Abstract

This paper examines how vertical integration affects non-price efficiency in the movie theater industry. Adopting a discrete choice framework, we derive consumer welfare under capacity constraints and fixed prices, and show that allocating capacity proportionally to demand is efficient. Applying our approach to estimating the efficiency of movie theaters’ seat allocations, we show that integrated theaters may be more efficient than non-integrated ones at picking movies to screen and allocating seats across them. We propose a theoretical mechanism behind these results. Specifically, we show that integrated theaters have higher incentives to acquire demand information and hence can be more efficient in allocating the seats.

Similar content being viewed by others

Notes

Gibbons (2005) provides an excellent literature review on the four formalizable theories of vertical integration.

“Conglomerates direct Korea’s film industry”, Korea Joongang Daily, Dec 06, 2012.

Henceforth, we say the capacity allocation is more efficient if it generates higher consumer welfare.

Under the assumption, we may overestimate the welfare loss under the capacity constraint.

The proof is given in the Appendix.

The revenue sharing ratio is 50:50 for domestic movies and 40:60 for foreign movies in Seoul, the largest city in South Korea. It is 50:50 for all movies in other regions in Korea.

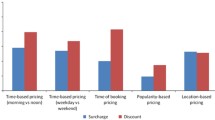

Orbach and Einav (2007) provide in-depth analysis of the uniform pricing in the movie theater industry. They point out explanations based on perceived fairness, demand uncertainty, and monitoring costs. Courty and Nasiry (2018) show that price uniformity commonly observed in media and entertainment markets might be attributed to consumer loss aversion and uncertain taste for quality.

From now on, we use “city” (“province”) and “market” interchangeably.

Korea Box Office Information System is accessible at http://kobis.or.kr.

Korean Film Council is accessible at http://www.kofic.or.kr.

During 2007, for instance, the average daily audience size in Korea was 300 thousand on weekdays and 570 thousand on weekends.

Another explanation for this difference would be the difference in the sample. For example, in his analysis Einav (2007) included only those movies that reached a wide release at some point during their run; the average peak number of screens is 100 for movies that are excluded from his analysis. In contrast, we include almost all movies released in Korea during the sample period with only few exceptions. Since the market expansion effect of movies played in just few screens are likely to be very small, inclusion of such movies may lead to a larger value of \(\sigma \). Table 8 in the appendix presents 2SLS estimates of the demand model, using only observations where the market share is larger than 0.01% in column (1), 0.05% in column (2), and 0.1% in column (3), respectively. Consistent with our conjecture, the estimated value of \(\sigma \) decreases as we drop movies with small market shares.

Predicted movie demand in a given week is the sum of estimated market shares of all movies in that week, averaged over 5 years.

To further alleviate the endogeneity concern, for these 32 theaters we calculate the average efficiency one week before the organizational form change. Also, we calculate the average efficiency at the 10th week of 2007 (the average calendar time for vertical integration) for other non-integrated theaters, and similarly, the average efficiency at the 36th week of 2007 (the average calendar time for disintegration) for other integrated theaters. Table 4 shows that the average efficiency of theaters that became integrated (0.37) is higher than that of theaters that remained non-integrated (0.3). However, this does not necessarily imply that more productive theaters were chosen to be vertically integrated, as the former also have more screens (7.6) than the latter (6.9). Similarly, both efficiency and the number of screens are higher for theaters that became disintegrated than theaters that remained integrated.

For around 1,300 movies in the data, we obtain each movie’s genre from the movie section of Naver, the largest online platform in Korea (https://movie.naver.com/).

All proofs are relegated to the appendix.

References

Berry ST (1994) Estimating discrete-choice models of product differention. RAND J Econ 25(2):242–262

Bjornerstedt J, Verboven F (2016) Does merger simulation work? Evidence from the Swedish analgesics market. Am Econ J Appl Econ 8(3):125–64

Brenkers R, Verboven F (2006) Liberalizing a distribution system: the European car market. J Eur Econ Assoc 4(1):216–251

Bruno HA, Vilcassim NJ (2008) Structural demand estimation with varying product availability. Marketi Sci 27(6):1126–1131

Cardell SN (1997) Variance components structures for the extreme-value and logistic distributions with application to models of heterogeneity. Econ Theory 13(2):185–213

Chipty T (2001) Vertical integration, market foreclosure, and consumer welfare in the cable television industry. Am Econ Rev 13(1):99–107

Choi J, Choi YJ, Kim M (2015) Vertical foreclosure in the movie industry. Working Paper

Conlon CT, Mortimer JH (2013) Demand estimation under incomplete product availability. Am Econ J Microecon 5(4):1–30

Courty P, Nasiry J (2018) Loss aversion and the uniform pricing puzzle for media and entertainment products. Econ Theory 66(1):105–140

Einav L (2007) Seasonality in the U.S. motion picture industry. RAND J Econ 38(1):127–145

Forbes SJ, Lederman M (2010) Does vertical integration affect firm performance? Evidence from the airline industry. RAND J Econ 41(4):765–790

Fu WW (2009) Screen survival of movies at competitive theaters: vertical and horizontal integration in a spatially differentiated market. J Media Econ 22(2):59–80

Gibbons R (2005) Four formal (izable) theories of the firm? J Econ Behav Organ 58(2):200–245

Gil R (2007) Make-or-buy in movies: integration and ex-post renegotiation. Int J Ind Organ 25(4):643–655

Gil R (2009) Revenue sharing distortions and vertical integration in the movie industry. J Law Econ Organ 25(2):579–610

Gil R (2015) Does vertical integration decrease prices? Evidence from the paramount antitrust case of 1948. Am Econ J Econ Policy 7(2):162–91

Grossman SJ, Hart OD (1986) The costs and benefits of ownership: a theory of vertical and lateral integration. J Polit Econ 94(4):691–719

Hastings JS, Gilbert RJ (2005) Market power, vertical integration and the wholesale price of gasoline. J Ind Econ 53(4):469–492

Hausman J (1996) Valuation of new goods under perfect and imperfect competition. In: The economics of new goods, pp 207–248. National Bureau of Economic Research, Inc

Hortaçsu A, Syverson C (2007) Cementing relationships: vertical integration, foreclosure, productivity, and prices. J Polit Econ 115(2):250–301

Hwang Y (2013) Vertical integration and market foreclosure in the Korean movie industry. Ph.D. thesis, University of Southern California

Lee RS (2013) Vertical integration and exclusivity in platform and two-sided markets. Am Econ Rev 103(7):2960–3000

Leung TC, Qi S, Yuan J (2019) Movie industry demand and theater availability. Rev Ind Organ 25:1–25

Lewis JB, Linzer DA (2005) Estimating regression models in which the dependent variable is based on estimates. Polit Anal 13(4):345–364

McFadden D (1978) Modelling the choice of residential location. In: Karlqvist FSA, Weibull J (eds) Spatial interaction theory and planning models, pp 75–96. North Holland

Nevo A (2001) Measuring market power in the ready-to-eat cereal industry. Econometrica 69(2):307–342

Orbach BY, Einav L (2007) Uniform prices for differentiated goods: the case of the movie-theater industry. Int Rev Law Econ 27(2):129–153

Persico N (2000) Information acquisition in auctions. Econometrica 68(1):135–148

Rey P, Tirole J (2007) Chapter 33 a primer on foreclosure, vol 3 of handbook of industrial organization. Elsevier, London, pp 2145–2220

Small KA, Rosen HS (1981) Applied welfare economics with discrete choice models. Econometrica 49(1):105–130

Spengler JJ (1950) Vertical integration and antitrust policy. J Polit Econ 58(4):347–352

Suzuki A (2009) Market foreclosure and vertical merger: a case study of the vertical merger between turner broadcasting and time warner. Int J Ind Organ 27(4):532–543

Verboven F (1996) International price discrimination in the European car market. RAND J Econ 27:240–268

Williamson OE (1971) The vertical integration of production: market failure considerations. Am Econ Rev 61(2):112–123

Author information

Authors and Affiliations

Corresponding author

Ethics declarations

Conflict of interest

The authors declare that they have no conflict of interest.

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

We thank Michael Baye, Ricard Gil, Ken Hendricks, Joep Konings, Alan Sorensen, Frank Verboven, Andriy Zapechelnyuk, anonymous referees and associate editor for excellent comments and suggestions that helped to improve this article. We are also grateful to seminar participants at the University of Wisconsin-Madison, Nazarbayev University, CORE@50 Conference in Louvain-la-Neuve, and the 43rd EARIE Annual Conference in Lisbon. Financial support from the Seed Program for Korean Studies through the Ministry of Education of the Republic of Korea (AKS-2018-INC-2230011) and the Small Grant Program at Nazarbayev University (SHSS2018004) is gratefully acknowledged.

Appendix

Appendix

Proof of Proposition 1

We solve

subject to

If \(\sum q_{j}\le C\), then \(s_{j}^{*}=\frac{q_{j}}{\sum _{j\ne 0}q_{j}}C\) for each j is optimal. Suppose \(\sum q_{j}>C\). Clearly, the inequality binds. Then the first-order conditions are:

where \(\lambda _j\) for each j and \(\mu \) are the corresponding Lagrange multipliers. Differentiating (16) with respect to \(s_{j}\) yields \(z'_{j}(s_{j})=-\frac{1}{g_{j}(z_{j}(s_{j}))q_{j}}\) for each j. Combining it with (15) for each j and k we get \(z_{j}(s_{j})-\varepsilon _{0}(z_{j}(s_{j}))=z_{k}(s_{k})-\varepsilon _{0}(z_{k}(s_{k})),\) which holds if

When each \(\varepsilon _{ij}\) is i.i.d. extreme value, one can show that for each j we have

where \(A=1+\sum _{i\ne 0}\exp \alpha _{i}.\) From (16), (18), and (19) for each j and k we get \(s_{j}q_{k}=s_{k}q_{j},\) and hence for each j we have \(s_{j}=\frac{q_{j}}{\sum _{j\ne 0}q_{j}}C.\) \(\square \)

Proof of Proposition 1

(Proof of Proposition 2) The theater solves

subject to

Clearly, the second order condition holds. From the first-order condition (13) using (11) we get

If \(\delta _{j}=\delta _{i}=\lambda \), then \(s_{j}=\frac{{\hat{q}}_{j}}{{\hat{q}}_{j}+{\hat{q}}_{i}}C\) for \(j=1,2\). If \(\delta _{j}=1\) and \(\delta _{i}=\lambda \), then the result follows from LHS being decreasing and RHS increasing in \(s_{1}\). \(\square \)

Before we provide the proof of Proposition 2 we need to introduce the following definition and lemma that can also be found in Persico (2000).

Definition 1

A function H(v) is quasi-monotone if \(v'>v\) and \(H(v)>0\) imply \(H(v')\ge 0\).

Lemma 1

Let (c, d) be an interval of the real line, \(J(\cdot )\) a nondecreasing function, \(H(\cdot )\) a quasi-monotone function. Assume that for some measure \(\mu \) on \({\mathbb {R}}\) we have \(\int _{c}^{d}H(v)d\mu (v)=0.\) Then \(\int _{c}^{d}H(v)J(v)d\mu \ge 0\).

Proof of Proposition 3

We shall show that the marginal value of information is higher for integrated theaters. Denote the type of a theater, independent or integrated, by subscript \(\tau \in \left\{ Ind,Int\right\} \). For each \(\tau \) let \(s_{\tau }^{\eta ,{\hat{q}}_{1},{\hat{q}}_{2}}\) be the optimal allocation for movie 1, and \(\pi ^{\tau }(s_{\tau }^{\eta ,{\hat{q}}_{1},{\hat{q}}_{2}},q_{1},q_{2})\) the maximal profit given accuracy \(\eta \), signals \({\hat{q}}_{1}\) and \({\hat{q}}_{2}\), and movie demands \(q_{1}\) and \(q_{2}\). Define

We want to show that

Note that from (10) it follows that \(T_{\eta ,\theta ,q}({\hat{Q}}_{j}^{\eta }|q_{j})\) is distributed as \({\hat{Q}}_{j}^{\theta }\) . Hence applying the change of variable in (21) we have

We now show that the inner double integral above is nonnegative. Evaluating it we get:

For each \(\tau \) we have \(\left. \frac{\partial s_{\tau }^{\theta ,{\hat{q}}_{1},{\hat{q}}_{2}}}{\partial \theta }\right| _{\theta =\eta }\) is independent of \(q_{1}\) and \(q_{2}\), and

by the first-order condition. So, we can rewrite (22) as

Rearranging we get

Integrating out \(q_{2}\) in the first term and \(q_{1}\) in the second term we have

Now we use the Lemma to show that the two terms above are nonnegative. First, note that

is increasing in \(q_{j}\) because \(T_{\eta ,\theta ,q_{j}}({\hat{q}}_{j})\) is increasing by assumption. By the first-order conditions

for each j. So, to apply the Lemma it remains to show that

is quasi-monotone in \(q_{1}\), and

is quasi-monotone in \(q_{2}\). Using the definition of payoff rewrite (24) as:

Integrating the above we get

From Proposition 1 we know that \(s_{Int}^{\eta ,{\hat{q}}_{1},{\hat{q}}_{2}}>s_{Ind}^{\eta ,{\hat{q}}_{1},{\hat{q}}_{2}}\). Hence if

then (24) is negative for \(q_{1}\le s_{Int}^{\eta ,{\hat{q}}_{1},{\hat{q}}_{2}}\), and positive for \(q_{1}>s_{Int}^{\eta ,{\hat{q}}_{1},{\hat{q}}_{2}}\), and hence is quasi-monotone in \(q_{1}\). So, it remains to show (26). Because \(s_{Int}^{\eta ,{\hat{q}}_{1},{\hat{q}}_{2}}>s_{Ind}^{\eta ,{\hat{q}}_{1},{\hat{q}}_{2}}\), we get

Therefore it is sufficient to prove that \(\frac{\partial s_{Ind}^{\eta ,{\hat{q}}_{1},{\hat{q}}_{2}}}{\partial {\hat{q}}_{1}}<\frac{\partial s_{Int}^{\eta ,{\hat{q}}_{1},{\hat{q}}_{2}}}{\partial {\hat{q}}_{1}}.\) Implicitly differentiating the first-order conditions and using (11) we obtain

and

where \(z_{1}^{\tau }=\frac{s_{\tau }^{\eta ,{\hat{q}}_{1},{\hat{q}}_{2}}-{\hat{q}}_{1}}{{\hat{q}}_{1}}\) and \(z_{2}^{\tau }=\frac{C-s_{\tau }^{\eta ,{\hat{q}}_{1},{\hat{q}}_{2}}-{\hat{q}}_{1}}{{\hat{q}}_{1}}\), and \(h^{\eta }(x)=\frac{g^{\eta }(x)}{1-G^{\eta }(x)}\) is the hazard function of \(G^{\eta }(x)\). Finally, we get

where the inequality is due to \(s_{Int}^{\eta ,{\hat{q}}_{1},{\hat{q}}_{2}}>s_{Ind}^{\eta ,{\hat{q}}_{1},{\hat{q}}_{2}}\) by Proposition 1, \(z_{2}^{Ind}=z_{1}^{Ind}\) and \(z_{2}^{Int}<z_{1}^{Int}\) from the first-order condition, and \(h^{\eta }(\cdot )\) is increasing by log-concavity of \(g^{\eta }(x)\). Therefore (26) holds, and (23) is quasi-monotone. The proof that (25) is quasi-monotone in \(q_{2}\) follows the similar steps using the fact that \(\frac{s_{\tau }^{\eta ,{\hat{q}}_{1},{\hat{q}}_{2}}}{{\hat{q}}_{2}}<0\). Hence, the marginal value of information is higher for integrated theaters and the standard comparative statics argument yields the result. \(\square \)

1.1 Vertical integration and foreclosure

In this subsection, we quantify the foreclosure effect of vertical integration. First, we examine the prediction that non-integrated theaters do not discriminate movies based on the type of a distributor. Using the data on the seat allocation of non-integrated theaters we estimate the following model:

where \(Seat\,Share_{jhmt}^{Ind}\) is movie j’s share of seats in non-integrated theater h operating in market m during weekends of week t. The variable of interest is dummy \(Integrated_{j}\) equal to one if movie j is released by an integrated distributor and zero otherwise. We control for the relative movie demand by including \(Demand\,Share_{jmt}\) which is movie j’s share in the total audience of all movies in market m during weekdays of week t. The higher the relative movie demand, the higher should be this movie’s seat share. Week and theater fixed effects, \(\psi _t\) and \(\psi _h\), are also included in the model.

Next, we investigate whether integrated theaters foreclose movies of rival distributors. Using the data on the seat allocation of integrated theaters we estimate

The model is similar to (27) except that dummy \(Integrated_{j}\) is replaced with \(Own_{jh}\) which is equal to one if movie j is released by the distributor affiliated with theater h and zero otherwise. Coefficient \(\beta _{Own}\) measures the foreclosure effect of vertical integration.

The first two columns of Table 6 present estimates of model (27). As expected, there is no strong evidence that the seat share of independent movies is different from the seat share of movies of integrated distributors. Also, consistent with our prediction we observe a significant foreclosure effect in the last two columns of the table: the seat share is higher by 18% in an integrated theater for its own movies compared to other movies, controlling for the relative demand.

1.2 Additional Tables and Figures

See Tables 7 and 8; Figs. 4, 5 and 6.

Demand model fit. Notes: Each panel of the figure shows the observed and predicted movie demand on weekdays and weekends separately in each of the eight markets in the data. Predicted movie demand in a given week is the sum of estimated market shares of all movies in that week, averaged over the 5 years

Demand model fit at the movie-level. Notes: Each panel of the figure presents a scatter plot for each region where the weekend within-industry share determines the position on the vertical axis and the predicted within-industry share determines the position on the horizontal axis

Change in welfare loss after the organizational form change. The two panels of the figure show estimated welfare loss relative to 1 month prior to vertical integration or disintegration along with 95% confidence bands

Rights and permissions

About this article

Cite this article

Kim, I.K., Nora, V. Does vertical integration enhance non-price efficiency? Evidence from the movie theater industry. Rev Econ Design 24, 143–170 (2020). https://doi.org/10.1007/s10058-020-00234-3

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s10058-020-00234-3