Abstract

Over the past decades, exit has been analyzed at the theoretical and empirical levels. From this rich series of contributions, two basic patterns of exit can be identified: the revolving door and the gale of creative destruction. In the first, the liability of newness plays a major role in the exit process, while in the second the displacement of non-innovators is the driver of exit. We have tested these two patterns of exit on the population of Dutch firms that exited in 2018. We find confirmation that the two patterns characterize different types of industries. In industries in which innovation does not play a major role, the revolving door effect is the typical pattern and exit is concentrated among the adolescent firms. These firms are also small in size. On the contrary, in industries in which innovation plays a role, exit takes place both among infant as well as mature firms. Exiters are not necessarily only the smaller firms. While a highly innovative and uncertain environment can threaten the survival of infant firms, the exit of mature firms is driven by the innovation of young firms, following the gale of creative destruction.

Similar content being viewed by others

1 Introduction

The exit of firms represents a key dimension of industrial dynamics. Over the past decades, exit has been analyzed in various ways: at the theoretical level by evolutionary models and by more traditional contributions, and at the empirical level by qualitative cases of individual firms or industries, by quantitative longitudinal analyses and by cross-industry studies. From this rich series of contributions, it has emerged as “stylized facts” that entry and exit rates are common and are also highly correlated across industrial sectors (Caves 1998; Dunne et al. 1988; Geroski 1995). These empirical regularities at the aggregate level have been explained on the basis of two basic patterns of exit. One pattern emphasizes that entry and exit are correlated. This is the so called “revolving door” metaphor (Audretsch 1995; Dunne et al. 1988) in which the “liability of newness” leads new firms to have a high probability of exit after a short period of activity. On this basis, exits are attributed to a “natural churning” that is more remarked in some industries than in others, because of idiosyncratic factors acting symmetrically as barriers to entry and exit (Manjón-Antolín 2010). Exit remains nevertheless a ‘white noise at the fringe of an industry '(Audretsch 1995, p. 590). The other pattern highlights that exit is related to innovation, because the Schumpeterian “gale of creative destruction” (Schumpeter 1934 , 1942) leads to the fall of those firms that are not able to cope successfully with the new technologies. In this pattern, described by the “forest” metaphor (Audretsch 1995; Marshall 1920) of young trees striving to grow in the shade of old trees, established firms are displaced by new innovative firms. Hence, churning may affect the core of an industry. This exit pattern is more likely to occur in industries in which technological and demand conditions favor the entry of innovative firms (Manjón-Antolín 2010) simultaneously to the displacement of less innovative incumbents, in a so called “entrepreneurial regime” as opposed to a “routinized regime” of innovation (Almudi et al. 2019; Almudi et al. 2013; Audretsch 1995; Breschi et al. 2000; Dosi et al. 1995; Dosi et al. 2017; Winter 1984).

This paper empirically identifies these two patterns and examines their relevance across all industries. Most studies on exit patterns have tested for cross-sectional correlations in exit and entry rates over time and across sectors. Some of these studies have also accounted for firm-specific heterogeneity such as firm size. Generally, these studies apply a “prospective cohort study” approach, examining the current incidence of exit among the exposed cases in a cohort of new firms (or entry cohort) moving forwards over time. In our analysis, we adopt a “retrospective cohort study” approach, starting with all the exits taking place in a certain year (or exit cohort) and looking backwards over time at its composition, in relation to firm-specific and industry-specific heterogeneity. This approach enables us to characterize the dynamics that have preceded an exit event.

The analysis is based on business demographic data for the Dutch economy. We consider all firms that exited in 2018 (our last year of observation) as the reference exit cohort. In order to ascertain the exit patterns, we examine retrospectively the composition of firms in the exit cohort by year of creation (or birth cohort) and size (as measured by number of employees). Under a “revolving door pattern”, we expect that the distribution of firms in the exit cohort is highly skewed with most of the firms concentrated in the birth cohorts immediately preceding the year of exit (2018). In this scenario, we also expect that the size of the exiting firms has remained small over their life cycle for each birth cohort. This reflects recently created small firms, rapidly exiting the market without a significant growth in size. Hence, in the whole exit cohort, the contribution to employment creation by each birth cohort will be marginal at any time. In other words, the exit cohort would be composed of relatively young and small firms that have remained at the fringe of an industry throughout their life cycle. Conversely, under a “Schumpeterian gale of creative destruction pattern”, we expect that firms in the 2018 exit cohort are more evenly distributed across birth cohorts, because exit occurs also among older firms. Furthermore, the exit cohort is likely to display greater variability in firm size over time per birth cohort, because some of the exiting firms will have reached a more prominent position in the market before collapsing in a process of dynamic competition. As a result, the contribution to employment creation (and the corresponding employment destruction) by the exiting firms will be sizeable for the older birth cohorts. This implies that firms in the exit cohort have moved up towards the center of the industry at some point of their lifecycle.

Having defined a cohort’s exit pattern on the basis of the year of firm creation and after following the subsequent employment dynamics of the exiting firms, we examine how this pattern differs across industries that present different technological and competitive environments at the time the exiting firms were created. This enables us to establish how the balance between a “revolving door” pattern and a “Schumpeterian gale of creative destruction” pattern emerging from the analysis of the exit cohort relates to the underlying structural conditions of industries at the year of entry. By doing so, our study offers a novel approach to explore the effects of the initial conditions that firms experience at the time of founding (Geroski et al. 2010; Hyytinen et al. 2015) on their subsequent exit path.

The paper is organized as follows. Section 2 discusses two different stylized facts regarding the exit process; in Section 3 we present the data, the variables and the relationships that we aim to investigate. Then Section 4 contains the descriptive statistics and the results of the multivariate analysis conducted at the industry level. Finally, in Section 5 we draw some conclusions from the empirical analysis.

2 Two different stylized facts on the process of exit of firms from industries

For a long time, the analysis of exit of firms has not been at the core of the empirical and theoretical analyses in the literature in industrial economics and industrial dynamics. Only in recent decades an increasing number of contributions have focused on exit. Detailed case studies, quantitative longitudinal or cross-industry analyses and models following an evolutionary or a mainstream neoclassical approach have shed light on various aspects of this key phenomenon. In this paper, it is not our aim to summarize the whole literature on entry, which has already been done, among others, in Audretsch (1995), Cefis and Marsili (2011) and Wennberg and DeTienne (2014). Rather, from the wide literature on exit we aim to highlight only those themes that are going to be relevant for the empirical analysis conducted in this paper.

A first aspect that we want to emphasize is the link of exit with industrial dynamics and the evolution of market structure. In this respect, a large literature has inserted exit in a series of “stylized facts” on industrial dynamics that have substantially changed the conventional way of looking at industries by highlighting the rich interaction between entry, exit and the changing market structure of industries. First, relatively high rates of entry and exit of firms are present in virtually all industries, even those with high capital intensity and other apparent barriers to entry. In addition, exit and entry rates tend to be strongly correlated (Bartelsman et al. 2005; Dunne et al. 1988). They are significantly higher in new industries and decline as industries mature. However, even relatively mature industries are often characterized by continuing entry and exit. The vast majority of entrants are small firms, and most of them exit the industry within a few years. Those new firms that manage to survive grow faster than incumbents, reaching average levels of productivity gradually over time. Even in relatively mature industries (Lieberman 1990) one often observes persistent turbulence and churning in the profile of industrial evolution, due not only to continuous entry and exit but also to changes in the incumbents’ market shares (Acs and Audretsch 1989, 1990; Bartelsman et al. 2005). These empirical findings concerning entry, exit and the dynamics of market structure have been replicated by various evolutionary models centered on the basic processes of learning and selection, from the seminal work of Nelson and Winter (1982) and Winter (1984) to the more complex contributions by Dosi et al. (1995), Dosi et al. (2017), Winter et al. (2000), and the more context-specific history-friendly models of innovation and industry evolution (Malerba et al. 2016). However, also in the more mainstream literature on industrial dynamics, the evolutionary metaphor has been increasingly and explicitly used, as one can see in the passive or active learning models of entry and selection (such as in the work by Jovanovic (1982); Jovanovic and MacDonald (1994); and Ericson and Pakes (1995)).

A research tradition different from the one associating exit with the entry of new firms, has related the exit of new as of well-established firms to the gale of creative destruction that innovation generates in industries (Baptista and Karaöz 2009; Cefis and Marsili 2006; Colombelli et al. 2016; Fontana and Nesta 2009; Ortiz-Villajos and Sotoca 2018). According to this view, innovation not only eliminates those new firms who are not innovative but also displaces incumbents tied to old technologies, products and production processes (Schumpeter 1934, 1942). It must be noted that the reasons that are at the base of the displacements of established firms are different from the ones concerning the exit of new firms in these contexts. The learning process by incumbents may often be myopic, focusing on what these firms are successfully doing and ignoring the long-run, the larger picture and the emergence of novelty (Dosi et al. 2000). Thus, competence traps may occur, in the sense that the same competences that give rise to the market success of a firm are at the base of the mechanisms that lead to the failure of that firm later on, when new technologies emerge. By focusing too much and for too long time on their core capabilities firms may turn them into core rigidities, which block adaptation and the rapid reaction to change (Leonard-Barton 1992). In the presence of inertia and competence traps, radical innovations may become competence destroying and lead to the failure and exit of incumbents. In fact, those incumbents with routines and capabilities related to the old technologies often are not be able to switch forcefully or rapidly to the new technologies (Tushman and Anderson 1986). It is possible to enlarge the analysis of displacement to architectural innovations, which introduce implicit change in new system products. Here changes may not be so easily and clearly identifiable by those established firms which produce successful systems. As a consequence, when implicit changes are introduced by competitors, current leaders may not recognize them as superior and thus may continue to focus on their established architectures. But the market and the consumers may rapidly switch to the new products with new architectures, so that incumbents may lose very quickly their advantages and have to exit the market (Henderson and Clark 1990). In addition, some innovations are disruptive in a sense that they may initially underperform existing products by incumbents in mainstream markets but have some features that are appealing to a small niche – generally new customers. Over time, these innovations have a trajectory that create products with a greater performance with respect to existing products, so that they become appealing also to mainstream customers. This leads to the disruption of existing products and the failure of market leaders (Christensen 1997). Finally, some innovations may be related to the emergence of a dominant product in the market and the stream of process innovations that follows. The emergence of a dominant design and of process innovations usually lead to the dominance of few firms, a reduction in the entry of new firms and a major surge of exit of existing firms. In general, the industry shakeout and the drastic reduction in the number of producers takes place over a relatively short time span (Abernathy and Utterback 1978; Gort and Klepper 1982; Klepper 1996, 1997). In sum, in all these different cases, innovation in products and processes causes the exit of incumbents as well as of new firms.

Finally, in dealing with firms that exit an industry, the literature has taken two different routes. The first has considered exit as an undifferentiated disappearance of firms, related to the fact that some firms are not active anymore in the economy or in an industry. The second has examined exit in a more articulated way, in which the specific way of exit from an industry is taken into account. In general, exit may have three basic modes: geographic relocation and radical restructuring, business closure (either voluntary liquidation or bankruptcy) or merger and acquisition (Balcaen et al. 2011; Cefis and Marsili 2012; DeTienne et al. 2015; Schary 1991). The choice of the exit mode depends on a variety of factors, ranging from the profitability and innovativeness of the firm, to the characteristics of the decision process within a firm, the amount of financial assets available, and the size of the firm. The three modes of exit mentioned above differ in several respects. Exit by relocation and restructuring is part of the dynamic process that involves the modification of firms’ products and processes. This implies that a firm may exit an industry but not the economy, because the firm may move to another industry. This mode is often undertaken when past performance in an industry is poor and may be caused by a low level of demand in that industry. Differences in the ease by which firms relocate depend on the level of firms’ capabilities, in that more capable firms are better able to move from one industry to another. Exit by dissolution may take place in two different ways – voluntary liquidation and bankruptcy (Balcaen et al. 2011). The former happens out of court and is preferred when cash reserves are significant and the leverage is low (Erwin and McConnell 1997). Bankruptcy on the other hand is an in-court procedure that involves higher transaction costs, and often takes place when the company has a high level of secured debt (Balcaen et al. 2011). Finally, mergers and acquisitions involve the transfer of ownership, while production capacity remains within the industry. They often take place in order to seize growth opportunities. Usually large firms tend to be involved in mergers, particularly when the entities involved are part of a group (Balcaen et al. 2011; Buehler et al. 2006). Given that the aim of this paper is to provide a broad and cross-industry examination of exit over a long period of time, we have chosen to consider exit in terms of passage from an active status to a non-active status, without entering into an analysis of the specific mode of exit. An analysis of all the various modes of exit would have made this paper too rich and too complex. However, some of the authors of the present paper have already done some work in this direction (Cefis and Marsili 2011, 2012), by considering the three above-mentioned modes of exit and their different economic meanings.

Inspired by the literature discussed above, this paper aims to test the relevance of two basic stylized patterns regarding the exit of firms from industries: the “revolving door effect” and “the gale of creative destruction”. The “revolving door effect” links exit to the “liability of newness” and to the fact that entrants are inexperienced, they may lack managerial skills and often they do not have the required technological, organizational or marketing capabilities to survive in an industry. Moreover, new firms may not have the appropriate level of financing nor benefit from a supporting network in terms of suppliers, partners and customers (Audretsch 1995; Dunne et al. 1988; Wennberg and DeTienne 2014). In all these cases, exit takes place among the youngest and the smallest firms, while the core of the industry is mostly left untouched by exit. In sum, the churning of firms occurs at the margin of the industry.

The “gale of creative destruction”, on the contrary, links exit to innovation, often introduced by the entrants in an industry. Here the basic reference is Schumpeter (1934, 1942) and the related Schumpeterian patterns of innovation (Malerba and Orsenigo 1995). According to this view, exit does not take place only (or mostly) among the newly entered firms, as in the “revolving door” case. Exit may also affect those incumbents that are not innovative enough and are not able to react to the innovations introduced by competitors. In this pattern, exit takes place through a “displacement effect” of new as well as old firms.

The characterization along these lines of the exit patterns of young firms can also help to a better understanding of the role of entrepreneurial firms in shaping the overall dynamic of industrial structure. Scholars have pointed out that such a role varies extensively. It can range from the one of “marginal firms” that are created and rapidly closed leaving an industry structure unaffected, to the one of fast growing firms or “gazelles” responsible for a large share of job creation in an industry. It must be noted that this variety of roles bears implications for resource allocation and policy making (Nightingale and Coad 2014). While in this paper we emphasize firm-specific and industry-specific sources of variety, there are also individual factors affecting the exit of entrepreneurial firms, due to the motivation and the experience of the business founders. Exit patterns partly reflect the subjective decision of the founders to exit in view of their own opportunity costs, personal motivations, and career alternatives (DeTienne et al. 2015; Gimeno et al. 1997). From an individual-based perspective, the Schumpeterian gale of creative disruption can be seen as associated with the dream and ambition to pursue novel opportunities, in contrast to the choice to engage in entrepreneurship motivated by low opportunity costs and lack of an alternative occupation, more likely to generate churning at the margin of the industry (Amit et al. 1995; Shane and Venkataraman 2000). It is also possible that at the aggregate level a “revolving door” exit pattern overlaps with the re-entry of serial entrepreneurs, something that been labeled “revolving door entrepreneurship” (Hessels et al. 2010).

Adopring an industrial dynamics perspective, in the next Sections we will test the relevance of the two patterns of firm exit discussed above (churning versus displacement) in the population of Dutch companies that exited in 2018. We will then relate the relevance of one or the other pattern to firm-specific characteristics, distinguishing between unlimited and limited liability businesses ( indicative of different types of entrepreneurship and entrepreneurial risk), and to industry-specific factors expressing the nature of the technological environment and the intensity of market competition.

3 Data and methods

3.1 Data

The analysis is conducted considering two different databases collected and managed by the Central Bureau of Statistics (CBS) Netherlands, namely the General Annual Business Register (ABR) and the Community Innovation Survey (including successive waves from CIS 2004 to CIS 2016). The ABR is a longitudinal database containing information on the demography and structure of the population of firms operating in the Netherlands. It reports the dates in months of the first inclusion and exclusion of firms from the register, according to the records provided by the Chamber of Commerce and the Tax Register, for the entire population of firms registered for fiscal purposes in the Netherlands. Hence, given the completeness of the dataset, the registered data allow us to identify firm entries and exits in the Netherlands. In addition, the ABR reports the number of employees, main industrial sector and legal form of firms per year. The ABR data was available for the years 1994–2018. The CIS surveys are based on harmonized innovation questionnaires conducted at the European level under the supervision and coordination of Eurostat. They are designed to gather detailed micro-level information on the innovative activities performed by firms. In the Netherlands, CISs have been collected from 1994 with a 2-year interval. The latest CIS available is the 2016 one.

3.2 Sample and variables

Compared to classic survival studies, the analytical framework we adopt works with an inverted logic, reconstructing firms’ life-spell retrospectively from the date of exit, instead of monitoring them up to a pre-defined point in time. The initial sample is composed by all firms whose exit is registered in the ABR in 2018. The focus of our analysis is thus the exit cohort of 2018. Within this exit cohort, firms are then tracked backwards, up to their year of entry. Because the earliest ABR dataset we have access to is 1994, we do not track firms entered before January 1994 (i.e. more than 25 years of age at exit). In order to control for the heterogeneity of modes of entry we limit our analysis of exits in 2018 to newly created firms (or greenfield entrants) only. Hence, we exclude all new entrants directly related to previously existing firms, due to spin-off, merger, restructuring or other radical transformations of the parent firm. This totals to 13,341 firms. As a result, we obtained an unbalanced panel of 133,267 firms created between 1994 and 2018 and exiting in 2018, across all sectors of activity. As descriptive statistics, we report the distribution of exits and the average number of employees by birth cohort, up to the 1994 cohort. We then carry out a more detailed analysis of the quartiles of the employment distribution by birth cohort, focusing on the 15 most recent cohorts, in order to disentangle the employment dynamics of the younger exiting firms (i.e. born between 2004 and 2018) from the more established firms. This has the purpose of identifying the rates of growth that new firms are able to achieve before exiting in various settings. This subset is composed of 127,012 firms (equal to 95.3% of all exits).

Our variable of interest is the industry-specific exit rate per birth cohort calculated for all firms in a given exit cohort (in our case 2018)Footnote 1:

where nxsc is the total number of exits in sector s = 1, …, m and birth cohort (year) c = 1, …, k for a given exit cohort. Specifically, it indicates the percentage of exits observed in 2018 by firms in a certain birth cohort as a proportion of all birth cohorts. In other words, it expresses how prevalent a certain birth cohort is among all firms exiting in a given (2018) exit cohort. In order to characterize the nature of the technological and competitive environments which may affect the exit pattern in an industry, being more similar to a “revolving door” or to a “Schumpeterian gale of creative destruction”, we focus on the conditions characterizing the industry environment at the time firms in the 2018 exit cohort were created. Founding conditions have been shown to have a long-lasting imprinting effect on the life and the exit of new firms (Geroski et al. 2010). Hence, we construct a number of indicators at the level of 2-digit sectoral code (defined according to the 2008 Standard Industrial Classification) by year of firm creation, for all birth cohorts from 2004 to 2018. For this purpose, we use the ABR and the CIS providing employment and innovation data by industry at the year of birth. We then relate the exit rate by birth cohort to the sectoral indicators by birth cohort, obtaining a ‘collapsed’ panel where the time dimension is the year of birth, ranging from 2004 to 2018.

Because the Business Register (ABR) encompasses the whole population of firms in the country, it is possible to calculate measures of concentration and industrial dynamics. From the ABR we first calculate two alternative indicators of industrial concentration:

C4 concentration ratio: sum of the employment shares of the 4 largest firms in a given industrial sector, defined as \( C{4}_{sc}={\sum}_{j=1}^4{s}_{jsc} \) where \( {s}_{jsc}=\frac{\# em{p}_{jsc}}{\sum_i\# em{p}_{isc}} \) is the share of employees of the largest 4 firms (j = 1, …, 4) in sector s in year c, while all firms i = 1, …, n constitute the sector s

Herfindahl–Hirschman index (HHI): sum of the squared employment shares of all firms operating in a given industrial sector s in year c, calculated as \( {HHI}_{sc}={\sum}_{i=1}^n{s}_{isc}^2 \) for any firm i = 1, …, n.

Turbulence: sum of the gross entry and gross exit rates according to the Dunne et al. (1988) definitions of entry and exit rates: \( {turb}_{sc}=\frac{n{e}_{sc}}{n_{sc}}+\frac{n{x}_{sc}}{n_{sc}} \), where nesc, nxsc, and nsc are respectively the total number of entrants, the total number of exits, and the overall number of firms in sector s in year c.

Group share: share of firms belonging to a group.

Share of unlimited liability companies: the proportion in the population of business structures without corporate (legal) personality (Business.gov.nl 2019), including both partnerships (general, professional, and limited) and sole proprietorships (or sole traders).Footnote 2 Sole proprietors and partnerships are unlimited liability companies, where, in most of the cases, the entrepreneurs are the unique shareholders and the company directors.

Community Innovation Surveys are valuable sources of context indicators related to innovation. By construction, they report information on representative samples of firms, which is then generalizable to the whole population. From the CISs we calculated the shares of innovative firms in different categories on the total number of firms in the CISs, per sector, as follows:

Innovators share: share of firms performing any kind of innovative activity. Innovations are defined in the most inclusive sense (technological or not, ongoing, completed or abandoned).

Young innovators share: share of innovative firms that are less than 10 years old.

Small innovators share: share of innovative firms with less than 50 employees.

Young and small innovators share: share of innovative firms that are less than 10 years old and have less than 50 employees.

Share of firms with new to the market products: share of innovative firms that introduced products new to the market.

Share of young firms with new to the market products: share of innovative firms that introduced products new to the market and are less than 10 years old.

Share of small firms with new to the market products: share of innovative firms that introduced products new to the market and have less than 50 employees.

Share of young and small firms with new to the market products: share of innovative firms that introduced products new to the market, are less than 10 years old and have less than 50 employees.

CISs are collected every two years. However, because their variables refer to two years before the sampling, we use the same variables for two consecutive years.

3.3 Method

The relationship we want to investigate can be represented by the following model (in the baseline formulation):

where εsc is the residual in sector s in year c. The model was estimated using standard panel data regression techniques, using the birth year as the time dimension. In particular, we employed within-regression (fixed effects) estimations, because with a regression analysis performed at the industry level, it is very likely that there are unobserved sector-specific time-unvarying factors, which influence the relationship of interest. Moreover, the variance-covariance matrix was estimated using the sandwich estimator developed by Huber (1967) and White (1980, 1982), obtaining robust standard errors.

4 Results

4.1 Descriptive statistics

The first three columns of Table 1 report the mean, median and standard deviation of our variables. It is interesting to notice that turbulence due to sum of entries and exits has a mean of 25.1% and a median of 22.6%. This shows that, generally, sectors are characterized by high churn, with a substantial share of firms being created ex-novo or closing down. As indicated by the large share of unlimited liability companies with a mean of 61.3%, businesses created without corporate (legal) personality (as sole proprietorship or partnership) are a consistent majority of the firms’ population. Innovation appears to be a pervasive phenomenon: on average, more than a company out of two performs some kind of innovative activity or has attempted to do so. While the share of young innovative firms and the share of small innovative firms are both slightly above 20%, this percentage falls to about 8% for innovative firms that are both young and small. A similar pattern is observed when considering innovations that are new to the market.

In Table 1, the correlation coefficients for turbulence indicate that industries with more intense dynamics of entry and exit are characterized by higher concentration (especially in terms of dominance of few leading firms) and lower presence of unlimited liabilities companies (in the form of partnership and sole proprietorship). This suggests that turbulence is associated with the presence of more structured and sizeable companies in an industry, as opposed to individually owned firms. Turbulence is also positively (although marginally) correlated with the share of firms that are part of a larger group. This confirms the previous observation that industries characterized by a larger presence of firms with the legal and ownership structure of corporations, as opposed to individual owners and partners, display more intense dynamics of entry and exit.

Focusing on the correlation between turbulence and innovation indicators, turbulence is positively correlated with both the share of young innovators and the share of young and small innovators, while it is not correlated in a statistically significant way with the share of innovators as a whole, and the share of small innovators. Conversely it is negatively correlated with the share of firms that introduced new-to-the-market products. These indicators seem to suggest that it is not the general level of innovativeness in a sector (or the general level of technological opportunity) that matters for the dynamics of entry and exit, but the extent to which innovation is driven by young firms. This pattern becomes more evident when considering radically new products. In fact, turbulence is negatively correlated to the share of all firms with new-to-the-market products and positively correlated to the share of young and small firms with new-to-the-market products. Hence, an entrepreneurial regime of innovation is characterized by more intense dynamics of entry and exit (Winter 1984). Finally, as expected, variables that reflect similar dimensions are highly correlated (e.g. C4 and Herfindahl index) and will be included only one at a time in the regression model.

4.2 The population dynamic of firm exits

Figure 1 shows the distribution of firms in the 2018 exit cohort by their birth cohort (from 1994 to 2018). The distribution of exiting firms is highly concentrated in the most recent birth cohorts. More than half of all exits involved infant firms, less than three years old. Specifically, exits were the highest for new firms in the second year after creation (i.e. one year old), with 23.3% of all exits in the 2017 birth cohort. Exits were somewhat lower in the first year after creation (less than 12 months old), with 14.6% of all exits in 2018 by firms born in the same year, and in the third year after creation (two years old), with 13.1% of all exits in 2018 by firms born in 2016. The proportion of exits is between 7% and 10% for the cohorts of firms born between 2013 and 2015 (from 3 to 5 years old), and then fall below 5% for older cohorts. In sum, the strong concentration of exits at 2018 among firms in the most recent birth cohorts suggests that the population of exits as a whole is characterized by a ‘revolving doors’ pattern of exit, with the majority of exits occurring for firms in their infancy, within the third year from birth. However, consistent with previous research (Bruderl and Schussler 1990), exit at birth (within 12 months from creation) is not the highest in the life of new firms, as the peak is observed in the second year of activity.

Birth-cohort distribution of exits at 2018

4.3 The dynamic of firm exits by industrial sector

Figure 2 reports the distribution of the 2018 exit cohort by birth cohort split by sector of activity, separating manufacturing from services firms. The peak of exit in the second year of activity is a few percentage points higher in services than in manufacturing new firms, 24.1% and 20.6% respectively. As well, exit at birth is relatively more frequent in services firms than in manufacturing (15.3% and 11.7% of firms exiting in 2018 in the respective sector were born within the same year). More specifically, after the common peak in the second year of activity, the most frequent class of exit is in the first year of activity for services firms, and in the third year for manufacturing firms. Overall, the ‘revolving door’ pattern is more pronounced in services than in manufacturing due to more intense churn in infant firms, especially within the first 24 months of life. The longer time to exit in manufacturing reflects the higher exit costs, because of the sunk costs and capital investments necessary at birth. In contrast, in services activities, more dependent on intangible and human resources, exit costs are lower and the time to exit shorter.

Birth-cohort distribution of exits at 2018 by industrial sector

4.4 The dynamic of firm exits by the business legal structure

Figure 3 compares the distribution of firms in the 2018 exit cohort by birth cohort between the two types of legal structure of business: with and without corporate (legal) personality. As mentioned in the data section, business structures without corporate personality include sole-proprietorships (or sole trades) and general, professional, and limited partnership. This is the legal structure generally chosen by self-employed individuals and freelancers when starting their own business (Business.gov.nl 2019). This business structure offers tax benefits especially at the early phase of setting up the business, but also imposes (unlimited) personal liabilities. The term “sole-proprietorship” refers to the legal structure, and not to the number of employees: a sole proprietor may hire employees, therefore not being a one-person business necessarily. Legal structures with corporate (legal) personality are autonomous entities, which are liable for any debts instead of the individual owners. As a director and shareholder, the entrepreneur is registered as an employee of the company. Theses legal structures include predominantly private limited companies but also public limited companies, cooperatives, associations, and foundations.

Birth-cohort distribution of exits at 2018 by business legal structure

Figure 3 shows very distinctive dynamics of exits between the two legal structures. In legal structures with corporate personality (Fig.3.a: Limited liability companies), the distribution of exits by birth cohort is especially concentrated in companies that are in their first or second year of activity from birth, representing 22.9% and 29.6% of the total exits respectively. In other words, more than half of the current exits (52%) occurs within the first 24 months of life of new companies. This percentage drops very rapidly with age and is down to about 12% of exits in the third year of activity (2016 cohort). In contrast, for sole proprietorships and partnerships (Fig.3.b: Unlimited liability companies) the distribution of exits is more even across birth cohorts. As of 2018, the proportion of exits in the sixth year of activity (2013 cohort) is almost equal to the proportion of exits at birth (2018 cohort), both representing about 10% of the total exits. As mentioned previously, the peak of exit is observed in the second year of activity and it is lower for sole proprietors and partnerships than for limited liability companies (18.6% versus 29.6%). Overall, the revolving door pattern is especially pronounced for the limited liability companies, with most of the churn taking place in the first two years of life of new businesses. Time to exit is short. In contrast, sole proprietors and partnerships stay in business for longer before exiting, with the time to exit extending up to six years in a relevant number of cases. Hence, individuals who are personally responsible for their own business, independently or as members of a partnership, await longer before making an exit decision, in comparison to corporate legal entities. This observation is consistent with the view that exit decisions reflect not only the economic performance of the business, but also subjective considerations by the individual entrepreneurs who gauge their opportunity costs in terms of available employment alternatives, as well as their emotional investment in the business (Gimeno et al. 1997). In businesses with a corporate structure, and less personal involvement and responsibility, exit decisions respond more quickly to performance according to a managerial logic.

4.5 The employment dynamics of exiting firms

Figure 4 traces back over time the average number of employees of firms in the 2018 exit cohort by birth cohort, going back to 1994 as the first birth cohort. It shows that, on average, the longer is the time to exit of new firms, the higher is the size at birth, the current size over time, and the size at exit. That is, older exiting firms were larger at birth, have grown more and exited with a greater number of employees, than those exiting young. Furthermore, the oldest birth cohorts, especially from 1995 to 1999, show a stronger “shadow of death” effect – where the exiting firms experience a steady decline in performance for several years before exit (Griliches and Regev 1995) – than the younger birth cohorts. Our results on the older cohorts support previous evidence confirming the “shadow of death effect” in terms of employment as, for example, in Troske (1996); Almus (2004); and Fackler et al. (2013). The younger birth cohorts do not show a “shadow of death” effect because they enter the market very small, they do not have the time to grow consistently and then they exit fairly small in terms of employees. It is worth noting, however, that even in the most resilient birth cohort, which reached the 25th years of activity before exiting, the maximum average size achieved during the lifecycle is seven employees. Thus, although firm size increases with the time to exit, exiting firms are persistently small, below 10 employees on average.

Average number of employees of exiting firms at 2018, by birth cohort: 1994–2018

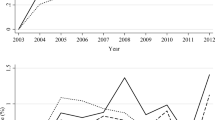

A similar, and more pronounced, pattern emerges when focusing on firms born from 2004 onwards and exiting at 2018. As shown in Fig. 5, the maximum firm size achieved over time by the most resilient cohort of new firms - those that exited at the 15th year of activity - is less than four employees on average.

Average number of employees of exiting firms at 2018 by birth cohort: 2004–2018

In order to establish whether some of the exiting firms may have achieved a more significant size at some point in time before exit, we consider the top percentile of the number of employees over time, for all birth cohorts since 2004. Figure 6 indicates that only 5% of all exiting firms reaches the size of 10 employees at some point in time. In other words, 95% of all exiting firms in 2018 born after 2004 are micro-firms with nine or fewer employees throughout their lifecycle.

Percentile (95th) of firm size of exiting firms at 2018 by birth cohort: 2004-2018

The combined picture of Figs. 5 and 6 suggests that there are three distinct classes of exiting firms within the 2018 exit cohort. In Fig. 5, the lines representing the average employment over time for each birth cohort appear to cluster around three groups. A first cluster (at the bottom of the graph) displays an average number of employees around one across the lifecycle of firms, for the most recent birth cohorts (from 2013 to 2018). As indicated in Fig. 6, within this group, 95% of firms remained below three employees throughout their lifecycle. We define this as the infancy class, of firms exiting within six years after founding. A second cluster (at the center of Fig. 5) is characterized by an average number of employees between one and two over the lifecycle of the exiting firms. This group includes firms from the 2006 to the 2012 birth cohort. Figure 6 shows that within this group the more recent cohorts (from 2009 to 2012) are more homogenous in the value of the employment at the 95th percentile, indicating that most firms in this group did not reach more than four employees over time. This is in contrast to the remaining group of relatively larger and older firms, able to sustain a firm size of five and more employees for some time before exiting. Hence, we define as the adolescence class those firms entering between 2009 and 2012, and exiting from the 7th to the 10th year of activity. Finally, the maturity class includes those firms entering between 2004 and 2008 and exiting from the 11th to 15th year after entry.

The 2006 birth cohort displays a somewhat mixed behavior: while in terms of age this cohort would fall in the mature category its employment trend is more similar to the adolescent category (Fig. 5). It must be noted however that the 2006 cohort would have been in its second year of activity in 2007, the onset of the financial crisis. As observed above, this year of activity has been the one with the highest incidence of exit. This combination may have intensified exit, shifting the pattern of exit from mature to adolescent.

In sum, the 2018 exit cohort is composed mainly of micro-firms with less than 10 employees. Specifically, infant exiting firms (less than 6 years of activity) remain mostly very small (below 3 employees) from birth to exit. These represent the majority of exits. Adolescent exiting firms (7 to 10 years of activity) have the possibility, for a small proportion of firms, to reach a more substantial size (around 4 employees) for a few years before they exit. Mature exiting firms (11 to 15 years of activity) display the potential, for a small proportion of firms, to maintain a relatively larger size (5 and more employees) over their lifecycle.

Moving the analysis to the type of industrial activity, Fig. 7 reports the 95th percentile of firm size of the 2018 exit cohort by birth cohort for services firms. The overall trend confirms what observed in the aggregate for the whole economy: that most of the firms exiting in 2018 and born after 2004 (i.e. less than 15 years old) do not reach a size above 10 employees throughout their live cycle. Only 5% did. In light of the exit patterns observed above, it emerges that although the services sector is characterized by a more evident “revolving door” pattern and shorter time to exit, the potential for growth of the most resilient exiting firms is comparable to the rest of the economy.

Percentile (95th) of firm size of exiting firms at 2018 by birth cohort, in the services sector

As for the legal structure of exiting firms, Fig. 8 shows the top percentile of firm size of the 2018 exit cohort by birth cohort for unlimited liability businesses. The 95th percentile of firm size for the sole proprietors and partnerships that exit in 2018 and were created after 2004 is at maximum equal to five employees. When comparing this to the overall 2018 exit cohort, as in Fig. 6, it results that while the exit cohort is composed for the largest part of micro-firms with less than 10 employees, only a small proportion of those with unlimited liability reaches more than five employees at any point in time. Hence, over a 15-year time period, cohorts of new limited liability companies with corporate (legal) personality achieve a more significant size before exiting, while new unlimited liability businesses (mainly sole proprietors and partnership) remain very small.

Percentile (95th) of firm size of exiting firms at 2018 by birth cohort, in unlimited liability companies

4.6 Multivariate analysis at the sectoral level per birth cohort

In this section, we present the results obtained with multivariate analysis at the sectoral level. Table 2 shows the coefficients of fixed effects regressions with robust standard errors. We present 6 models that differ for the choice of the indicator of industry concentration (the Herfindhal Index and the C4 index, respectively in Mod. 1 and 2) and of additional independent variables. In Mod.3 we add the share of young firms that introduce new-to-the-market products; in Mod. 4 the share of small firms that introduce new-to-the-market products; in Mod.5 the share of young and small firms that introduce new-to-the-market products; and, finally, in Mod.6 the share of young and small firms that introduce new-to-the-market products and the share of young and small firms innovating in the sector. We then present the results concerning the sub-samples obtained distinguishing between the different phases of the firm’s life: infancy (Mod.7), adolescence (Mod.8) and maturity (Mod.9). With respect to the pooled sample (Mod. 1–6), there is not a striking difference in the effect of the industry concentration indicator that we use. Both the Herfindahl and the C4 index affect negatively the sectoral exit rate in each cohort. The Herfindahl index has a lower statistical significance and a lower coefficient with respect to the C4 index; however, both of them show that a more concentrated sector at the date of founding has a negative effect on the exit rate of new firms observed in 2018. This result is consistent with the existence of entry barriers in more concentrated industries. If firms are able to overcome this initial obstacle and enter the sector, the factors that constitute the entry barriers make the entrants become established in the sector, being often stronger than other firms. This mechanism decreases the exit rate at the sector level.

The fact that the effect of C4 is stronger than HHI also suggests the possibility of a “shielding” effect. Here the main point to emphasize is not the concentration of the industry itself, but the existence of very large “industry leaders”. Newly created firms in an industry where large firms dominate the market may become strongly linked to them, either because they enter a wide network of economic relations (they are part of the supply chain lead by large established firms) or because standardized practices beneficial to all firms which apply them exist (like, for example, Siemens promoting best practices). Both mechanisms indicate that while there is a churning effect involving the fringe of the industry, a higher concentration makes the industry more “stable”, thus decreasing the exit rate.

The results concerning turbulence seem to confirm the hypothesis of the churning effect. Turbulence is the sum of entry and exit rates in the sector and captures, at least partially, the revolving-door-effect: the higher are the entry and exit rates at the time of the founding of a firm, the higher is the exit rate of the sector by cohorts. We can claim therefore that the turbulence variable is our best indicator for the churning effect.

Opposite effects are observed for the share of firms belonging to a group and for the share of unlimited liability companies (sole proprietorships and partnerships). While an increase of the share of firms in a group decreases the exit rate in 2018, the increase in the share of sole proprietorships and partnerships increases the exit rate. Groups seem to provide a more stable and solid background in terms not only of financial resources but also of management expertise: these factors decrease the exit rate. On the other hand, a large share of sole proprietorship and partnership in a sector increases the exit rate since such business structures are more vulnerable to financial constraints and to external shocks than limited liability companies with corporate (legal) personality. While the time to exit is shorter for limited liability companies compared to unlimited liability businesses (as noted earlier), their exit rate is lower as a whole. New limited liability companies exit less frequently but more rapidly that new ventures without a corporate legal personality.

The results concerning the importance of innovators in the sector are quite interesting and, in some way, seem to confirm the Schumpeterian hypothesis. In particular, the share of innovators in a sector and even more the share of the innovators that introduce new-to-the-market products increase the exit rate in that sector. This result assigns a disruptive role to innovations that force those firms that are not able to adapt and catch-up with the new technologies to exit the market.

While the share of innovators in the sector at the time of founding increases the exit rate of new firms, the share of small innovators active in the sector at the moment of founding decreases the exit rate in the sector (except in the model specification in which we add a variable indicating the share of small firms that introduced new-to-the-market products). This result suggests that the sector in which there is a larger share of small innovators is a high-intensity innovation sector in which both the large firms as well as new firms innovate. As we know from the literature (Cefis and Marsili 2006) the innovation premium in terms of survival is greater for small firms than for large firms. This could explain why a sector with a larger share of small innovators presents lower exit rates.

The additional variables inserted in Mod. 3 to Mod. 6 do not seem to change the overall results discussed above and do not improve the fit of the basic models (1 and 2).

We then focus on firms belonging to three distinct age classes, namely infancy, adolescence and maturity (as defined earlier in Section 4.5 describing the employment dynamics of exiting firms). With respect to the infancy class, we know from Fig. 1 that this class is the one that experienced the higher exit rate, supporting what the literature has already indicated (Agarwal and Audretsch 2001; Dunne et al. 1988; Evans 1987; Geroski et al. 2010; Mata and Portugal 1994). For this class of firms, the concentration or the turbulence of the sector in which they enter do not have any significant impact on their exit rates. The share of firms with unlimited liability increases significantly the probability of exit, but the factors that are relevant for the exit rate at the sector’s level are the variables regarding innovation. In particular, the share of innovators on the population of the sector and the share of innovators that have introduced new-to-the-market products increase significantly the exit rates. These results suggest that while industrial concentration and industrial dynamics at the date of entry do not affect the exit of infant firms, the intensity of the competition in terms of innovation does. Those infant firms that are not able to immediately catch-up with the new technologies are likely to exit in a very short time. Thus, new firms founded in a highly innovative and uncertain environment (i.e. with a large share of innovators in products that are new to the market) are exposed to high risk of infant exit.

For the adolescence class we note that the innovation variables lose all their importance, while only the variables that describe the composition of the sector in terms of legal forms (the share of firms with unlimited liability) and the share of those belonging to a group indicate factors that lower the exit rate. These results suggest that during adolescence the most important factor that helps survival is to be inserted in a network that shields firms from exit. In this class, the turbulence indicator is also very significant and positive: the revolving-door effect seems relevant in affecting survival. Those new firms that reach adolescence are those that are part of a larger corporate structure which provides them with resources that maintain them in activity.

With regard to the maturity class, innovation is important but with a different pattern with respect to the infant class. The total share of innovators has now a negative coefficient (marginally statistically significant). Furthermore, the variable that captures the innovations introduced by young innovators becomes statistically significant with a positive coefficient, thus increasing the exit rate. Hence, a Schumpeterian mechanism of creative-destruction seems at work: innovations introduced by young firms appear to threaten the survival of firms in their maturity phase. If a firm is not able to adapt and catch-up with the new technologies introduced by the innovative entrants, they are likely going to exit the market even if they are mature firms.

4.7 Sensitivity analysis

In the analysis of the sectoral patterns of exit across different age classes (Table 2) we grouped the birth cohorts of exiting firms in three intervals: 2004–2008 (maturity), 2009–2012 (adolescence) and 2013–2018 (infancy), as characterized in Section 4.5. In order to assess the sensitivity of our results to the choice of the intervals, we repeated the analysis for alternative choices of thresholds for the time intervals defining the three age classes of exiting firms, namely: 2004–2007 (maturity), 2008–2012 and 2009–2013 (adolescence), and 2014–2018 (infancy). As the new estimates show (Table 3), the changes in the time period do not alter the overall results that we observed before. The only small exception is for the adolescence class defined for 2008–2012 where the coefficient of innovation variable indicating the share of innovators that has introduced a new-to-the-market product becomes statistically significant at the 8.2% level with a negative sign. Overall, the sensitivity analysis confirms our results that environments of higher technological opportunity at entry increase the exit rates of infant firms but decreases those of mature firms. The sensitivity noted above seems to originate in the classification of the birth cohort of 2008, entered in the midst of the global financial crisis, whose exit pattern resembles more closely the maturity category of relatively larger entrants (as in the Table 2), rather than the adolescence category of smaller entrants (as in Table 3).

5 Conclusions

This paper has tested the relevance of two different patterns of firms exit: the revolving door and the gale of creative destruction. In the first, the liability of newness plays a major role in the exit process, while in the second the displacement of non-innovators is the driver of exit. We have tested these two patterns of exit on the population of Dutch firms that exited in 2018.

A general initial result in line with previous studies is that turbulence is high, and exit takes place across all industries. In addition, exit is higher and takes place earlier in services than in manufacturing. Sole proprietorship entrepreneurs have a distribution of exit more even across birth cohorts, indicating a greater involvement in the company and a higher opportunity cost of closing down the business.

When examining the two exit patterns identified in this paper, we find confirmation that they characterize different types of industries. In industries in which innovation does not play a major role, the revolving door is the typical pattern: here exit is concentrated among the adolescent firms. These firms are also small in size. On the contrary, in industries in which innovation plays a role, exit takes place both among infant as well as mature firms. Moreover, exiters are not necessarily only the smaller firms. While a highly innovative and uncertain environment can threaten the survival of infant firms, the exit of mature firms is driven by the innovation of young firms, in a typical gale of creative destruction.

Interesting and intriguing results emerge when industrial structure is introduced in the analysis. In fact, contrary to what one could expect, concentration negatively affects exit, pointing to the role of entry barriers that, while diminishing entry rates, diminish also the exit rates of those firms that actually are able to enter. Also, industry leaders in concentrated industries have a positive effect on the survival of the younger and smaller companies, because they generate standardization and network effects. Similarly, the increasing relevance of groups in an industry introduces more stability in industry structure, thus decreasing exit. On the contrary, a larger share of business ventures with unlimited liability and without corporate personality (sole proprietors and partnerships) in industries, indicating a more turbulent environment, increases exit.

This paper offers a novel approach to the study of firm exit patterns by looking retrospectively to the dynamic of an exit cohort, from the time of exit back to time of creation of the exiting firms. In order to account for the variety of exit patterns observed in an economy, we have focused on initial conditions at birth, defined by firm-specific structural characteristics, such as the legal structure of the business, and the technological and competitive environment in the industry at the time of entry. This is only a first step in the direction of examining the sources of variety between a “revolving door” pattern and a “gale of creative destruction” pattern. In fact, firm exit is a multi-layered process influenced not only by how resources match market selection and technological opportunities, but also by the strategic choices and personal motivations of the founders, which may affect timing and modes of exit (Bradley et al. 2011; DeTienne et al. 2015; Gimeno et al. 1997).

In future research it would be interesting to explore how exit strategies, innovation at entry, and founder experience, all factors influencing the likelihood of exit, can also contribute to explain the variety of exit patterns of new firms, from churning at the margin to the displacement of incumbents. Our approach allows also to assess the contribution of an exit cohort to employment generation (and destruction), with an impact on the dynamics of industrial structure. In the future it would be interesting to extend this approach to investigate how through knowledge transfer and spillover an exit cohort can add more broadly to experimentation and growth in the economy, beyond its immediate effect on industrial dynamics (Kerr et al. 2014; Knott and Posen 2005; Lindholm-Dahlstrand et al. 2018; Rosenberg 1992). Finally, our paper calls for a better and deeper understanding of the relationship between industrial concentration and exit. In fact, this paper has shown that entry barriers become exit barriers for those firms that are able to enter an industry and that for the survival of new firms there can be a difference between an industry with an oligopolistic structure of many large firms and one with few leaders. Future research should develop these findings much more in depth and move forward our understanding of industries by disentangling the diverse roles of different degrees and types of concentration on the stability of industrial structure and on the relationship between large firms and the survival and growth of new firms.

Notes

For simplicity from here on we refer to the exit rate by birth cohort only as exit rate.

In the Netherlands, business structures can be with or without corporate (legal) personality. The group of legal structures with corporate (legal) personality include: private limited liability companies, public limited liability companies, cooperatives, associations, and foundations (Business.gov.nl 2019).

References

Abernathy WJ, Utterback JM (1978) Patterns of industrial innovation Technology Review 80

Acs ZJ, Audretsch DB (1989) Small firms in U.S. manufacturing economics letters 31:399-402 https://doi.org/10.1016/0165-1765(89)90037-2

Acs ZJ, Audretsch DB (1990) Innovation and small firms. MIT Press, Cambridge

Agarwal R, Audretsch DB (2001) Does entry size matter? The impact of the life cycle and technology on firm survival. The Journal of Industrial Economics 49:21–43

Almudi I, Fatas-Villafranca F, Fernández-Márquez CM, Potts J, Vazquez FJ (2019) Absorptive capacity in a two-sector neo-Schumpeterian model: a new role for innovation policy ICC https://doi.org/10.1093/icc/dtz052

Almudi I, Fatas-Villafranca F, Izquierdo LR (2013) Industry dynamics, technological regimes and the role of demand JEE 23:1073-1098 https://doi.org/10.1007/s00191-013-0303-y

Almus M (2004) The Shadow of Death – An Empirical Analysis of the Pre-Exit Performance of New German Firms SBE 23:189–201 https://doi.org/10.1023/b:sbej.0000032033.00519.00

Amit R, Muller E, Cockburn I (1995) Opportunity costs and entrepreneurial activity JBS 10:95–106

Audretsch DB (1995) The propensity to exit and innovation RIO 10:589-605 https://doi.org/10.1007/bf01026884

Balcaen S, Manigart S, Buyze J, Ooghe H (2011) Firm exit after distress: differentiating between bankruptcy, voluntary liquidation and M&a SBE 39:949-975 https://doi.org/10.1007/s11187-011-9342-7

Baptista R, Karaöz M (2009) Turbulence in growing and declining industries SBE 36:249–270 https://doi.org/10.1007/s11187-009-9226-2

Bartelsman E, Scarpetta S, Schivardi F (2005) Comparative analysis of firm demographics and survival: evidence from micro-level sources in OECD countries ICC 14:365–391 https://doi.org/10.1093/icc/dth057

Bradley SW, Aldrich H, Shepherd DA, Wiklund J (2011) Resources, environmental change, and survival: asymmetric paths of young independent and subsidiary organizations SMJ 32:486-509 https://doi.org/10.1002/smj.887

Breschi S, Malerba F, Orsenigo L (2000) Technological regimes and Schumpeterian patterns of innovation EJ 110:388–410

Bruderl J, Schussler R (1990) Organizational mortality: The liabilities of newness and adolescence. Administrative Science Quarterly 35:530–547

Buehler S, Kaiser C, Jaeger F (2006) Merge or fail? The determinants of mergers and bankruptcies in Switzerland, 1995–2000. Econ Lett 90:88–95. https://doi.org/10.1016/j.econlet.2005.07.010

Business.gov.nl (2019) Webpage of Government information for entrepreneurs: https://business.gov.nl/starting-your-business/choosing-a-business-structure/business-structures-in-the-netherlands-overview/. Accessed 15 October 2019

Caves RE (1998) Industrial organization and new findings on the turnover and mobility of firms JEL 36:1947-1982

Cefis E, Marsili O (2006) Survivor: The role of innovation in firm's survival RP 35:626–641

Cefis E, Marsili O (2011) Born to flip. Exit decisions of entrepreneurial firms in high-tech and low-tech industries JEE 21:473–498 https://doi.org/10.1007/s00191-010-0210-4

Cefis E, Marsili O (2012) Going, going, gone. Exit forms and the innovative capabilities of firms RP 41:795–807

Christensen MC (1997) The Innovator's dilemma. Harvard Business School Press,

Colombelli A, Krafft J, Vivarelli M (2016) To be born is not enough: the key role of innovative start-ups SBE 47:277–291 https://doi.org/10.1007/s11187-016-9716-y

DeTienne DR, McKelvie A, Chandler GN (2015) Making sense of entrepreneurial exit strategies: A typology and test JBS 30:255–272 https://doi.org/10.1016/j.jbusvent.2014.07.007

Dosi G, Marsili O, Orsenigo L, Salvatore R (1995) Learning, market selection and the evolution of industrial structures SBE 7:411-436

Dosi G, Nelson RR, Winter SG (2000) The nature and dynamics of organizational capabilities. Oxford university press,

Dosi G, Pereira MC, Virgillito ME (2017) The footprint of evolutionary processes of learning and selection upon the statistical properties of industrial dynamics ICC 26:187–210 https://doi.org/10.1093/icc/dtw044

Dunne T, Roberts MJ, Samuelson L (1988) Patterns of firm entry and exit in the U.S. manufacturing industries RAND journal of economics 19:495-515

Ericson R, Pakes A (1995) Markov-perfect industry dynamics: A framework for empirical work Review of Economic Studies 62:53–82

Erwin GR, McConnell JJ (1997) To live or let die? An empirical analysis of piecemeal voluntary corporate liquidations. J Corp Financ 3:325–354. https://doi.org/10.1016/s0929-1199(97)00003-5

Evans DS (1987) The relationship between firm growth, size, and age: estimates for 100 manufacturing industries. J Ind Econ 35:567–581

Fackler D, Schnabel C, Wagner J (2013) Lingering illness or sudden death? Pre-exit employment developments in German establishments ICC 23:1121–1140 https://doi.org/10.1093/icc/dtt041

Fontana R, Nesta L (2009) Product Innovation and Survival in a High-Tech Industry RIO 34:287–306 https://doi.org/10.1007/s11151-009-9210-7

Geroski PA (1995) What do we know about entry? Int J Ind Organ 13:421–440

Geroski PA, Mata J, Portugal P (2010) Founding conditions and the survival of new firms SMJ 31:510–529 https://doi.org/10.1002/smj.823

Gimeno J, Folta TB, Cooper AC, Woo CY (1997) Survival of the fittest? Entrepreneurial Human Capital and the Persistence of Underperforming Firms Administrative Science Quarterly 42:750–783

Gort M, Klepper S (1982) Time paths in the diffusion of product innovations. The Economic Journal 92:630–653

Griliches Z, Regev H (1995) Firm productivity in Israeli industry 1979–1988. J Econ 65:175–203. https://doi.org/10.1016/0304-4076(94)01601-u

Henderson RM, Clark KB (1990) Architectural Innovation: The Reconfiguration of Existing Product Technologies and the Failure of Established Firms Administrative Science Quarterly 35:9 https://doi.org/10.2307/2393549

Hessels J, Grilo I, Thurik R, Zwan, Pvd (2010) Entrepreneurial exit and entrepreneurial engagement JEE 21:447–471 https://doi.org/10.1007/s00191-010-0190-4

Huber PJ The behavior of maximum likelihood estimates under nonstandard conditions. In, 1967 1967. University of California Press, pp 221–233

Hyytinen A, Pajarinen M, Rouvinen P (2015) Does innovativeness reduce startup survival rates? JBS 30:564–581. https://doi.org/10.1016/j.jbusvent.2014.10.001

Jovanovic B (1982) Selection and the evolution of industry. Econometrica 50:649–670

Jovanovic B, MacDonald GM (1994) The life cycle of a competitive industry JPE 102:322–347

Kerr WR, Nanda R, Rhodes-Kropf M (2014) Entrepreneurship as Experimentation JEP 28:25–48 https://doi.org/10.1257/jep.28.3.25

Klepper S (1996) Entry, exit, growth, and innovation over the product life cycle. Am Econ Rev 86:562–583

Klepper S (1997) Industry life cycle ICC 6:145-181

Knott AM, Posen HE (2005) Is failure good? SMJ 26:617–641

Leonard-Barton D (1992) Core capabilities and core rigidities: a paradox in managing new product development SMJ 13:111-125. https://doi.org/10.1002/smj.4250131009

Lieberman MB (1990) Exit from declining industries: "shakeout" or "stakeout"? RAND J Econ 21:538. https://doi.org/10.2307/2555467

Lindholm-Dahlstrand Å, Andersson M, Carlsson B (2018) Entrepreneurial experimentation: a key function in systems of innovation SBE 53:591–610 https://doi.org/10.1007/s11187-018-0072-y

Malerba F, Orsenigo L (1995) Schumpeterian Patterns of Innovation CJE 19:47–65

Malerba F, Orsenigo L, Nelson RR, Winter SG (2016) Innovation and industrial evolution. Innovation and the evolution of industries: history-friendly models. Cambridge University press, Cambridge. https://doi.org/10.1017/CBO9781107280120.004

Manjón-Antolín MC (2010) Firm size and short-term dynamics in aggregate entry and exit. International journal of industrial organization 28:464–476. https://doi.org/10.1016/j.ijindorg.2009.11.002

Marshall A (1920) Principles of economics, 8th edn. Mcmillan, London

Mata J, Portugal P (1994) Life duration of new firms. The Journal of Industrial Economics 42:227–245

Nelson RR, Winter SG (1982) An evolutionary theory of economic change. Belknap Press of Harvard University Press, Cambridge, MA

Nightingale P, Coad A (2014) Muppets and gazelles: political and methodological biases in entrepreneurship research ICC 23:113–143 https://doi.org/10.1093/icc/dtt057

Ortiz-Villajos JM, Sotoca S (2018) Innovation and business survival: A long-term approach RP 47:1418–1436 https://doi.org/10.1016/j.respol.2018.04.019

Rosenberg N (1992) Economic Experiments ICC 1:181–203 https://doi.org/10.1093/icc/1.1.181

Schary MA (1991) The probability of exit. RAND J Econ 22:339–353

Schumpeter JA (1934) The theory of economic development: an inquiry into profits, capital, credit, interest, and the business cycle (English edition, German original 1911). Harvard Economic Studies, Cambridge

Schumpeter JA (1942) Capitalism, socialism and democracy. Harper & Row, New York

Shane S, Venkataraman S (2000) The promise of entrepreneurship as a field of research. Academy of management review 25:217–226

Troske KR (1996) The dynamic adjustment process of firm entry and exit in manufacturing and finance, Insurance, and Real Estate. J Law Econ 39:705–735. https://doi.org/10.1086/467363

Tushman M, Anderson P (1986) Technological discontinuities and organisational environments. Administrative science quarterly 31:439–465

Wennberg K, DeTienne DR (2014) What do we really mean when we talk about ‘exit’? A critical review of research on entrepreneurial exit. Int Small Bus J Res Entrepreneurship 32:4–16. https://doi.org/10.1177/0266242613517126

White H (1980) A heteroskedasticity-consistent covariance matrix estimator and a direct test for heteroskedasticity Econometrica: journal of the Econometric Society:817–838

White H (1982) Maximum likelihood estimation of misspecified models Econometrica: Journal of the Econometric Society:1–25

Winter SG (1984) Schumpeterian competition in alternative technological regimes. Journal of Economic Behavior & Organization 5:287–320

Winter SG, Kaniovski YM, Dosi G (2000) Modeling industrial dynamics with innovative entrants SCED 11:255–293. https://doi.org/10.1016/s0954-349x(99)00010-7

Acknowledgments

The authors thank Alessandro Lucini-Paioni for precious research assistance, and the participants at the International ICC Conference: Beyond Technological Innovation and Diffusion. University of Berkeley, Berkeley, CA, U.S.A., December 11-14, 2016; and at the Workshop in honor of Luigi Orsenigo on December 5-6, 2018, at ICRIOS, Bocconi University, Milan, Italy, for fruitful discussions. The empirical part of this research was carried out at Microdata – Centraal Bureau voor Statistiek (CBS), the Netherlands. The views expressed in this paper are those of the authors and do not necessarily reflect the policies of Statistics Netherlands. Elena Cefis acknowledges financial support from the University of Bergamo (grants n. 60CEFI18 and n. 60CEFI19, Dept. of Management, Economics, and Quantitative Methods).

Funding

Open access funding provided by Università degli Studi di Bergamo within the CRUI-CARE Agreement.

Author information

Authors and Affiliations

Corresponding author

Ethics declarations

Conflict of interest

Elena Cefis has received research grants from the University of Bergamo, Dept. of Management, Economics, and Quantitative Methods, Bergamo, Italy: grants n. 60CEFI18 and n. 60CEFI19.

The authors declare that they have no conflict of interest.

Additional information

Publisher’s note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Luigi Orsenigo is deceased

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons licence, and indicate if changes were made. The images or other third party material in this article are included in the article's Creative Commons licence, unless indicated otherwise in a credit line to the material. If material is not included in the article's Creative Commons licence and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this licence, visit http://creativecommons.org/licenses/by/4.0/.

About this article

Cite this article

Cefis, E., Malerba, F., Marsili, O. et al. Time to exit: “revolving door effect” or “Schumpeterian gale of creative destruction”?. J Evol Econ 31, 1465–1494 (2021). https://doi.org/10.1007/s00191-020-00701-8

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s00191-020-00701-8