Understanding Factors Affecting Innovation Resistance of Mobile Payments in Taiwan: An Integrative Perspective

1

Department of Marketing and Logistic Management, National Penghu University of Science and Technology, Magong 88046, Taiwan

2

Undergraduate Program of Financial Management College, CTBC Business School, Tainan 70963, Taiwan

*

Author to whom correspondence should be addressed.

Mathematics 2020, 8(10), 1841; https://doi.org/10.3390/math8101841

Submission received: 27 August 2020

/

Revised: 15 October 2020

/

Accepted: 16 October 2020

/

Published: 19 October 2020

(This article belongs to the Special Issue Mathematical Analysis in Economics and Management)

Abstract

:Mobile payment is a new payment method that provides opportunities for the financial services industry and involves various payment mediums. There are numerous drivers and barriers that influence customers’ willingness to use mobile payment. Previous studies have focused upon the motivations which facilitate its usage, but this study takes the opposite viewpoint and seeks to understand and classify the resistance to mobile payment from the customer perspective. Structural equation modeling (SEM) was used to analyze the data. More specifically, due to the small sample size, the study employed the Partial Least Squares (PLS) technique. A total of 348 valid samples were collected. Self-determination is an antecedent of innovation resistance theory and further affects the intention to use the mobile payment approach. The conclusion is that resistance to new products will reduce as consumers’ psychological needs are fulfilled. Several theoretical and practical implications are discussed for the mobile payment resistance.

1. Introduction

According to eMarketer [1], about 75% of the Taiwanese population have a smart phone, and amongst these, according to the Taiwan Network Information Center [2], more than 85% surf the internet using their devices. Various services are provided through apps on the smart phone, including real-time communications (What’s app, Line), online news (BBC news, Yahoo news), music streaming, media services (YouTube, Spotify), and email (Gmail, Outlook Mail), whilst the innovative mobile payment service has attracted consumer attention and achieved remarkable growth. The rapid development of m-commerce (mobile commerce) and mobile payment services has had a significant influence on economic and business models which receive a great deal of attention from academia and industry [3].

M-commerce allows customers to conduct business or make transactions without the restrictions of time and space [4]. This unique feature provides convenience and flexibility for customers, which makes mobile payment both popular and trendy. In the past, transactions made by cash have involved a number of risks, including the potential for greater spending, the chance that cash may be stolen, and the possibility that currency might carry pathogens [5]. Credit cards were issued as a medium for payment to solve the problems inherent in the use of cash, and in 2000, with the development of the internet and smart phones, mobile payments were introduced.

Mobile payments are defined as payments made through mobile devices and the internet [6,7]. Several sectors are involved in the mobile payment process, including banking and retailing industries, and the government. The banking industry plays an important role because it provides the system, monetary flow, and technological support. The retailing industry, on the other hand, must be willing to install the necessary mobile payment infrastructure to allow customers to use different payment tools. Regulations and laws governing mobile payment are made by government. Customers, venders, and banks may be exposed to risk if the laws managing mobile payment are not well regulated. Last but not least, the most important determinant of the success or failure of mobile payment is customers’ willingness to adopt and accept the system [8].

IDC (International Data News) estimates that mobile payments accounted for approximately 27.2% of the total global payment market in 2019. More specifically, the global mobile payment market was $780 billion in that year, with an annual growth rate of 25.8%. Accenture Consulting [9] believes that the use of traditional payment instruments will significantly reduce in the next 10 years, and mobile payments will replace them and become the most popular tools for payment.

Despite the upward trend in mobile payments globally, their adoption in Taiwan has failed to meet the expected target [10]. The coverage rate for mobile payment in advanced countries has already reached 80%, but in Taiwan the figure is far lower. One of the reasons for this is the fierce competition in the Taiwanese financial ecosystem (for example, commercial banks and technology companies). In addition, people are not sufficiently knowledgeable about mobile payment, although information provided by the banks, financial services companies, and government is plentiful. Consumers also worry about the security and privacy issues of mobile payment [11]. These factors have slowed development of mobile payment in Taiwan compared to other countries, and it is therefore important to understand the barriers and difficulties that exist.

According to the Financial Supervisory Commission [12], the financial services infrastructure in Taiwan has significantly improved, with the growth rate for mobile payment usage in 2019 increasing by 67.05% over the previous year. However, only a quarter of consumers are experienced mobile payment users. In January 2020, there were 6215 financial institutions in Taiwan with 30,580 Automated Teller Machines (also known as cashpoints), and this could be regarded as evidence that Taiwanese consumers are used to making cash transactions.

Market structure and customer acceptance affect the coverage of this new method of payment. Past studies have shown that the average failure rate for new products launched was 40% [13]. Consumers are resistant to change when faced with innovation [14], and Heidenreich and Kraemer [15] argued that such resistance is an important factor in the failure of new products. The effect of innovation resistance on consumer intention is therefore subject to increasing attention [16,17,18].

Innovation resistance comes mainly from psychological barriers [18]. Dysfunction occurs when the functional attributes of innovative technologies fail to meet their ideal expectations, and psychological barriers are raised when perception of the attributes of innovative technology is the cause of psychological conflict or other problems for consumers [19]. When customers perceive obstacles and become resistant, they will seek out further information that will set new standards of resistance. The innovation resistance concept can be used to change their current mindset [20]. However, changes must be made to the customer’s psychological state to reduce the conflict caused by the resistance.

Self-determination is explained by the fact that individuals are intrinsically motivated to engage in activities. Self-determination guides their behavior in a self-determined manner according to their own choices and maintains a happy mood [21]. The key conditions for the effective working of biological functions in the human-motivation system are interest, social recognition, and personal values shaped by interpersonal interactions. Humans seek recognition and care as two of their basic needs, and if these are not found the individual will lack motivation. The self-determination theory focuses on the needs that lead individuals to things of interest, to develop activities, and to adapt to the environment.

Ram and Sheth [20] proposed the innovation resistance theory, which states that consumers’ resistance may be aroused by an innovation even though it is capable of providing better services and products. In recent studies, innovation resistance theory has been employed to explore behavior in online banking, although limited attention has been paid to mobile banking and mobile payment behaviors. With the exception of the early adaptors, mobile payment has not been widely accepted by the public [22]. It is important to explore the factors that have resulted in consumer resistance in this case and to provide a marketing strategy for the banking industry to use to promote mobile payment.

Existing research on the intention to adopt innovation focuses on perceived safety, perceived trust, behavioral belief, and personal innovative behavior. Kaur, Dhir [23] employed innovation resistance theory to discuss perspectives on mobile payment solutions, whilst Leong, Hew [24] used a two-staged structural equation modeling–artificial neural network (SEM-ANN) to predict resistance to the m-wallet, and also suggested incentives that might reduce the influence of that resistance. Academics have, however, paid limited attention to understanding the psychosocial perspectives of innovation resistance, and this research aims to address that gap by investigating the drivers and barriers to the usage of mobile payment.

This research makes two contributions to knowledge. First, although extant research in this area has primarily adopted the innovation resistance theory to understand customer resistance to using mobile payment [23,24], it has seldom considered the psychological barriers which influence innovation resistance and further influence consumers’ intention to use mobile payments. This study suggests that consumer resistance to mobile payments depends not only on complexity, image, and risk barriers, but also on the extent of the consumer’s self-determination, including their autonomy, competence, and relatedness. Second, through the employment of self-determination theory, the study posits that self-determination is an antecedent which influences and minimizes consumer innovation resistance to the use of mobile payments. Thus, using two underpinning theories, this study proposes a model that examines the applicability of the theories and assesses the relative importance of understanding consumers’ innovation resistance with regard to the adoption of mobile payments.

2. Literature Review

2.1. Mobile Payment

Mobile phones have affected the daily life of billions of people around the world and have dramatically changed the function of the original telephone. The added value of mobile phones has far surpassed the basic functions of the telephone to make and receive voice calls. Mobile phones have stimulated the development of the value-added space of mobile payments. The mobile phone and other mobile devices, such as tablets, have driven the growth of mobile businesses. These devices are engaged in marketing activities, sales, production and delivery of products and services between businesses and customers. In fact, mobile devices themselves have become payment instruments. Not only do they serve as a business platform, mobile devices also facilitate monetary transactions [25].

The private sector is responding to this development through mobile payments [26,27]. The banking industry plays an important role in mobile payments. Mobile network operators and other non-banking institutions have launched a broad array of financial services. These services include international and local remittances, deposits and collections, retail payments, loan payments, repayments, stock trading, and even electronic money. The growth of these mobile financial services depends on customer needs and the business environment and model [26,27].

Mobile payments are financial transactions (including mobile money and e-wallet transactions) conducted on or via various mobile and wearable devices [26,27,28,29]. At present, mobile payments are only available in a limited number of countries and are not yet globally accepted [29]. Technological innovation, improved socioeconomic environments, and the proliferation of mobile devices will drive the development of mobile payments in developing markets [30]. Therefore, the eventual globalization of mobile payments is a challenge that governments and businesses will have to face.

2.2. Innovation Resistance Theory

Rogers [31] proposes that new products and developments are spread and shared through social systems. Product innovation is a process of great uncertainty and the launch of new products can have many effects on a company’s competitiveness [32,33]. On one hand, revenues from new products and services can help companies to achieve profitability and market position [34], but new products with lower revenues may be abandoned if they are seen to hurt the company’s competitiveness, destroy its brand image, or have a negative financial impact on investors [35]. Therefore, identifying the cause of product failure is a core challenge when managing a company’s innovation activities.

Understanding the reasons why people do not use a new product is as important as understanding why they use it. The conclusion not only helps with the development phase of new products, but also suggests adjustments to existing ‘new’ products. According to the authors Midgley and Dowling [36], the innovation resistance model can be seen as a feedback model that draws inferences from a negative perspective. Midgley and Dowling [36] believe that although many researchers are interested in the proliferation of new product innovations, some scholars still focus on resistance. Therefore, further research on confrontation should help to broaden the understanding of innovative behavior.

In the past, scholars have maintained a positive attitude towards new product innovations, but only a few researchers have been interested in resistance [37]. Mittelstaedt and Grossbart [38] proposed a resistance model that includes the notion of symbolic adoption or resistance. The model concludes that there are many reasons for human resistance, and it divides them into three types [38]. In the first, innovation resistance can be generated as a result of gathering new ideas or information. In the second type, individuals accept new things symbolically, but refuse to enter into the evaluation stage of using those things. In the third type, symbolic acceptance occurs if the individual is unwilling or unable to enter into the evaluation stage of using new things, and in this circumstance, a procrastination situation may occur. Gatignon and Robertson [39] showed that resistance to innovation can be divided into two types: rejecting innovation and delaying innovation. Those who reject innovation are those who already have sufficient information, and it is challenging to make them change their mind. In contrast, individuals who delay innovation adoption can potentially be persuaded. More information is required by these people who may move gradually toward acceptance. The latter approach is common to the majority of people [14]. Therefore, it is essential for academia and practitioners to understand innovation resistance so that it can be corrected or amended and successful innovation can be achieved.

2.3. Self-Determination Theory

Numerous studies explore the motivations of personal behavior, but they have been notably discussed in terms of Maslow’s hierarchy of needs [40], which identifies the five hierarchical elements: physiological, security, social, self-esteem, and self-fulfilling needs. Self-determination theory originated from the exploration of motives for media behavior or the activities that meet basic human psychological needs [41]. Early research into self-determination theory has focused mainly on intrinsic motivation.

Self-determination theory explains how humans achieve goals or develop activities through psychological or perceptual responses. In the case of self-determination theory, these psychological or perceptual responses can integrate different forms of motivation [21]. The theory defines extrinsic motivation as rewards (such as money or food), whilst intrinsic motivation is a psychological or perceptual response that is regulated by different levels of choice or self-will, or through interpersonal or inner spiritual power [41]. According to self-determination theory, intrinsic motivation is illustrated by the internal reasons or needs driving consumers to execute a behavior.

There is another perspective to self-determination theory. According to Deci and Ryan [41], “there is a set of universal needs that must be satisfied for effective functioning and psychological health (p. 183)”. Ryan and Deci [42] further proposed that there are three types of needs, autonomy, competence, and relatedness, which influence peoples’ psychological well-being. Relatively limited attention has been paid to the influence of self-determination theory on the influences of innovation. For example, studies apply the self-determination theory in the field of broadcasting intention on Twitch [43]. Migliorini and Cardinali [44] employed the self-determination theory approach on customers facing health innovation challenges.

This study applied self-determination theory to discuss consumers’ intention to use mobile payment, and more specifically, when faced with using this innovative payment method, how the self-determinants influence consumers’ psychosocial perception. Three types of needs, autonomy, competence, and relatedness, from self-determination theory, are proposed as the antecedents. This study, therefore employed self-determination theory to examine consumers’ psychological perception of innovation.

3. Research Methods

3.1. Hypotheses Development

Harisson, Laplante [45] discussed employees’ resistance behaviors when introducing total quality management and adopting mobile network theory. The study concluded that employees require autonomy and that sufficient autonomy allows employees to fully express their opinions. Meier, Ben [46] explored employees’ attitude toward organizational transformation in the public IT services sector using the technology acceptance model. Their conclusion was that the organizational transformation failed because employees were worried about losing their autonomy. The study also indicated that autonomy, perceived quality of information, and social influence had a significant impact on innovation resistance.

Autonomy is regarded as a self-oriented psychological perception and as an intrinsic motivation that drives behavior. Purchasing will take place or behavior will be executed when a need is formulated and people intend to fulfill that need [47]. In the marketing discipline, several factors, including demographic variables [48], skills, and knowledge, have been found to influence innovation adoption or resistance; however, innovation resistance applies not only to functional but also to psychological barriers. de Bellis and Venkataramani Johar [49] argued that the main reason for innovation resistance is autonomy. Antioco and Kleijnen [50] explored the influences of autonomy, competence, and relativeness on technological innovation adoption. Schweitzer and Gollnhofer [51] confirmed that autonomy as an influential determinant has an impact upon new product adoption.

Three barriers—the complexity barrier, image barrier, and risk barriers—are employed to understand the innovation resistance to mobile payments. Previous studies provide discussions that support the relationships between autonomy and the three barriers. Mani and Chouk [16] explored the relationship between the complexity barrier and autonomy. The stronger the autonomy that exists, the lower the perceived complexity. When consumers autonomously learn to use a new technology, this demonstrates that they have overcome the complexity barrier with regard to the new task. Both autonomous adoption and previous experience influence consumer purchase intention [51]. Schweitzer and Gollnhofer [51] further employed a qualitative method to understand the relationship between autonomy and perceived image. The risk barrier is an influential factor in new product adoption from the consumers’ perspective [52]. When perceived control is higher, then perceived risk is lower. Thus, it is proposed that autonomy influences the risk barrier in innovation resistance.

Likewise, this study proposes that the autonomy of using mobile payment has a negative influence on innovation resistance in terms of three barriers. Hypotheses 1–3 are stated below:

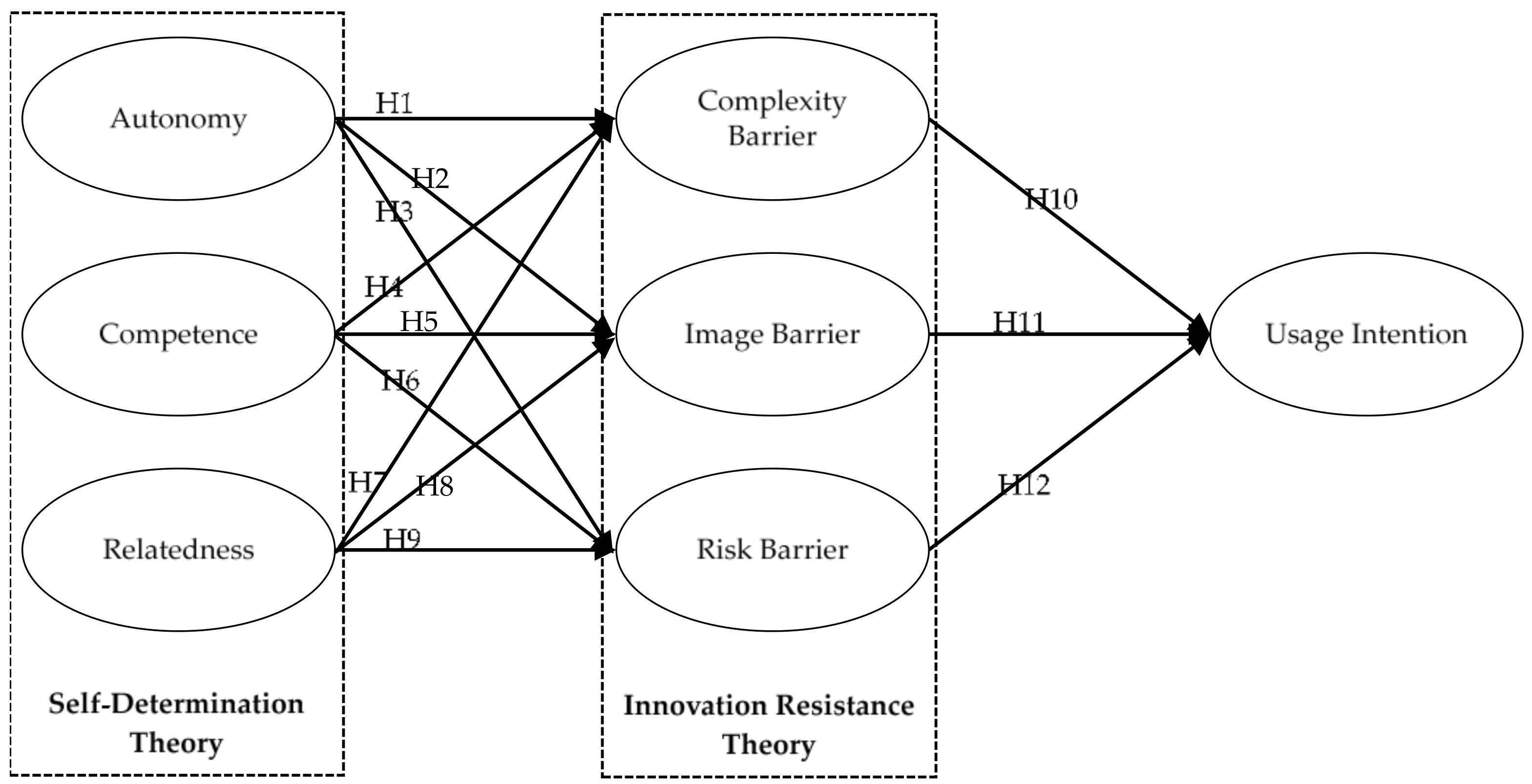

Hipothesis 1 (H1).

The autonomy of using mobile payment has a significant and negative effect on the complexity barrier.

Hipothesis 2 (H2).

The autonomy of using mobile payment has a significant and negative effect on the image barrier.

Hipothesis 3 (H3).

The autonomy of using mobile payment has a significant and negative effect on the risk barrier.

Competence is the perceived control of the internal and external environment. Harisson and Laplante [45] pointed out that employees must be competent to implement their company’s systems and reduce the degree of the innovation resistance. Students with higher degrees of competence achieve better performance in the learning process [53] and are thus more willing to take up a new course or tackle new challenges. Competence refers to the feeling that one is able to act in the environment and to reach a desired goal [44]. It is employed by the current study to discuss the innovation resistance.

Andreinald and Prayoga [54] posited that employees’ competence includes their knowledge, skills, and experience. Higher competence results in better outcomes in terms of working performance evaluation. Even when facing a complicated and challenging task, a highly competent employee is expected to complete it. Therefore, this study aims to understand the influence of competence on the innovation complexity barrier. Garretson and Clow [55] also explored consumer’s awareness of various risks in the process of adopting products. If these perceived risks are too high, consumer incompetence will hinder consumer willingness to adopt products.

Thus, this study posits that competence has a negative impact on the risk barrier to innovation. Personal competence is also considered to be influential in the perceived image of products or services [56]. When a person with a higher level of competence is seen to have adopted an innovation, this may produce a stronger perceived image of a low-quality product or poor service.

Therefore, hypotheses 4–6 propose that:

Hipothesis 4 (H4).

The competence of using mobile payment has a significant and negative effect on the complexity barrier.

Hipothesis 5 (H5).

The competence of using mobile payment has a significant and negative effect on the image barrier.

Hipothesis 6 (H6).

The competence of using mobile payment has a significant and negative effect on the risk barrier.

In many circumstances, companies provide as much information as possible when promoting a new product or service, but this marketing approach can lead to a negative response from customers. Kleijnen and Lee [57] argued that mass information provision leads to consumer disfavor when a new product is launched, and that relevant information which fulfills customer needs is more than adequate. This study intended to explore the relationship between relativeness from self-determination theory and innovation resistance

Leung and Matanda [58] employed self-determination theory to discuss customers’ adoption of self-service technologies. In contrast to relatedness, their study suggests that three dimensions—autonomy, competence, and perceived anonymity—can predict consumer adoption intention with regard to self-service technologies. The results confirmed that perceived anonymity is positively associated with adoption intention. Relatedness, however, produced the opposite effect to perceived anonymity [58]. Therefore, the current study aimed to understand the relationship between relatedness and innovation acceptance or resistance.

Relatedness refers to the need to maintain a relationship in a social environment [44], which is important to increase a perception of belonging [59]. When people feel connected with a specific brand or company, that attachment influences their choice of new smart phone [60], but if that connection is missing, perceived risk or perceived complexity may result from the unfamiliarity of an unknown product. Resistance can emerge as the consumer communicates with other customers and companies and identifies potential problems. These problems can lead consumers to resist new products. Peter and Tarpey Sr. [61] developed strategies to make customers feel connected to a company in order to reduce expected losses and perceived risk. To extend these conclusions, this study investigated the relationship between relatedness and innovation resistance. In identifying the influence of relatedness, the risk, complexity, and image barriers are regarded as dependent variables.

Hence, hypotheses 7–9 propose that:

Hipothesis 7 (H7).

The relatedness of using mobile payment has a significant and negative effect on the complexity barrier.

Hipothesis 8 (H8).

The relatedness of using mobile payment has a significant and negative effect on the image barrier.

Hipothesis 9 (H9).

The relatedness of using mobile payment has a significant and negative effect on the risk barrier.

Innovation resistance occurs when an existing behavior pattern is altered. Ram [14] believes that satisfaction is generated when consumers receive benefits from an innovation, but there is conflict when that innovation offends their original belief. Mobile payment, introduced in recent years, is an innovative payment method that is quite different from traditional approaches using cash or credit card. The mobile payment service attempts to change consumers’ existing payment model whilst they still have doubts about its usage. Based on these arguments, this study infers that mobile payment services are an attempt to change people’s existing payment models and can easily conflict with their existing beliefs, causing them to resist their adoption. Thus, hypotheses 10–12 are:

Hipothesis 10 (H10).

The complexity barrier has a significant and negative effect on the intention to use mobile payments.

Hipothesis 11 (H11).

The image barrier has a significant and negative effect on the intention to use mobile payments.

Hipothesis 12 (H12).

The risk barrier has a significant and negative effect on the intention to use mobile payments.

3.2. Research Framework

This study integrated two theories, innovation resistance theory, proposed by Ram and Sheth [20], and self-determination theory, posited by Deci and Ryan [62]. It explored consumer’s usage intention with regard to mobile payment by combining these two theories. The proposed research model is shown in Figure 1.

3.3. Common Method Bias Test

Common method variance was applied to assess the systematic bias among the variables [63,64] that this study employed using Harman’s one-factor test [65]. All items of measurement scale were analyzed by exploratory factor analysis in order to identify systematic bias. Six factors were extracted and the explanatory power of the first factor is 23.37% which is far below the cap (50%) suggested by Harman [65]. These results indicate that there is no common method bias in this study.

4. Results

This section provides a descriptive statistical analysis of the distribution of sample structures, the scores of the dimensions and scale items to understand the characteristics of the sample.

4.1. Measures

The data were collected in Taiwan in order to examine the proposed conceptual framework. Measures of competence, relatedness, and autonomy were adopted from self-determination theory, as in Rezvani and Khosravi [66], and the measures complexity barrier, image barrier, and risk barrier were adopted from innovative resistance theory, as in Laukkanen and Sinkkonen [67]. In addition, the measures of mobile payments intention were adopted from Fagan and Neill [68]. The list of the items is displayed in Appendix A. A seven-point Likert scale was employed. Demographic questions were also included in the questionnaire. Given that the scales were available in English from previous research, translation from English to Chinese was required since the survey was to be conducted in Taiwan. To finalize the validity of the words used in the questionnaire, the translation was extensively discussed and modified by three linguistic professionals. Thirty responses were collected to ensure the reliability and validity of the questionnaire. Cronbach’s α for each dimension was higher than 0.8 [69]. Results from exploratory factor analysis showed that the factor loading of each extracted factor was larger than 0.6, whereas communality was more than 0.5 [70]. The reliability and validity of the constructs in this study met the satisfactory standards. The questionnaire was then released for data collection.

4.2. Data Screening

Data were collected using a convenience sampling approach and the My Survey (www.mysurvey.tw) online platform. To ensure that data collection went smoothly, a small incentive was provided to encourage participation and questionnaire completion. This study aimed to understand consumers’ perception of mobile payments, so all participants with experience of online payment were allowed to participate in the survey. A total of 398 questionnaires were distributed by the online platform, and when the collected samples were sorted and screened, the number of valid samples was 348. Demographic statistics are shown in Table 1.

4.3. Reliability and Validity Analysis

Reliability was examined using Cronbach’s alpha, composite reliability (CR) and the average variance extracted (AVE) for each construct of this study. The results are shown in Table 2 and met the satisfactory standards. Composite reliability (CR) and Cronbach’s alpha values for all measures were greater than 0.70 [71], whereas values of average variance extracted (AVE) were higher than 0.50 [72]. Furthermore, three steps are required to justify discriminant validity. First, the Fornell Larcker criterion [73] is shown in Table 3. The diagonal AVE square root indicates that the diagonal value is greater than the dimension correlation coefficient value. Second, in Table 4, the cross-loading indicates that, when the dimensions are combined, the dimension is larger than the other dimension values. Finally, the Heterotrait–Monotrait ratio (HTMT), in Table 5, determines whether the validity criterion is below the threshold of 0.90 [74]. Based on the above, the reliability and validity are well demonstrated in this study.

The overall adaptation model in Smart-PLS focuses on the identification of each indicator: SRMR (Standardized Root-Mean-Square Residual) is an absolute adaptation indicator, measuring the misspecification of hypotheses [75] where SRMR values less than 0.10 means the better the fit. The value of d_ULS needs to be less than the upper limit of the confidence interval, which means that the difference between the model correlation matrix and the empirical correlation matrix is small and can be attributed to the sampling error. Chi-Squared mainly measures the extent to which this hypothesis reflects the observations and does not have a measure of fitness itself. The closer the Normed Fit Index (NFI) value is between 0 and 1, the better the fit, and an NFI value above 0.80 represents an acceptable fit [76]. To conclude, the model-fit is demonstrated in this study. This study complies with Smart-PLS regulations in the structural model set estimation model. Therefore, it can be concluded that this study is more suitable in the adaptation model (see Table 6).

4.4. Structural Analysis

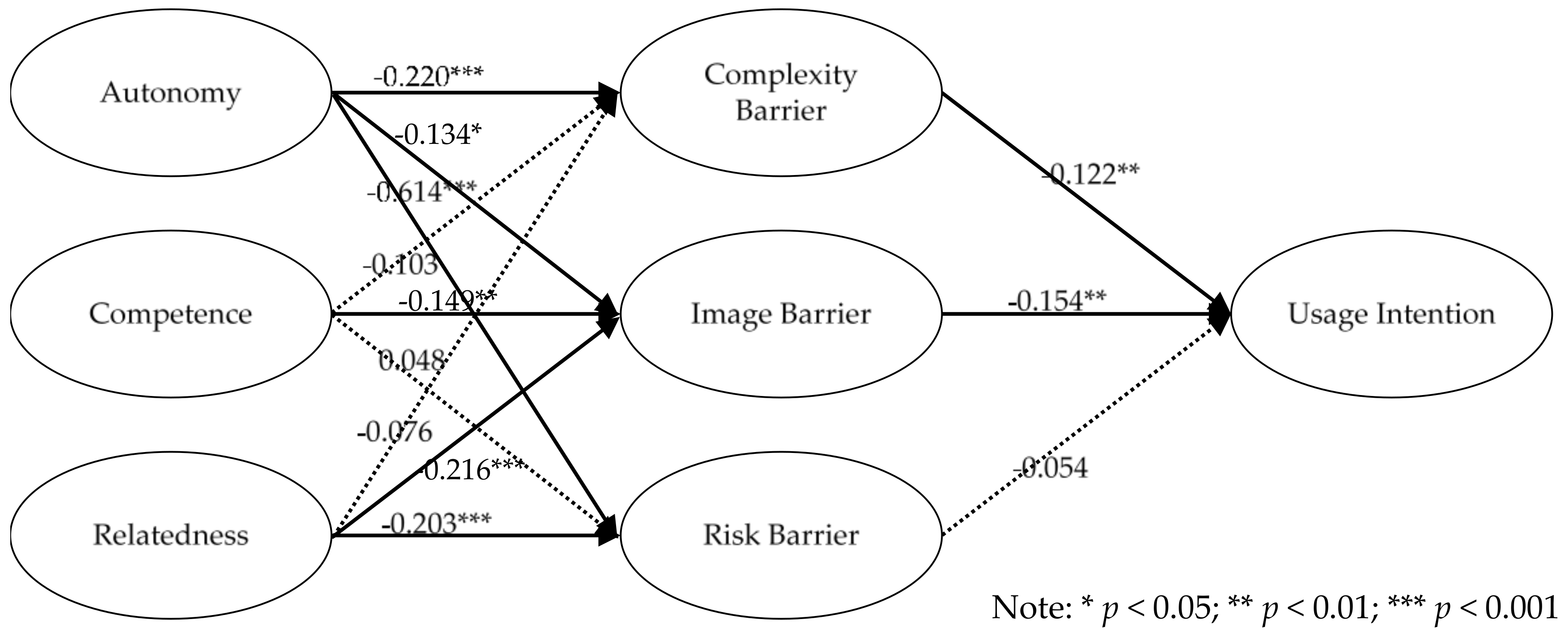

Path analysis mainly carries out the causal relationship verification among the potential variables in the research structure. The path coefficients in Table 4, Table 5 and Table 6 have been standardized, which represents the direct effect among the potential variables. The larger the value, the greater the interaction between the variables. The majority of the hypotheses in this study are supported, but H4, H6, H7, and H12 (H4: competence on complexity barrier, H6: competence on risk barrier, H7: sense of connection to complexity barrier, and H12: risk barrier on adopting intention) are not supported. The summary of the results is shown in Figure 2 and Table 7.

5. Conclusions and Discussion

This section presents the discussion, conclusion, recommendations, and management implications of the study. The research model proposed by this investigation adopted two theories from previous research, the innovation resistance theory and the self-determination theory. This study proposed an integrated framework and employed mobile payment users in Taiwan as the respondents. The proposed model explored consumer self-determination and resistance factors that affect consumers’ usage intention with regard to mobile payments.

5.1. Discussion

From the results, although there has been an increase in the usage of mobile commerce and mobile payments, currently only a specific group of people will easily adopt the new technology. This group of people are in their thirties, hold a university degree, work in the financial sector, and earn a good salary. The results show that although this group may accept mobile payment methods easily, the risk barrier of innovation resistance exists and is influenced by the competence and relatedness of self-determination. Therefore, it is important to understand the factors which generate innovation resistance. Moreover, business should create a strategy to eliminate or reduce the impact of innovation resistance.

Differences in gender, age, occupation, and length of time using mobile payment methods can result in different interpretations of mobile commerce. Marketing strategies should be differential and relevant, guiding customers to understand the convenience and benefits of using mobile payments. Ultimately, this should increase willingness and intention to use. The research found that people of different ages have different levels of resistance to mobile banking. The younger the age group, the higher their acceptance of new information. Older people have accumulated more life experience, which makes it harder for them to change their point of view, and in this case, easier to develop resistance toward new technology and mobile commerce. With regard to gender, it has been found that more men are using mobile payment methods than women. This is because men tend to have a strong interest in new or creative topics they can discuss with their peers. Marketers can analyze users’ backgrounds to discover which parties are most likely to accept the mobile payment approach, and draft appropriate strategies to encourage its use.

Self-determination theory considers a person’s innate talent and their psychological needs. Rather than external causes and influences, it is mainly discovering one’s motive. Consumers who are innovation-resistant tend, when faced with an innovative product or service, to self-evaluate their needs with regard to that product. Therefore, the main reason for consumers to accept innovative products or service is if they perceive the same innovative qualities.

This research explained that the higher the sense of autonomy, the lower the complexity barrier for mobile commerce. This indicates that those with a higher sense of autonomy will actively use new technology and seek help when they need it. Eventually, as more people use the new technology, the complexity barrier for mobile commerce is lowered. From the competency perspective, it should be understood that competency itself is an individual’s ability; an evaluation of how an individual can complete a task. Therefore, as competency increases, users will start to appreciate the functions of mobile payment and find ways to better use those functions, thus lowering the barriers. On the other hand, relatedness refers to maintaining the relationship with others. More frequent usage results in familiarity and connection from the customers’ side to the service side. Perceived risk from the mobile payments will be reduced. Therefore, negative correlation is verified between relatedness and risk barriers.

From the viewpoint of innovation resistance, the findings are that innovation diffusion and innovation resistance are two sides of the same thing; they are not related but instead coexist. To a certain extent, consumers face the changes brought by innovation, and innovation resistance is their response to those changes. Once innovation resistance has been overcome, consumers will adopt the innovation. Thus, innovation resistance can be seen as a habit when reacting to innovation, or a process that must be gone through before innovation can be adopted. In this study, with the exception of the risk barrier, innovation resistance has a significant impact on user intention. The risk barrier refers to a certain degree of risk carried by the innovation. Innovation involves many uncertainties and potential surprises; therefore, when consumers acknowledge the existence of risk, they need to overcome that risk in order to embrace the innovation.

If the software or hardware of a mobile payment is complicated, it will reduce intention to use mobile payments. Also, due to image barrier in the finance industry, when a new product has a bad image, the intention to use that product will be low. Therefore, banks must package their products to reduce the risk of image barrier and increase people’s intention to use. The risk barrier is known to have little effect on user intention; however, younger people have more faith in financial products and greater intention to try new things.

5.2. Research Contribution

Many studies about mobile payments discuss the perception of innovative technology services toward their usage intention. This research proposed a conceptual model providing different angles to understand the resistance of using mobile payments. It makes three theoretical contributions to knowledge.

First, an integrated framework was proposed by adopting two theories, the self-determination theory and the innovative resistance theory. This model gives a better understanding of NOT using mobile payments.

Second, the study explored the circumstances which arouse consumer resistance to using mobile payments. It took the different levels of resistance into account, from complexity, impressions, and risks to the final use of the mobile payments process. This is in line with past research studies on the usage intention of the mobile payments. The study found that, apart from innovation resistance, consumers will adapt their learning styles to new payment methods in the early stages of mobile payment usage. Future research could take this into consideration when discussing usage intention with regard to mobile payments.

Third, from self-determination theory, the usage intention of mobile payments is affected by the ability of consumers themselves. Alternatively, from innovative resistance theory, the intention NOT to use mobile payment is affected by changes in technology. Both perspectives provide a holistic picture of our understanding of mobile payment usage.

5.3. Practical Implications

Nowadays, mobile payments are common in many countries, and as a payment tool, it is convenient and effective for both consumers and businesses. In Taiwan, the popularity of mobile devices is high and the mobile network infrastructure is well established. Both the financial services industry and government have made considerable efforts to promote the usage of mobile payment systems, but their acceptance is still limited. This study provides four managerial implications for practitioners.

First, a negative relationship was found between autonomy and complex obstacles. The higher the sense of autonomy, the lower the complexity that is sensed. Under such circumstance, people consider using new technologies of their own free will, and will seek assistance or find solutions as and when they encounter difficulties using those new products or services. Obstacles to adoption are thus reduced.

Second, from a competency perspective, consumers set out to master the function and operation of mobile payments. They seek effective and efficient solutions to using the facility, thereby reducing the obstacles to usage.

Third, relatedness refers to an intention to interact with others. If using mobile payments provides an opportunity to interact with, say, service providers, the complexity barrier will be reduced and people will be more willing to use the service.

Fourth, the complexity of operating mobile payment systems results in a lower intention to use them. Moreover, the impression created by new products can affect both customer purchasing and usage intentions. The banking industry should simplify the operating interface for mobile payments, which would create a positive image for its use. Consumers with these impression and perception would be more willing to use mobile payments.

To conclude, the process of using mobile payments is easier and clearer, which will increase consumers’ intention to use them. Financial service providers could affect the intention to use mobile payments by appropriate interaction with customers and the introduction of new products. Moreover, customer representatives should bear in mind the concerns of customers with a view to facilitating the usage of mobile payments. The current study provides implications for the banking industry and financial service providers, and suggests strategies for increasing customer intention and reducing resistance to mobile payment usage.

In Taiwan, the acceptance of mobile payments is relatively low, despite the innovative technology developed by the service providers to create successful strategies that will attract greater usage and obtain higher profits. The results of this study show that innovation resistance for mobile payments is negatively influenced by autonomy, competence, and relatedness, and businesses should eliminate or minimize those factors that have a negative impact on innovation adoption. For example, technological companies should provide user-friendly apps, which may reduce the complexity barrier and further prompt customer adoption of mobile payment. On the other hand, data encryption could be applied to lower the risk barrier, and increase the adoption of mobile payments. Perceived risks and worries are generated by the unfamiliarity and limited knowledge and skills surrounding innovative technology, but relevant and useful information provision can effectively reduce those worries and create a positive image that becomes associated with that technology. Banking and financial services companies could produce commercials or provide instructions that lower the image barrier and further increase customer adoption of mobile payment systems.

5.4. Limitations

Through rigorous research, this study illustrates the reasons and ideas behind consumer resistance and uses self-determination theory to explore the actual state of mobile payments by consumers. However, the limitations of the work should be addressed in order to identify opportunities for future research. First, an online questionnaire was employed, which meant that non-internet users were not involved and their opinions could not be investigated. Future studies could use field investigations to improve understanding of consumer resistance to the use of mobile payments. Second, the research explored the key factors of consumer resistance to mobile payments, and the conclusions cannot be extended to other financial services or products. Third, the scales were adopted from previous studies, so the items in each construct may be limited. Although the model was statistically both reliable and valid, it is challenging to justify the representativeness of each construct. Fourth, this research focuses on risk, image, and complexity barriers only, and other innovation barriers are not discussed. Future research could consider the subject from the viewpoint of other barriers. Finally, the main purpose of this study was to discover why consumers resist mobile payments and their response toward its use, but the research only examines the intention to use mobile payments in Taiwan and therefore cannot be extended to other countries or regions. However, the result can still provide insights for academics and practitioners outside of Taiwan. In the future, surveys could be conducted in other countries to increase the generality of the results.

Author Contributions

K.C.C. and S.W.-J.L. conceived of the presented idea and contributed to the manuscript. K.C.C. developed the theoretical framework, carried out data collection and analyzed the data. S.W.-J.L. aided in interpreting the results and editing the final manuscript. All authors provided critical feedback and helped shape the research, analysis and manuscript. All authors have read and agreed to the published version of the manuscript.

Funding

There is no funding for this study.

Conflicts of Interest

The authors declare no conflict of interest.

Appendix A

Relatedness

I am satisfied when using the mobile payment.

I have gotten used to having mobile payment.

I feel a close connection to others when using the mobile payment.

Autonomy

It is convenient for me to use the mobile payment.

I feel that mobile payments are a necessity in my daily life.

I feel there are some difficulties in using the mobile payment.

I feel that I am able to complete my tasks or reach my goals when using the mobile payment.

When I see others using mobile payments, I feel that I am able to do so, too.

Complexity barrier

If no instruction manual is provided, I may not be able to successfully use the mobile payment or even attempt to try.

I find the user interface for mobile payment to be too complicated.

There is limited information available when using the mobile payment.

I need expert guidance when using the mobile payment.

Competence

I find it very easy to use mobile payment services.

I find it very convenient to use mobile payment services.

I find it very efficient to use mobile payment services.

I find it is very convenient to change my PIN code when using mobile payment services.

Image barrier

It is my impression that new technology is often too complicated

It is my impression that mobile payment services are difficult to use.

Risk barrier

I worry that while I am using the mobile payment, I might type in incorrect information as it is difficult to check for accuracy on a screen.

I worry that while I am using the mobile payment, someone may hack my account.

I worry that any information transmitted through the Internet may be used improperly.

Using intention

I intend to use the mobile payment.

I will use mobile payment apps again when I purchase products.

I intend to use the mobile payment app again to make additional purchases in the future.

References

- eMarketer. Mobile Taiwan: A look at A Highly Mobile Market. Available online: https://www.emarketer.com/Article/Mobile-Taiwan-Look-Highly-Mobile-Market/1014877?ecid=NL1007 (accessed on 28 July 2020).

- Taiwan Network Information Center. 2019 The Internet Report in Taiwan; Taiwan Network Information Center: Taipei, Taiwan, 2019. [Google Scholar]

- Marriott, J.W., Jr.; Sorenson, A.M. Marriott International, Inc. 2018 Annual Report; Marriott International, Inc.: Bethesda, MD, USA, 2018. [Google Scholar]

- Holmes, A.; Byrne, A.; Rowley, J. Mobile shopping behaviour: Insights into attitudes, shopping process involvement and location. Int. J. Retail Distrib. Manag. 2014, 42, 25–39. [Google Scholar] [CrossRef]

- Sabareeshan, K. 5 Disadvantages of Handling Cash. Available online: https://www.asiaone.com/money/5-disadvantages-handling-cash (accessed on 28 July 2020).

- Chen, S.-C.; Chung, K.C.; Tsai, M.Y. How to achieve sustainable development of mobile payment through customer satisfaction—The SOR model. Sustainability 2019, 11, 6314. [Google Scholar] [CrossRef] [Green Version]

- Téllez, J.; Zeadally, S. Mobile Payment Systems: Secure Network Architectures and Protocols; Springer: Cham, Switerland, 2017. [Google Scholar]

- Filieri, R.; Chen, W.; Dey, B.L. The importance of enhancing, maintaining and saving face in smartphone repurchase intentions of Chinese early adopters: An exploratory study. Inf. Technol. People 2017, 30, 629–652. [Google Scholar] [CrossRef]

- Accenture Consulting. 2015 North America Consumer Digital Payments Survey; Accenture Consulting: Dublin, Ireland, 2015. [Google Scholar]

- Anil, S.; Ting, L.T.; Moe, L.H.; Jonathan, G.P.G. Overcoming barriers to the successful adoption of mobile commerce in Singapore. Int. J. Mob. Commun. 2003, 1, 194–231. [Google Scholar] [CrossRef]

- Qin, Z.; Sun, J.; Wahaballa, A.; Zheng, W.; Xiong, H.; Qin, Z. A secure and privacy-preserving mobile wallet with outsourced verification in cloud computing. Comput. Stand. Interfaces 2017, 54, 55–60. [Google Scholar] [CrossRef]

- Taiwan Financial Supervisory Commission. Financial Statistics Abstract; Financial Supervisory Commission Taiwan: Taipei, Taiwan, 2020. [Google Scholar]

- Castellion, G.; Markham, S.K. Perspective: New product failure rates: Influence of argumentum ad populum and self-interest. J. Prod. Innov. Manag. 2013, 30, 976–979. [Google Scholar] [CrossRef]

- Ram, S. A model of innovation resistance. In NA—Advances in Consumer Research; Wallendorf, M., Anderson, P., Eds.; Association for Consumer Research: Provo, UT, USA, 1987; Volume 14, pp. 208–212. [Google Scholar]

- Heidenreich, S.; Kraemer, T. Innovations-doomed to fail? Investigating strategies to overcome passive innovation resistance. J. Prod. Innov. Manag. 2016, 33, 277–297. [Google Scholar] [CrossRef]

- Mani, Z.; Chouk, I. Drivers of consumers’ resistance to smart products. J. Mark. Manag. 2017, 33, 76–97. [Google Scholar] [CrossRef]

- Patsiotis, A.G.; Hughes, T.; Webber, D.J. An examination of consumers’resistance to computer-based technologies. J. Serv. Mark. 2013, 27, 294–311. [Google Scholar] [CrossRef]

- Talke, K.; Heidenreich, S. How to overcome pro-change bias: Incorporating passive and active innovation resistance in innovation decision models. J. Prod. Innov. Manag. 2014, 31, 894–907. [Google Scholar] [CrossRef]

- Heidenreich, S.; Handrich, M. What about passive innovation resistance? Investigating adoption-related behavior from a resistance perspective. J. Prod. Innov. Manag. 2015, 32, 878–903. [Google Scholar] [CrossRef]

- Ram, S.; Sheth, J.N. Consumer resistance to innovations: The marketing problem and its solutions. J. Consum. Mark. 1989, 6, 5–14. [Google Scholar] [CrossRef]

- Deci, E.L.; Ryan, R.M. A motivational approach to self: Integration in personality. In Nebraska Symposium on Motivation, 1990: Perspectives on Motivation; University of Nebraska Press: Lincoln, NE, USA, 1991; pp. 237–288. [Google Scholar]

- Zhou, T. An empirical examination of continuance intention of mobile payment services. Decis. Support Syst. 2013, 54, 1085–1091. [Google Scholar] [CrossRef]

- Kaur, P.; Dhir, A.; Singh, N.; Sahu, G.; Almotairi, M. An innovation resistance theory perspective on mobile payment solutions. J. Retail. Consum. Serv. 2020, 55, 102059. [Google Scholar] [CrossRef]

- Leong, L.-Y.; Hew, T.-S.; Ooi, K.-B.; Wei, J. Predicting mobile wallet resistance: A two-staged structural equation modeling-artificial neural network approach. Int. J. Inf. Manag. 2020, 51, 102047. [Google Scholar] [CrossRef]

- Jenkins, B. Developing Mobile Money Ecosystems; International Finance Corporation and Harvard Kennedy School: Washington, DC, USA, 2008. [Google Scholar]

- Dahlberg, T.; Guo, J.; Ondrus, J. A critical review of mobile payment research. Electron. Commer. Res. Appl. 2015, 14, 265–284. [Google Scholar] [CrossRef]

- Dahlberg, T.; Mallat, N.; Ondrus, J.; Zmijewska, A. Past, present and future of mobile payments research: A literature review. Electron. Commer. Res. Appl. 2008, 7, 165–181. [Google Scholar] [CrossRef] [Green Version]

- Dermish, A.; Kneiding, C.; Leishman, P.; Mas, I. Branchless and mobile banking solutions for the poor: A survey of the literature. Innov. Technol. Gov. Glob. 2011, 6, 81–98. [Google Scholar] [CrossRef]

- Evans, D.S.; Pirchio, A. An empirical examination of why mobile money schemes ignite in some developing countries but flounder in most. SSRN Electron. J. 2015. [Google Scholar] [CrossRef] [Green Version]

- Kazan, E.; Tan, C.-W.; Lim, E.T.K.; Sørensen, C.; Damsgaard, J. Disentangling digital platform competition: The case of UK mobile payment platforms. J. Manag. Inf. Syst. 2018, 35, 180–219. [Google Scholar] [CrossRef] [Green Version]

- Rogers, E.M. Diffusion of Innovations, 3rd ed.; Free Press: New York, NY, USA, 1983. [Google Scholar]

- Bissola, R.; Imperatori, B.; Colonel, R.T. Enhancing the creative performance of new product teams: An organizational configurational approach. J. Prod. Innov. Manag. 2014, 31, 375–391. [Google Scholar] [CrossRef]

- Hansen, J.M.; McDonald, R.E.; Mitchell, R.K. Competence resource specialization, causal ambiguity, and the creation and decay of competitiveness: The role of marketing strategy in new product performance and shareholder value. J. Acad. Mark. Sci. 2013, 41, 300–319. [Google Scholar] [CrossRef]

- Markham, S.K.; Lee, H. Product development and management association’s 2012 comparative performance assessment study. J. Prod. Innov. Manag. 2013, 30, 408–429. [Google Scholar] [CrossRef]

- Urbig, D.; Bürger, R.; Patzelt, H.; Schweizer, L. Investor reactions to new product development failures:The moderating role of product development stage. J. Manag. 2013, 39, 985–1015. [Google Scholar] [CrossRef] [Green Version]

- Midgley, D.F.; Dowling, G.R. A longitudinal study of product form innovation: The interaction between predispositions and social messages. J. Consum. Res. 1993, 19, 611–625. [Google Scholar] [CrossRef]

- Matsuo, M.; Minami, C.; Matsuyama, T. Social influence on innovation resistance in internet banking services. J. Retail. Consum. Serv. 2018, 45, 42–51. [Google Scholar] [CrossRef]

- Mittelstaedt, R.A.; Grossbart, S.L.; Curtis, W.W.; DeVere, S.P. Optimal stimulation level and the adoption decision process. J. Consum. Res. 1976, 3, 84–94. [Google Scholar] [CrossRef]

- Gatignon, H.; Robertson, T.S. Technology diffusion: An empirical test of competitive effects. J. Mark. 1989, 53, 35–49. [Google Scholar] [CrossRef]

- Maslow, A.H. Motivation and Personality; Harpers: Oxford, UK, 1954. [Google Scholar]

- Deci, E.L.; Ryan, R.M. The “What” and “Why” of goal pursuits: Human needs and the self-determination of behavior. Psychol. Inq. 2000, 11, 227–268. [Google Scholar] [CrossRef]

- Ryan, R.M.; Deci, E.L. Self-determination theory and the facilitation of intrinsic motivation, social development, and well-being. Am. Psychol. 2000, 55, 68–78. [Google Scholar] [CrossRef]

- Zhao, Q.; Chen, C.-D.; Cheng, H.-W.; Wang, J.-L. Determinants of live streamers’ continuance broadcasting intentions on Twitch: A self-determination theory perspective. Telemat. Inform. 2018, 35, 406–420. [Google Scholar] [CrossRef]

- Migliorini, L.; Cardinali, P.; Rania, N. How could self-determination theory be useful for facing health innovation challenges? Front. Psychol. 2019, 10, 1870. [Google Scholar] [CrossRef] [Green Version]

- Harisson, D.; Laplante, N.; St-Cyr, L. Cooperation and resistance in work innovation networks. Hum. Relat. 2001, 54, 215–255. [Google Scholar] [CrossRef]

- Meier, R.; Ben, E.R.; Schuppan, T. ICT-enabled public sector organisational transformation: Factors constituting resistance to change. Inf. Polity 2013, 18, 315–329. [Google Scholar] [CrossRef]

- Broniarczyk, S.M.; Griffin, J.G. Decision difficulty in the age of consumer empowerment. J. Consum. Psychol. 2014, 24, 608–625. [Google Scholar] [CrossRef]

- Arts, J.W.C.; Frambach, R.T.; Bijmolt, T.H.A. Generalizations on consumer innovation adoption: A meta-analysis on drivers of intention and behavior. Int. J. Res. Mark. 2011, 28, 134–144. [Google Scholar] [CrossRef]

- De Bellis, E.; Venkataramani Johar, G. Autonomous shopping systems: Identifying and overcoming barriers to consumer adoption. J. Retail. 2020, 96, 74–87. [Google Scholar] [CrossRef]

- Antioco, M.; Kleijnen, M. Consumer adoption of technological innovations: Effects of psychological and functional barriers in a lack of content versus a presence of content situation. Eur. J. Mark. 2010, 44, 1700–1724. [Google Scholar] [CrossRef]

- Schweitzer, N.; Gollnhofer, J.F.; de Bellis, E. Consumer Perceptions of Autonomous Shopping Systems. 2019. Available online: https://www.alexandria.unisg.ch/261036/ (accessed on 28 July 2020).

- Jörling, M.; Böhm, R.; Paluch, S. Service robots: Drivers of perceived responsibility for service outcomes. J. Serv. Res. 2019, 22, 404–420. [Google Scholar] [CrossRef]

- Lauter, J.; Branchereau, S.; Herzog, W.; Bugaj, T.J.; Nikendei, C. Tutor-led teaching of procedural skills in the skills lab: Complexity, relevance and teaching competence from the medical teacher, tutor and student perspective. Z. Evidenz Fortbild. Qual. Gesundh. 2017, 122, 54–60. [Google Scholar] [CrossRef]

- Andreinald, D.; Prayoga, S.R.; Simorangkir, E.N. Effect of work experience, competence, indepedence, accountability, complexity in audit quality: Empirical study in public accountant office of medan city. J. Res. Bus. Econ. Educ. 2020, 2, 273–282. [Google Scholar]

- Garretson, J.A.; Clow, K.E. The influence of coupon face value on service quality expectations, risk perceptions and purchase intentions in the dental industry. J. Serv. Mark. 1999, 13, 59–72. [Google Scholar] [CrossRef]

- Nguyen, N.; Leclerc, A. The effect of service employees’ competence on financial institutions’ image: Benevolence as a moderator variable. J. Serv. Mark. 2011, 25, 349–360. [Google Scholar] [CrossRef]

- Kleijnen, M.; Lee, N.; Wetzels, M. An exploration of consumer resistance to innovation and its antecedents. J. Econ. Psychol. 2009, 30, 344–357. [Google Scholar] [CrossRef]

- Leung, L.S.K.; Matanda, M.J. The impact of basic human needs on the use of retailing self-service technologies: A study of self-determination theory. J. Retail. Consum. Serv. 2013, 20, 549–559. [Google Scholar] [CrossRef]

- Higgins, E.T.; Spiegel, S. Promotion and prevention strategies for self-regulation: A motivated cognition perspective. In Handbook of Self-Regulation: Research, Theory, and Applications; Vohs, K.D., Baumeister, R.F., Eds.; Guilford Publications: New York, NY, USA, 2016; pp. 171–187. [Google Scholar]

- Kim, J.; Lee, H.; Lee, J. Smartphone preferences and brand loyalty: A discrete choice model reflecting the reference point and peer effect. J. Retail. Consum. Serv. 2020, 52, 101907. [Google Scholar] [CrossRef]

- Peter, J.P.; Tarpey Sr., L.X. A comparative analysis of three consumer decision strategies. J. Consum. Res. 1975, 2, 29–37. [Google Scholar] [CrossRef]

- Deci, E.L.; Ryan, R.M. Intrinsic Motivation and Self-Determination in Human Behavior; Springer: New York, NY, USA, 1985. [Google Scholar]

- Valaei, N. Organizational structure, sense making activities and SMEs’ competitiveness: An application of confirmatory tetrad analysis-partial least squares (CTA-PLS). VINE J. Inf. Knowl. Manag. Syst. 2017, 47, 16–41. [Google Scholar] [CrossRef]

- Podsakoff, P.; MacKenzie, S.; Lee, J.-Y.; Podsakoff, N. Common method biases in behavioral research: A critical review of the literature and recommended remedies. J. Appl. Psychol. 2003, 88, 879–903. [Google Scholar] [CrossRef]

- Harman, H.H. Modern Factor Analysis; University of Chicago Press: Chicago, IL, USA, 1976. [Google Scholar]

- Rezvani, A.; Khosravi, P.; Dong, L. Motivating users toward continued usage of information systems: Self-determination theory perspective. Comput. Hum. Behav. 2017, 76, 263–275. [Google Scholar] [CrossRef]

- Laukkanen, T.; Sinkkonen, S.; Kivijärvi, M.; Laukkanen, P. Innovation resistance among mature consumers. J. Consum. Mark. 2007, 24, 419–427. [Google Scholar] [CrossRef]

- Fagan, M.H.; Neill, S.; Wooldridge, B.R. Exploring the intention to use computers: An empirical investigation of the role of intrinsic motivation, extrinsic motivation, and perceived ease of use. J. Comput. Inf. Syst. 2008, 48, 31–37. [Google Scholar] [CrossRef]

- Nunnally, J.C. Psychometric Theory; McGraw-Hill: New York, NY, USA, 1967. [Google Scholar]

- George, D.; Mallery, M. Using SPSS for Windows Step by Step: A Simple Guide and Reference, 7th ed.; Allyn & Bacon: Boston, MA, USA, 2003. [Google Scholar]

- Cohen, J. Statistical Power Analysis for the Behavioral Sciences, 2nd ed.; Lawrence Erlbaum Associates: Hillsdale, NJ, USA, 1988. [Google Scholar]

- Hair, J.F., Jr.; Hult, G.T.M.; Ringle, C.; Sarstedt, M. A Primer on Partial Least Squares Structural Equation Modeling (PLS-SEM), 2nd ed.; Sage Publications: Thousand Oaks, CA, USA, 2016. [Google Scholar]

- Fornell, C.; Larcker, D.F. Evaluating structural equation models with unobservable variables and measurement error. J. Mark. Res. 1981, 18, 39–50. [Google Scholar] [CrossRef]

- Teo, T.S.H.; Srivastava, S.C.; Jiang, L. Trust and electronic government success: An empirical study. J. Manag. Inf. Syst. 2008, 25, 99–132. [Google Scholar] [CrossRef]

- Henseler, J.; Ringle, C.M.; Sarstedt, M. A new criterion for assessing discriminant validity in variance-based structural equation modeling. J. Acad. Mark. Sci. 2015, 43, 115–135. [Google Scholar] [CrossRef] [Green Version]

- Ullman, J.B.; Bentler, P.M. Structural Equation Modeling. In Using Multivariate Statistics, 2nd ed.; Tabachnick, B.G., Fidell, L.S., Eds.; Allyn and Bacon: Needham Heights, MA, USA, 2001; pp. 653–771. [Google Scholar]

Figure 1.

The proposed research model.

Figure 2.

Hypothesized Model.

{kind=link}

{kind=link}

Table 1.

Demographics of the respondents.

| Demographics | Frequency | Percentage |

|---|---|---|

| Gender | ||

| Male | 198 | 56.9 |

| Female | 150 | 43.1 |

| Age | ||

| Under 19 years old | 56 | 16.1 |

| 21–30 years old | 268 | 77.0 |

| 31–40 years old | 24 | 6.9 |

| Education | ||

| Senior High School | 23 | 6.6 |

| Junior College/College | 214 | 61.5 |

| Graduate | 111 | 31.9 |

| Length of time using mobile payments | ||

| 1–5 years | 258 | 74.1 |

| 6–10 years | 89 | 25.6 |

| Above 11 years | 1 | 0.3 |

Table 2.

Validity and Reliability of Latent Constructs.

| Constructs | Item | Item Loading | 𝛒A | AVE | CR | Cronbach’s Alpha |

|---|---|---|---|---|---|---|

| Usage Intention | UI 1 | 0.944 | 0.927 | 0.867 | 0.951 | 0.923 |

| UI 2 | 0.947 | |||||

| UI 3 | 0.901 | |||||

| Competence | Co1 | 0.814 | 0.823 | 0.642 | 0.878 | 0.816 |

| Co 2 | 0.783 | |||||

| Co 3 | 0.803 | |||||

| Co 4 | 0.806 | |||||

| Image Barrier | Ib 1 | 0.887 | 0.758 | 0.803 | 0.891 | 0.755 |

| Ib 2 | 0.904 | |||||

| Relatedness | Re1 | 0.841 | 0.790 | 0.701 | 0.876 | 0.787 |

| Re 2 | 0.826 | |||||

| Re 3 | 0.844 | |||||

| Autonomy | Auto 1 | 0.781 | 0.844 | 0.615 | 0.889 | 0.844 |

| Auto 2 | 0.792 | |||||

| Auto 3 | 0.781 | |||||

| Auto 4 | 0.793 | |||||

| Auto 5 | 0.774 | |||||

| Complexity Barrier | Cb 1 | 0.774 | 0.782 | 0.669 | 0.858 | 0.756 |

| Cb 2 | 0.819 | |||||

| Cb3 | 0.858 | |||||

| Risk Barrier | Rb1 | 0.830 | 0.843 | 0.758 | 0.904 | 0.840 |

| Rb 2 | 0.896 | |||||

| Rb 3 | 0.884 |

Note: Average variance extracted (AVE) (>0.5); Composite reliability (CR) (>0.7); Cronbach’s Alpha (>0.7).

Table 3.

Fornell Larcker Criterion.

| Construct | Usage Intention | Competence | Image Barrier | Relatedness | Autonomy | Complexity Barrier | Risk Barrier |

|---|---|---|---|---|---|---|---|

| Usage Intention | 0.931 | ||||||

| Competence | 0.149 | 0.802 | |||||

| Image Barrier | −0.178 | −0.193 | 0.896 | ||||

| Relatedness | 0.133 | 0.189 | −0.290 | 0.837 | |||

| Autonomy | 0.157 | 0.028 | −0.212 | 0.340 | 0.784 | ||

| Complexity Barrier | −0.149 | −0.123 | 0.095 | −0.170 | −0.249 | 0.818 | |

| Risk Barrier | −0.117 | −0.008 | 0.234 | −0.403 | −0.682 | 0.222 | 0.870 |

Note: The bold diagonal figures represent the square root of the AVE of each variable, whereas the off-diagonal figures represent variable’s correlations.

Table 4.

Cross-loading.

| Construct | Using Intention | Competence | Image Barrier | Relatedness | Autonomy | Complexity Barrier | Risk Barrier |

|---|---|---|---|---|---|---|---|

| Rb 1 | −0.139 | −0.201 | 0.887 | −0.253 | −0.156 | 0.079 | 0.189 |

| Rb 2 | −0.178 | −0.147 | 0.904 | −0.266 | −0.222 | 0.092 | 0.229 |

| Cb 1 | −0.103 | −0.152 | 0.032 | −0.076 | −0.153 | 0.774 | 0.168 |

| Cb2 | −0.155 | −0.043 | 0.076 | −0.083 | −0.192 | 0.819 | 0.155 |

| Cb3 | −0.111 | −0.110 | 0.113 | −0.227 | −0.250 | 0.858 | 0.214 |

| Rb1 | −0.116 | −0.056 | 0.201 | −0.336 | −0.561 | 0.194 | 0.830 |

| Rb2 | −0.078 | 0.008 | 0.192 | −0.353 | −0.629 | 0.191 | 0.896 |

| Rb3 | −0.115 | 0.025 | 0.219 | −0.363 | −0.590 | 0.195 | 0.884 |

| Co 1 | 0.111 | 0.143 | −0.285 | 0.841 | 0.314 | −0.134 | −0.348 |

| Co 2 | 0.076 | 0.171 | −0.214 | 0.826 | 0.260 | −0.130 | −0.333 |

| Co 3 | 0.146 | 0.162 | −0.224 | 0.844 | 0.277 | −0.163 | −0.331 |

| Auto 1 | 0.162 | 0.025 | −0.127 | 0.270 | 0.781 | −0.182 | −0.533 |

| Auto 2 | 0.135 | −0.010 | −0.148 | 0.282 | 0.792 | −0.183 | −0.574 |

| Auto 3 | 0.069 | 0.018 | −0.200 | 0.216 | 0.781 | −0.201 | −0.491 |

| Auto 4 | 0.110 | 0.012 | −0.183 | 0.288 | 0.793 | −0.202 | −0.531 |

| Auto 5 | 0.138 | 0.064 | −0.174 | 0.275 | 0.774 | −0.207 | −0.542 |

| Co 1 | 0.154 | 0.814 | −0.155 | 0.125 | 0.002 | −0.110 | 0.028 |

| Co 2 | 0.149 | 0.783 | −0.133 | 0.133 | 0.045 | −0.054 | 0.006 |

| Co 3 | 0.059 | 0.803 | −0.170 | 0.183 | 0.042 | −0.109 | −0.044 |

| Co 4 | 0.128 | 0.806 | −0.155 | 0.158 | 0.004 | −0.111 | −0.007 |

| UI 1 | 0.944 | 0.123 | −0.154 | 0.134 | 0.137 | −0.135 | −0.110 |

| UI 2 | 0.947 | 0.149 | −0.166 | 0.122 | 0.142 | −0.159 | −0.123 |

| UI 3 | 0.901 | 0.143 | −0.177 | 0.116 | 0.161 | −0.119 | −0.094 |

Note: Bold values are loadings for items, which are above the recommended value of 0.5.

Table 5.

Heterotrait–Monotrait Ratio.

| Construct | Usage Intention | Competence | Image Barrier | Relatedness | Autonomy | Risk Barrier |

|---|---|---|---|---|---|---|

| Usage Intention | 0.176 | |||||

| Competence | 0.212 | 0.245 | ||||

| Image Barrier | 0.156 | 0.233 | 0.373 | |||

| Relatedness | 0.179 | 0.157 | 0.119 | 0.415 | ||

| Autonomy | 0.178 | 0.057 | 0.264 | 0.204 | 0.303 | |

| Risk Barrier | 0.124 | 0.052 | 0.294 | 0.495 | 0.809 | 0.274 |

Note: The criterion for Heterotrait–Monotrait ratio is below 0.90.

Table 6.

Overall Model Fit.

| Statistical Indicator | Structural Model | Measurement Model |

|---|---|---|

| Standardized Root Mean Square Residual (SRMR) | 0.05 | 0.055 |

| d_ULS | 0.698 | 0.830 |

| d_G1 | 0.396 | 0.402 |

| Chi-Square | 715.544 | 720.679 |

| Normed Fit Index (NFI) | 0.806 | 0.804 |

Table 7.

Summary of results.

| Hypothesis | Path Coefficient | Standard Deviation | T-Value | p-Values | Decision | |

|---|---|---|---|---|---|---|

| H1 | Autonomy > Complexity Barrier | −0.220 | 0.053 | 4.136 | 0.000 | Supported. |

| H2 | Autonomy > Image Barrier | −0.134 | 0.057 | 2.363 | 0.018 | Supported. |

| H3 | Autonomy > Risk Barrier | −0.614 | 0.056 | 10.983 | 0.000 | Supported. |

| H4 | Competence > Complexity Barrier | −0.103 | 0.053 | 1.929 | 0.054 | Not Supported. |

| H5 | Competence > Image Barrier | −0.149 | 0.051 | 2.919 | 0.004 | Supported. |

| H6 | Competence > Risk Barrier | 0.048 | 0.036 | 1.339 | 0.181 | Not Supported. |

| H7 | Relatedness > Complexity Barrier | −0.076 | 0.060 | 1.271 | 0.204 | Not Supported. |

| H8 | Relatedness > Image Barrier | −0.216 | 0.060 | 3.594 | 0.000 | Supported. |

| H9 | Relatedness > Risk Barrier | −0.203 | 0.055 | 3.689 | 0.000 | Supported. |

| H10 | Complexity Barrier > Usage Intention | −0.122 | 0.053 | 2.305 | 0.021 | Supported. |

| H11 | Image Barrier > Usage Intention | −0.154 | 0.056 | 2.764 | 0.006 | Supported. |

| H12 | Risk Barrier > Usage Intention | −0.054 | 0.044 | 1.229 | 0.219 | Not Supported. |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Chung, K.C.; Liang, S.W.-J. Understanding Factors Affecting Innovation Resistance of Mobile Payments in Taiwan: An Integrative Perspective. Mathematics 2020, 8, 1841. https://doi.org/10.3390/math8101841

AMA Style

Chung KC, Liang SW-J. Understanding Factors Affecting Innovation Resistance of Mobile Payments in Taiwan: An Integrative Perspective. Mathematics. 2020; 8(10):1841. https://doi.org/10.3390/math8101841

Chicago/Turabian StyleChung, Kuo Cheng, and Silvia Wan-Ju Liang. 2020. "Understanding Factors Affecting Innovation Resistance of Mobile Payments in Taiwan: An Integrative Perspective" Mathematics 8, no. 10: 1841. https://doi.org/10.3390/math8101841

Note that from the first issue of 2016, this journal uses article numbers instead of page numbers. See further details here.