate Across Importers, Unpublished Manuscript, Stanford University.

Hanson, Gordon H. 2012. The Rise of Middle Kingdoms: Emerging Economies in Global Trade. Journal of Economic Perspectives 26 (2): 41–64.

IMF. 2019. World Economic Outlook, Technical Report, April 2019 World Economic Outlook Analytical Chapter 4.

Johnson, Robert C. 2014. Five Facts About Value-Added Exports and Implications for Macroeconomics and Trade Research. Journal of Economic Perspectives 28 (2): 119–42.

Levchenko, Andrei A., and Jing Zhang. 2016. The Evolution of Comparative Advantage: Measurement and Welfare Implications. Journal of Monetary Economics 78: 96–111.

McLaren, J. 2016. Chapter 2: The Political Economy of Commercial Policy. In Handbook of Commercial Policy, vol. 1, ed. Kyle Bagwell, and Robert W. Staiger, 109–159. North-Holland: Elsevier.

Mendoza, Enrique G. 2010. Sudden Stops, Financial Crises, and Leverage. American Economic Review 100 (5): 1941–66.

Mendoza, Enrique G., and Linda L. Tesar. 1998. The International Ramifications of Tax Reforms: Supply-Side Economics in a Global Economy. American Economic Review: 226–245.

Mix, Carter. 2019. Technology, Geography, and Trade Over Time: The Dynamic Effects of Changing Trade Policy. (Manuscript).

Montiel, Peter J. 2011. Macroeconomics in Emerging Markets. Cambridge: Cambridge University Press.

Morrow, Peter M., and Daniel Trefler. 2017. Endowments, Skill-Biased Technology, and Factor Prices: A Unified Approach to Trade, NBER Working Papers 24078, National Bureau of Economic Research, Inc.

Neumeyer, Pablo A., and Fabrizio Perri. 2005. Business Cycles in Emerging Economies: The Role of Interest rates. Journal of Monetary Economics 52 (2): 345–380.

Ossa, Ralph. 2014. Trade Wars and Trade Talks with Data. American Economic Review 104 (12): 4104–4146.

Parro, Fernando. 2013. Capital-Skill Complementarity and the Skill Premium in a Quantitative Model of Trade. American Economic Journal: Macroeconomics 5 (2): 72–117.

Ravikumar, B., Ana Maria Santacreu, and Michael Sposi. 2019. Capital Accumulation and Dynamic Gains from Trade. Journal of International Economics 119: 93–110.

Reyes-Heroles, Ricardo. 2016. The Role of Trade Costs in the Surge of Trade Imbalances, (Manuscript).

Timmer, Marcel P., Abdul Azeez Erumban, Bart Los, Robert Stehrer, and Gaaitzen J. de Vries. 2014. Slicing Up Global Value Chains. Journal of Economic Perspectives 28 (2): 99–118.

Timmer, Marcel P., Erik Dietzenbacher, Bart Los, Robert Stehrer, and Gaaitzen J. de Vries. 2015. An Illustrated User Guide to the World Input–Output Database: The Case of Global Automotive Production. Review of International Economics 23 (3): 575–605.

Trefler, Daniel. 1995. The Case of the Missing Trade and Other Mysteries. The American Economic Review: 1029–1046.

Trefler, Daniel, and Susan Chun Zhu. 2010. The Structure of Factor Content Predictions. Journal of International Economics 82 (2): 195–207.

UNCTAD. 2004. The New Geography of International Economic Relations, Background Paper No. 1.

Uribe, Martín, and Vivian Z. Yue. 2006. Country Spreads and Emerging Countries: Who Drives Whom? Journal of International Economics 69 (1): 6–36. Emerging Markets.

Végh, Carlos A. 2013. Open Economy Macroeconomics in Developing Countries. Cambridge: MIT Press.

Author information

Authors and Affiliations

Corresponding author

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

We thank participants at the MF-CBC-IMFER ‘Current Policy Challenges Facing Emerging Markets’ conference, the EIIT conference, and the International Finance workshop (Federal Reserve Board) for valuable comments. We are very grateful to Sebastian Claro for discussing the paper as well as the editorial committee of the IMF-CBC-IMFER conference and two anonymous referees for constructive comments and suggestions. We also thank Charlotte Singer for excellent research assistance. The views in this paper are solely the responsibility of the authors and should not be interpreted as reflecting the views of the Board of Governors of the Federal Reserve System or of any other person associated with the Federal Reserve System.

Appendices

Appendix 1: Data Sources and Calibration

1.1 Facts 1–5

To document facts 1–5, we use data at the HS-6 level from UN Comtrade from 1996 to 2016. We rely on the BEC classification system outlined in ‘Appendix 2’ to classify traded goods as intermediate, consumption, and capital goods.

We consider 56 countries and one rest of the world aggregate for our analysis of these facts. We classify 21 countries as EMs: Argentina, Bulgaria, Brazil, China, Chile, Colombia, Croatia, Hungary, India, Indonesia, Mexico, Malaysia, Peru, Philippines, Poland, Romania, Russia, South Africa, Thailand, Turkey, and Vietnam. We also classify the rest of the world aggregate as an EM. The AEs encompass 35 countries: Australia, Austria, Belgium, Canada, Cyprus, Czech Republic, Denmark, Spain, Estonia, Finland, France, Germany, Greece, Hong Kong, Ireland, Israel, Italy, Japan, Lithuania, Latvia, Luxembourg, Malta, Netherlands, Norway, New Zealand, Portugal, Singapore, Slovakia, Slovenia, South Korea, Sweden, Switzerland, Taiwan, the UK, and the USA.

These 56 countries have trade data available for the entire period and represent 91 percent of world trade and 91 percent of world GDP. The AE and EM classification is based on that of the IMF World Economic Outlook (WEO) for 2018.

Data on nominal GDP to construct openness measures come from the IMF WEO for 1996–2016. We include 56 main countries, including 34 AEs, 22 EMs, and one aggregate rest of the world.

1.2 Fact 6

To document fact 6, we consider data from the World Input–Output Database (WIOD) 2013 release and the associated 2014 release of the Socio-Economic Accounts (SEA). The SEA considers three different types of labor according to skill levels: low, medium, and high skill. These data are readily available from 1995 to 2009.

1.3 Model Calibration

For the calibration of the model, we consider 31 countries: 30 core countries and an aggregate that we label rest of the world (ROW). The following is the list of the countries we consider to calibrate our model.

-

AEs [20] Australia (AUS), Austria (AUT), Germany (DEU), Canada (CAN), Denmark (DNK), Spain (ESP), Finland (FIN), France (FRA), Italy (ITA), Greece (GRC), Ireland (IRL), Japan (JPN), Korea (KOR), the Netherlands (NLD), New Zealand (NZL), Norway (NOR), Portugal (PRT), Sweden (SWE), the UK (GBR), and the USA (USA).

-

EMEs [11] Argentina (ARG), Brazil (BRA), Chile (CHL), China (CHN), Hungary (HUN), Indonesia (IDN), India (IND), Mexico (MEX), Turkey (TUR), South Africa (ZAF), Rest of the World (ROW).

Table 2 shows the sectors we consider, which are the same as in as in Caliendo and Parro (2015).

-

1.

Trade We use bilateral trade from the United Nations Statistical Division Commodity Trade (UNCOMTRADE) database for 2016 at the Harmonized System 6-digit (HS-6) level. We include 30 separate countries, which together account for more than 85 percent of world GDP, and a ROW modeled as one aggregate block.Footnote 44 We map these HS-6 product level codes to the 20 tradable sectors as in Caliendo and Parro (2015) using the HS-ISIC concordance tables.

-

2.

Tariffs We collect tariff data for 2016 from the United Nations Statistical Division-Trade Analysis and Information System (UNCTAD-TRAINS) and Most-Favored Nation (MFN) databases for the same 30 countries and a ROW average. The UNCTAD TRAINS data contain bilateral tariffs at the Harmonized System 6-digit (HS-6) product level. The MFN data provide importer-specific MFN tariff rates, which is also at the HS-6 product level.

We then aggregate the HS-6 product level tariff data to sectoral tariffs by using bilateral trade weights for all the HS-6 level trade flows within a sector. All told, we compute 31 by 31 bilateral tariffs for each of the 20 tradable sectors in 2016 and assume infinitely large trade barriers for the 20 non-tradable sectors to serve as our baseline. The implemented and proposed tariffs are taken from the lists released by the United States Trade Representative (USTR) and China’s Ministry of Commerce (MOFCOM). The published lists typically disaggregate goods at the HS-10 product level. Therefore, when computing the imposed and prospective tariffs for our counterfactual analysis, we convert the HS-10 product level codes to HS-6 product level codes.

-

3.

Input–output tables We use the World Input–Output Database (WIOD)Footnote 45 for 2014 to compute the input–output coefficients as the total dollar value of an input sector’s intermediate goods divided by the total dollar value of the output sector’s inputs. The last year with available data in the 2016 release of the WIOD is 2014. We supplement these data with the OECD’s input–output (I–O) tables for 2011 for those countries that are not included in WIOD.

-

4.

Gross output and value added We use sectoral gross output and value added data from the OECD STAN database for 2016. We supplement these data with the sectoral gross output and value added data from the Socio-Economic Accounts (SEA), the United Nations’ INDSTAT2 and the National Accounts databases. We construct value added shares for our model as the ratio of a sector’s value added to gross output.

-

5.

Factors of Production We consider aggregate data on capital and labor from the Penn World Tables (PWT) latest release. We then consider skill share provided in the SEA release 2014 of the WIOD. We define low-skill workers as those workers classified as either low skill or medium skill in the data for the year 2009, which is the latest year for which these data are available.

-

6.

Sectoral Expenditure Shares To construct sectoral expenditure shares, we consider data from the WIOD 2016 release for the year 2014.

-

7.

Factor and Sectoral prices To recover data on factor prices, we rely on data for factor compensations and endowments. We consider factor compensation for capital and total labor for 2014 from the SEA 2016 release. We then use labor compensation shares across skill groups from the SEA 2014 release for the year 2009. This procedure is similar to the one followed in Reyes-Heroles (2016). We estimate sectoral prices by exploiting the sector-specific gravity structure of our model following the exact same procedure as in Reyes-Heroles (2016).

Appendix 2: BEC Goods Classification

-

1.

Intermediate goods

-

121—Food and beverages, processed, mainly for industry

-

21—Industrial supplies not elsewhere specified, primary

-

22—Industrial supplies not elsewhere specified, processed

-

322—Fuels and lubricants, processed (other than motor spirit)

-

42—Parts and accessories of capital goods (except transport equipment)

-

53—Parts and accessories of transport equipment

-

-

2.

Commodities (excluding oil)

-

111—Food and beverages, primary, mainly for industry

-

112—Food and beverages, primary, mainly for household consumption

-

-

3.

Capital goods

-

41—Capital goods (except transport equipment)

-

521—Transport equipment, industrial

-

-

4.

Other

-

122—Food and beverages, processed, mainly for household consumption

-

31—Fuels and lubricants, primary

-

321—Fuels and lubricants, processed (motor spirit)

-

51—Passenger motor cars

-

521—Transport equipment, industrial

-

522—Transport equipment, non-industrial

-

61—Consumer goods not elsewhere specified, durable

-

62—Consumer goods not elsewhere specified, semi-durable

-

63—Consumer goods not elsewhere specified, non-durable

-

7—Goods not elsewhere specified

-

Appendix 3: Calibration of Model in Sect. 6.2

To calibrate the version of our model considered in Sect. 6.2, we first aggregate the relevant data considered in Sect. 5 to four countries (USA, China, AEs excl. the USA, and EMs excluding China) and three sectors (agriculture and mining, manufacturing, and services). We then follow the same procedure as in Sect. 5 to discipline parameters and labor endowments. However, we choose a different strategy to calibrate sectoral productivities. First, we recover trade barriers using Head–Ries indices, implying that we assume symmetric trade barriers. Then, we proceed to set investment efficiencies equal to one around the world and calibrate sectoral productivities such that, in its initial steady state, the model matches as close as possible data on domestic trade shares and country GDP shares. It is possible to consider this strategy given that solving for the steady state of the smaller model is significantly faster than for the baseline calibration of our model.

Appendix 4: Additional Figures

See Figs. 19, 20, 21, 22, 23, 24, 25, 26, and 27.

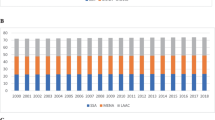

Total exports ($ trillions)

EM and AE trade openness (exports + imports as a share of GDP)

EM and AE trade openness excluding China (exports + imports as a share of GDP)

EM and AE trade openness (imports as a share of GDP)

EM and AE trade openness excluding China (imports as a share of GDP)

Total intra- and inter-group exports ($ trillions)

Intra-group exports ($ trillions)

Importance of EMs in intermediate and capital goods trade

Trade among EMs ($ trillions)

Rights and permissions

About this article

Cite this article

Reyes-Heroles, R., Traiberman, S. & Van Leemput, E. Emerging Markets and the New Geography of Trade: The Effects of Rising Trade Barriers. IMF Econ Rev 68, 456–508 (2020). https://doi.org/10.1057/s41308-020-00117-1

Published:

Issue Date:

DOI: https://doi.org/10.1057/s41308-020-00117-1