Abstract

We construct a new test for correlation matrix break based on the self-normalization method. The self-normalization test has practical advantage over the existing test: easy and stable implementation; not having the singularity issue and the bandwidth selection issue of the existing test; remedying size distortion problem of the existing test under (near) singularity, serial dependence, conditional heteroscedasticity or unconditional heteroscedasticity. This advantage is demonstrated experimentally by a Monte-Carlo simulation and theoretically by showing no need for estimation of complicated covariance matrix of the sample correlations. We establish the asymptotic null distribution and consistency of the self-normalization test. We apply the correlation matrix break tests to the stock log returns of the companies of 10 largest weight of the NASDAQ 100 index and to five volatility indexes for options on individual equities.

Similar content being viewed by others

1 Introduction

Correlation coefficient is a standard statistical measure for linear dependency among random variables. Correlation analysis for time series data is reliable only for the data having no change in correlation over time. However, constancy of the correlation over time is sometimes broken in practice. For example, many studies revealed that the correlations of financial asset returns have changes in times of financial or economic events showing stronger correlation in the period of global financial crisis. Hence, several studies are conducted for testing constancy of correlation coefficient.

Wied et al. (2012), Galeano and Wied (2014) and Choi and Shin (2019a, b) developed break tests for correlation coefficient, which are applied to the global minimum-variance portfolios by Wied et al. (2013), to identifying the impact of financialization on the relation between commodities and stocks by Adams and Gluck (2015), to forecasting value-at-risk of financial portfolio by Berens et al. (2015) and to others by many others. Wied (2017) constructed a CUSUM-type test, \(W_T\) say, with bootstrap variance matrix estimator to detect change in correlation matrix, which is applied to financial or economic data sets by Berens et al. (2015), Posch et al. (2019) and others.

However, the test \(W_T\) of Wied (2017) has several non-ignorable weaknesses some of which were already discussed by Posch et al. (2019), Wied (2017), Demetrescu and Wied (2019) and Duan and Wied (2018). When the number P of variables is not small relative to the time series dimension T of data, \(W_T\) is unstable having over-size for large P due to (near) singularity of variance matrix estimator as pointed out by Wied (2017). Moreover, for moderate P, \(W_T\) tends to be under-sized and have low power as discussed by Posch et al. (2019). The size problem of \(W_T\) will be demonstrated in the Monte-Carlo simulation in Sect. 4.

The test \(W_T\) of Wied (2017) has another size distortion problem for unconditionally heteroscedastic samples. In order to overcome this problem, Demetrescu and Wied (2019) and Duan and Wied (2018) proposed residual-based correlation matrix break test based on the standardized data adjusted for mean and variance breaks. However, the residual-based test detects the change in the correlation matrix for data sets adjusted for mean and variance breaks, not for the original data sets. The other weakness of the test \(W_T\) is that it tends to have over-size under serial dependence and/or conditional heteroscedasticity, and requires block length selection and complicated computation.

We circumvent all these weaknesses of the existing test \(W_T\) of Wied (2017) by applying the self-normalization method proposed by Kiefer et al. (2000), Lobato (2001) and Shao and Zhang (2010). Superior size performance of self-normalization break tests over the usual CUSUM tests has been reported in many studies: Shao and Zhang (2010) for single time series, Le and Wang (2014) for a parameter in the diffusion index model, Choi and Shin (2019b) for correlation break and many others. We define a new correlation matrix break test \(Q_T\) based on self-normalization method. The test \(Q_T\) requires no estimation for complicated covariance matrix of the sample correlations. Thus, \(Q_T\) has no issues related to variance estimation such as unstability or singularity. The test \(Q_T\) implements stably and easily without block length selection and complicate computation. Moreover, \(Q_T\) has better size performance than \(W_T\) for serially correlated, cross-sectionally correlated, conditionally heteroscedastic or unconditionally heteroscedastic data. We however admit that the good size property of \(Q_T\) is achieved at the cost of some power loss. While having reasonable power against non-cancelling single break, it has no power against totally cancelling breaks and against some multiple breaks. An extension of \(Q_T\) is made to have power against multiple break alternatives.

We derive the asymptotic null distribution of the self-normalization test \(Q_T\) which is a function of standard brownian bridge. Consistency of \(Q_T\) is derived under an alternative hypothesis of one break. A Monte-Carlo simulation demonstrates that the existing test \(W_T\) of Wied (2017) has singularity issue in the variance matrix estimation in terms of relative magnitude of P and T which render \(W_T\) to have distorted size for P not small. It also shows over-size of \(W_T\) under serial dependence, conditional heteroscedasticity or unconditional heteroscedasticity. On the other hand, \(Q_T\) shows good size for all cases. The correlation matrix break tests \(Q_T\) and \(W_T\) are applied to two real data sets: the stock log returns of the companies of 10 largest weights of the NASDAQ 100 index and five volatility indexes for options on individual equities.

The remaining of the paper is organized as follows. Sect. 2 defines the self-normalization test for correlation matrix break. Section 3 establishes the asymptotic null distribution and consistency of the self-normalization test. Section 4 provides a finite sample Monte Carlo simulation result. Section 5 gives applications to the real data sets. Section 6 concludes.

2 Self-normalization test

Assume that a sample \(\{X_{it}, ~ i = 1, \cdots , P, ~t = 1, \cdots , T\}\) of P-variable is given. Let \(R_t\) be the correlation matrix whose (i, j)-th element is the correlation coefficient \(\rho _t^{ij}\) of \(X_{it}\) and \(X_{jt}\) at time t. We are interested in a test for constancy of correlation matrix \(R_t\) during the observation period. The null hypothesis of constant correlation matrix is

for constants \(\rho ^{ij}_0\) against the alternative hypothesis

and for some correlation break time \(t_0 \in \{1, \cdots , T-1\}\). For a \(P\times P\) symmetric correlation matrix \(R = (\rho ^{ij})\), let vecho(R) = \((\rho ^{12}, \rho ^{13}, \cdots , \rho ^{1P}, \rho ^{23}, \cdots , \rho ^{(P-1)P})^T\) whose elements are the same as those of \(vech(R) = (1, \rho ^{12}, \rho ^{13}, \cdots , \rho ^{1P}, 1, \rho ^{23}, \cdots , \rho ^{(P-1)P}, 1)^T\) keeping only off-diagonal elements of R. Wied (2017) proposed a correlation matrix break test as given by

where \(\tau _T(z) = [2+z(T-2)], z \in [0,1]\), \(||\cdot ||_1\) is the \(L_1\)-norm and \(vecho(\hat{R}_{l,k}) = (\hat{\rho }_{l,k}^{12}, \hat{\rho }_{l,k}^{13}, \cdots , \hat{\rho }_{l,k}^{1P}, \hat{\rho }^{23}_{l,k},\) \(\cdots , \hat{\rho }_{l,k}^{2P}, \cdots , \hat{\rho }_{l,k}^{(P-1)P})^T\), \(\hat{\rho }_{l,k}^{ij}\) is the sample correlation estimated from the the paired sample \(\{(X_{it}, X_{jt}),~ t = l, l+1, \cdots , k\}\). \(\hat{E}\) is a consistent estimator of the \(\frac{P(P-1)}{2} \times \frac{P(P-1)}{2}\) long-run covariance matrix E of \(\sqrt{T} vecho(\hat{R}_{1,T})\). The test \(W_T\) has the asymptotic null distribution \(\sup _{0\le s\le 1} ||B_0^{\frac{P(P-1)}{2}}(s)||_1, \) where \(B_0^{N}(\cdot )\) is an N-dimensional standard brownian bridge. Note that the asymptotic critical values of the test \(W_T\) depend on P.

Wied (2017) noted that explicit expression for E is very complicated, which takes nearly one-page even for \(P = 2\) (Wied et al. 2012, p.580). Therefore, Wied (2017) implemented \(\hat{E}\) with a block bootstrap method. The test \(W_T\) has limitations in practical use owing to singularity problem of \(\hat{E}\) for P not small relative to T and over-size problem under serial dependence, conditional heteroscedasticity or unconditional heteroscedasticity as will be shown in the Monte-Carlo simulation in Sect. 4. The block bootstrap estimation for E requires block length selection and complicated computation. We discuss these issues in more detail in Remarks 3.5, 3.6.

All these limitations of the existing test \(W_T\) are remedied by a new test \(Q_T\) based on the self-normalization method proposed by Kiefer et al. (2000), Lobato (2001) and Shao and Zhang (2010). The self-normalization test \(Q_T\) is

The denominator \(Q_{2T}(z)\) is composed of two terms, which is designed for a single break alternative as discussed in Shao and Zhang (2010, p.1230). Therefore, our test \(Q_T\) is also designed for single break alternative. A multiple break extension is discussed in Remark 3.9. The difference \( \Sigma _{1 \le i < j \le P}(\hat{\rho }_{1,[Tz]}^{ij} - \hat{\rho }_{[Tz]+1,T}^{ij})\) is self-normalized by \(Q_{2T}(z)/z(1-z)\) without complicate covariance estimation of \(\sqrt{T}vecho(\hat{R}_{1,T})\) such as the bootstrap covariance estimation or the kernel long-run variance estimation. Accordingly, \(Q_T\) has merits over \(W_T\) by getting away from the singularity of estimated covariance matrix for all P. Asymptotic critical values of \(Q_T\) are free from P as will be shown in Theorem 3.3 below.

3 Asymptotic null distribution and consistency

We establish the asymptotic null distribution, consistency and asymptotic local power of the self-normalization test \(Q_T\). The former is derived under the assumptions (A1)-(A4) of Wied (2017).

-

(A1)

For \(U_t = (X_{1t}^2, \cdots , X_{Pt}^2, X_{1t}, \cdots , X_{Pt}, X_{1t}X_{2t}, X_{1t}X_{3t}, \cdots , X_{P-1,t}X_{Pt})^T\) and \(S_j = \sum _{t=1}^j (U_t - E[U_t]) = \sum _{t=1}^j \tilde{U}_t\), we have \(\lim _{m\rightarrow \infty } E[\frac{1}{m}S_m S_m^T] = D_1\), where \(D_1\) is a finite \((2P+\frac{P(P-1)}{2}) \times (2P + \frac{P(P-1)}{2})\) matrix.

-

(A2)

For some \(r>2\), the r-th absolute moments of the components of \(\tilde{U}_t\) are uniformly bounded, that means, \(\sup _{t \in Z} E|| \tilde{U}_t ||_r < \infty \).

-

(A3)

For r from Assumption (A2), the vector \((X_{1t}, \cdots , X_{Pt})^T\) is \(L_2\)-NED (near-epoch dependent) with size \(-(r-1)/(r-2)\) and constants \(c_t\), \(t\in Z\), on a sequence \(V_t\), \(t\in Z\), which is \(\alpha \)-mixing of size \(\phi ^* = -r/(r-2)\), i.e.,

$$\begin{aligned} ||(X_{1t}, \cdots , X_{Pt}) - E(X_{1t}, \cdots , X_{Pt}) | \sigma (V_{t-l}, \cdots , V_{t+l})||_2 \le c_t v_l \end{aligned}$$with \(\lim _{l \rightarrow \infty } v_l = 0\). The constants \(c_t\), \(t \in Z\) fulfill \(c_t \le 2 ||\tilde{U}_t ||_2\) with \(\tilde{U}_t\) from Assumption (A1).

-

(A4)

\((X_{1t}, \cdots , X_{Pt}), t\in Z,\) has constant expectation and variance, that means, \(E[X_{it}], i = 1, \cdots , P\) and \(0<E[X_{it}^2], 1 \le i \le P\), do not dependent on t.

Assumption (A1) is more general than that of Wied (2017) in which \(D_1\) is assumed to be positive definite for the long-run variance matrix E of \(vecho(\hat{R}_{1,T})\). Since our method does not require estimation of E, positive definiteness of \(D_1\) is not required. The remaining conditions (A2)-(A4) are the same as those of Wied (2017). The \(L_2\)-NED assumption (A3) makes it possible to establish the asymptotic null distribution of the self-normalization test under weak dependence such as the GARCH-type conditional heteroscedasticity and ARMA-type serial correlation.

Lemma 3.1

(Wied 2017) Under \(H_0\), Assumptions (A1)-(A4), and fixed P, as \(T\rightarrow \infty \),

Lemma 3.2

Assume the assumptions of Lemma 3.1 hold and \(\omega \ne 0\). Then, under \(H_0\), for fixed P, as \(T\rightarrow \infty \),

where \(B_0(\cdot ) = B_0^1(\cdot )\) is a one-dimensional standard brownian bridge and \(\omega ^2 = J^TE J\), \(J=(1, \cdots , 1)^T\) is a \(\frac{P(P-1)}{2}\times 1\) vector.

The asymptotic null distribution of \(Q_T\) is established by combining Lemma 3.2 and the continuous mapping theorem.

Theorem 3.3

Assume the assumptions of Lemma 3.2 hold and \(\omega \ne 0\). Then, under \(H_0\), for fixed P, as \(T\rightarrow \infty \),

Now, \(Q_T\) rejects \(H_0\) at level \(\alpha \in (0,1)\) if \(Q_T>q_\alpha \), where \(q_\alpha \) is the right \(\alpha \)-quantile of Q available in Shao and Zhang (2010) which is free from P. Examples are \(q_{0.01} = 68.6\), \(q_{0.05} = 40.1\), \(q_{0.1} = 29.6\).

Remark 3.4

(Robust size of \(Q_T\)) Note that all the data features such as the data dimension P, cross-sectional dependence, serial dependence and conditional heteroscedasticity are reflected in the limiting distribution \(\omega B_0(z)\) of \(Q_T(z)\) by a single multiplicative constant \(\omega \) which is canceled out in the limiting null distribution of \(Q_T = Q_{1T}/Q_{2T}\) as stated in Theorem 3.3. Thus, \(Q_T\) is free from the issues for the test \(W_T\) to have size distortion: singularity problem for large P, serial dependence, cross-sectional correlation, or conditional heteroscedasticity. Unlike \(W_T\), the test \(Q_T\) has good size under such size-related issues for \(W_T\), as will be demonstrated in Sect. 4. If \(Q_T\) would be based on \(\sum _{1 \le i < j \le P} |\hat{\rho }^{ij}_{1,[Tz]} - \hat{\rho }^{ij}_{[Tz]+1,T}|\) or \( \sum _{1 \le i < j \le P} (\hat{\rho }^{ij}_{1,[Tz]} - \hat{\rho }^{ij}_{[Tz]+1,T})^2\) for better power consideration instead of \(\sum _{1 \le i < j \le P} (\hat{\rho }^{ij}_{1,[Tz]} - \hat{\rho }^{ij}_{[Tz]+1,T})\), then nuisance parameters in the limiting null distributions of \(Q_{1T}\) and \(Q_{2T}\) should not be cancelled out in the limit of \(Q_T = Q_{1T}/Q_{2T}\). Therefore, the resulting test would have no good size any more.

Remark 3.5

(Stability of \(Q_T\) for all P In the existing test \(W_T\), the difference \((vecho(\hat{R}_{1,[Tz]}) - vecho(\hat{R}_{1,T}))\) is normalized by the \(\frac{P(P-1)}{2}\times \frac{P(P-1)}{2}\) matrix \(\hat{E}\), the long-run variance matrix estimator of \(\sqrt{T}vecho(\hat{R}_{1,T})\). The test \(W_T\) is feasible only if \(\hat{E}\) is nonsingular. However, if \(P(P-1)/2\) is not sufficiently smaller than T, \(\hat{E}\) is (near) singular. Near-singular \(\hat{E}\) induces severe size distortion problem for \(W_T\). Moreover, if \(P(P-1)/2\) is larger than T, the estimator \(\hat{E}\) becomes singular, which makes \(W_T\) be infeasible to implement. Thus, \(W_T\) has a singularity issue for \(\hat{E}\) in terms of relative magnitudes of P and T. Note that even for singular E, the result of Theorem 3.3 holds good provided \(\omega ^2 = J^TEJ \ne 0\). Therefore, for finite T, even for singular \(\hat{E}\) arising from large P, the distribution of \(Q_T\) would be close to Q provided \(J^T \hat{E} J\) is not close to 0. Hence, the test \(Q_T\), requiring no variance estimation, is implemented stably for all (P, T), showing good size, as will be revealed in Monte Carlo simulation in Sect. 4.

Remark 3.6

(No need for covariance matrix estimator) Wied (2017) implemented \(W_T\) with the variance estimator \(\hat{E}\) estimated by the block bootstrap method. Even though the block bootstrap estimator \(\hat{E}\) addresses the serial dependence, it is not precise for covariance matrix for finite samples with serial dependence and/or conditional heteroscedasticity, see Goncalves and White (2005), which causes oversize problems of tests based on it. This point will be demonstrated in the Monte-Carlo simulation in Sect. 4. Also, the block bootstrap covariance matrix estimator \(\hat{E}\) requires block length selection. However, the optimal block length for \(\hat{E}\) is not simple to specify. Shao (2010) discussed that, in panel data sets, the block bootstrap covariance estimator is very sensitive to the block length. Thus, it is difficult to select block length giving precise variance estimator in all cases. On the other hand, \(Q_T\) is free from these issues because of no need for variance estimation, which makes \(Q_T\) have good size, as will be shown in Sect. 4.

Consistency of \(Q_T\) is established under an alternative hypothesis where the correlation matrix is changed by a change of a covariance of \(X_{it}\) and \(X_{jt}\) for some \(i,j\in \{1,\cdots ,P\}\) at an unknown time \(t_0\). Let \(I(t>t_0) = 1\) for \(t>t_0\) and 0 otherwise.

-

(A5)

For some \(\Delta _{ij}\) with \(\Sigma _{1 \le i < j \le P} \Delta _{ij}\ne 0\) and \(t_0\), \(E[X_{it}X_{jt}] = m_{X_i X_j} + \Delta _{ij} I(t>t_0)\).

Theorem 3.7

Under the alternative of (A5) and Assumptions (A1)-(A4), \(\omega \ne 0\), for \(t_0/T \rightarrow z_0 \in (0,1)\) and fixed P, as \(T\rightarrow \infty \), we have

Remark 3.8

(Non-cancelling break condition) The condition \(\sum _{1 \le i< j \le P} \Delta _{ij} \ne 0\) in (A5) is that the breaks \(\Delta _{ij}\) in \(\rho _t^{ij}\) are not cancelled in their sum. The good size property of \(Q_T\) over \(W_T\) as discussed in Remarks 3.4, 3.5, 3.6 is obtained by sacrificing power against total cancelling break \(\sum _{1 \le i<j \le P}\Delta _{ij} =0\) for which \(Q_T\) has no power but \(W_T\) has power. See more discussion in Remark 3.11. In practice, however, total cancelling breaks may be rare. For example, letting \(R_{01}\) and \(R_{02}\) be the sample correlation matrices of \(\{X_{it}, i = 1, \cdots , P, ~t = 1, \cdots , T/2\}\) and \(\{X_{it}, i = 1, \cdots , P, ~t =T/2+ 1, \cdots , T\}\) of log returns \(\{X_t\}\), respectively, of the first \(P = 4, 10\) largest companies in weight for the NASDAQ index analyzed in Sect. 5; for \(P = 4\), (minimum, maximum) values of all elements \(\Delta _{ij}\) of difference \(R_{02} - R_{01}\) are (0.12, 0.25) indicating non-cancelling breaks in that all elements \(\Delta _{ij}\) of \(R_{02} - R_{01}\) are positive and, for \(P = 10\), they are (−0.16, 0.29) indicating some but not total cancelling breaks. Powers of \(Q_T\) and \(W_T\) under these breaks are investigated in Sect. 4.

Remark 3.9

(Multiple breaks) The proposed test \(Q_T\) is designed for a single break alternative. We apply the subsample method for multiple break alternatives developed by Choi and Shin (2020) whose spirit is similar to the scan method of Yau and Zhao (2016) in which a subsample of moving window is used for detecting one break for each subsample. For the subsample method, the sample size T is split into L subsamples corresponding to \(A = \{t:t \in ( \frac{(l-1)T}{L} , \frac{lT}{L}],~l = 1,\cdots ,L\}\) and \((L-1)\) subsamples corresponding to \(B = \{t:t \in ( \frac{T}{2L} + \frac{(l-1)T}{L} , \frac{T}{2L} +\frac{lT}{L}], l=1, \cdots , L-1\}\) of size T/L from which L subsample break tests \(Q_{lT}^A,~l = 1, \cdots ,L\) and \((L-1)\) subsample tests \(Q_{lT}^B,~ l = 1,\cdots ,L-1\) are computed, respectively. The set of samples corresponding to \(A \cup B\) is similar to a set of moving window samples. For example, if \(L = 4\), then \(A \cup B = \{ (0,\frac{T}{4}], (\frac{T}{8}, \frac{3T}{8}], (\frac{T}{4}, \frac{3T}{4}], \cdots , (\frac{3T}{4}, T]\}\). We scan breaks for each subsample in \(A \cup B\). It is easy to show that \(Q_{lT}^A,~l = 1,\cdots ,L\) are asymptotically independent having asymptotic null distribution Q and so are \(Q_{lT}^B\), \(l = 1, \cdots , L-1\). Now, the subsample extension of \(Q_T\) is \(Q_T^S = \max \{\max _{1 \le l \le L} Q_{lT}^A,~ \max _{1 \le l \le L-1} Q_{lT}^B\}\). The test \(Q_T^S\) rejects \(H_0\) at level \(\alpha \) if \(Q_T^S>q_{L\frac{\alpha }{2}}\), where \(q_{L \frac{\alpha }{2}}\) is the \(\frac{\alpha }{2}\)-quantile of \(\max _{1 \le l \le L} Q_{(l)}\) and \(Q_{(l)},~ l= 1, \cdots , L\) are iid from Q, the weak limit of \(Q_T\). According to Theorem 2.1 of Choi and Shin (2020), \(Q_T^S\) has asymptotically valid level. It has power against multiple breaks as will be illustrated in a simulation in Sect. 4. According to Choi and Shin (2020), Bonferroni-type adjusted p-values of \(Q_T^S= q\), \(Q_{lT}^A = q\) or \(Q_{lT}^B = q\) can be approximated by \(2P[\max _{1\le l \le L}Q_{(l)}>q]\). If T/L is not large, one may safely assume at most one break during the period of a subsample. This subsample method is illustrated in the example in Sect. 5.

We next derive the limiting distribution of the self-normalization test under the local alternatives of

-

(A6)

\(E[X_{it}X_{jt}] = m_{X_i X_j} +\frac{ \Delta _{ij}}{\sqrt{T}} I(t>t_0)\).

Theorem 3.10

Under the same conditions of Theorem 3.7 with (A6) instead of (A5), for \(T\rightarrow \infty \),

where \(b_1(z) = z(1-z)(\frac{1}{z} \int _0^zI(u>z_0) du -\frac{1}{1-z} \int _z^1 I(u>z_0)du )\), \(b_2(s) = (\int _0^s I(u>z_0)du - \frac{s}{z}\int _0^z I(u>z_0)du)\), \(b_3(s) = (\int _s^1 I(u>z_0)du -\frac{1-s}{1-z}\int _z^1 I(u>z_0)du)\), \(\Delta = \Sigma _{1 \le i < j \le P} \Delta _{ij}\).

Local power of level 0.05 test \(Q_T\) under \(d = \frac{1}{2}, ~\Delta _{ij} = \omega = 1,~ P =4, ~ z_0 = \lim _{T\rightarrow \infty } \frac{t_0}{T}\)

Remark 3.11

(Local power) Assume \(E[X_{it}X_{jt}] = m_{X_iX_j} + \Delta _{ij}/T^d\) for some \(d \ge 0\). By the arguments of proofs of Theorems 3.7, 3.10, we can show that \(P(Q_T>q_\alpha ) \rightarrow 1\) for \(0\le d<\frac{1}{2}\); \(P(Q_T>q_\alpha )\rightarrow \alpha \) for \(d>\frac{1}{2}\). Theorem 3.10 states that the local power of \(Q_T\) under \(d=\frac{1}{2}\) depends on the magnitude of break via \(\Delta \), cross-sectional and/or serial correlations via \(\omega \), and position of break time via \(z_0 = \lim _{T\rightarrow \infty } t_0/T\). Fixing \(\Delta = \omega = 1\), local power \(p(z_0) = P[Q_{Local}>q_{0.05}]\) of level 0.05 test is depicted in Figure 1 for \(z_0 = 0, 0.1, \cdots ,1\) which is computed by approximating B(z) 2000 times by a Monte Carlo simulation \(\frac{1}{\sqrt{T}} \sum _{t=1}^{[Tz]} e_t\), \(e_t\) are iid N(0, 1), \(T = 1000\). It shows \(p(z_0) = P[Q_{Local}>q_{0.05}] >0.05\) for \(0<z_0<1\); \(p(z_0) \rightarrow 0.05\) as \(z_0 \rightarrow 0\) or 1; and \(p(z_0)\) takes maximum at \(z_0 = 1/2\). We may reasonably guess that, under local alternative of (A6) of \(d = 1/2\), local power of level \(\alpha \) test \(Q_T\), i.e. \(P(Q_{Local}>q_\alpha )\), is always greater than \(\alpha \). The order d of deviation \(T^{-d} \Delta \) for \(Q_T\) should satisfy \(d \le \frac{1}{2}\) to detect a break. For cancelling break of \(\Delta = 0\), \(Q_{Local}\) is the same as Q and hence the local power of level \(\alpha \)-test \(Q_T\) becomes \(P(Q_{Local}>q_\alpha ) = P(Q>q_\alpha )=\alpha \). Therefore \(Q_T\) does not have any local power against cancelling break.

4 Monte Carlo simulation

We compare finite sample performances of the proposed self-normalization test \(Q_T\) with the existing test \(W_T\) of Wied (2017). The comparison will show that \(Q_T\) has stabler sizes than \(W_T\) under large P, P larger than T, serial dependence, conditional heteroscedasticity or unconditional heteroscedasticity. The test \(Q_T\) retains size advantage over \(W_T\) when they are applied to GARCH-filtered data. The comparison also shows that \(Q_T\) has reasonable power for a single noncancelling break and for a historic double break but no power for a totally cancelling break of \(\Delta = 0\) and for up-down (or down-up) type double breaks.

For the data generating process (DGP), we consider a vector autoregression of order 1

where \(X_t = (X_{1t}, \cdots , X_{Pt})^T\) and the error \(a_t = (a_{1t}, \cdots , a_{Pt})^T\) has zero mean and covariance matrix \(\Sigma _t = \Xi _t R_t \Xi _t\) with \(\Xi _t = diag(\sigma _{1t}, \cdots , \sigma _{Pt})\) and correlation matrix \(R_t\). Serial independence and dependence are considered by \(\phi = 0,0.8\). We consider homoscedastic and conditionally heteroscedastic errors \(a_t\) given by

\((\alpha _1, \beta _1) = (0,0), (0.1, 0.89)\), where \(e_t = (e_{1t}, \cdots , e_{Pt})^T\) is a vector of independent errors. Unconditional heteroscedasticity is also considered with

under which we check finite sample validities of the tests \(Q_T\) and \(W_T\) for the sample having constant correlation, but having change in the variances. For \(e_{it}\), we consider the standard normal distribution N(0, 1) or the standardized t distribution, \(t_3\), with 3 degrees of freedom, as considered by Wied (2017). The vector \(a_t=\Sigma _t^{1/2}e_t\) with the normal and \(t_3\) errors \(e_{it}\) are generated by “rmvnorm” and “rmvt”, respectively, in the R-package.

Size comparison is made for the correlation matrix \(R_t = R_0\), \(R_0 = \Big ({\begin{matrix} 1 &{} \rho _{0} &{}\cdots &{}\rho _{0}\\ &{} 1 &{} \cdots &{}\rho _{0} \\ &{}&{} \ddots \\ &{}&{}&{}1 \end{matrix}}\Big )\), \(\rho _0 = 0, 0.5\), for all t. Power comparison is also made for the breaks considered by Wied (2017) and for the historical breaks from \(R_t = R_{01}\) to \(R_t = R_{02}\) discussed in Remark 3.8. The comparison is based on 1000 repetitions of the tests \(Q_T\), \(W_T\) with level 5% unless specified otherwise. For \(T= 2000\) and \(P>20\), sizes in Figure 2 are obtained by 100 repetitions because of computing time consideration of \(W_T\). The 5% critical value of \(Q_T\) is \(q_{0.05} = 40.1\) for all \(P = 2, \cdots , 40\). The 5% critical value of the test \(W_T\) is computed as the right \(5 \%\) empirical quantile of 1000 values of \(\sup _{0\le s\le 1} ||B_0^{\frac{P(P-1)}{2}}(s)||_1\) computed from simulated Brownian bridge with \(T = 10000\). The test \(W_T\) of Wied (2017) is constructed with 999 bootstrap samples for the bootstrapping estimator \(\hat{E}\) for which we consider the moving block bootstrap with the block length \(l = T^{1/4}\) used by Wied (2017).

Sizes (%) of the level 5% tests \(Q_T\) and \(W_T\) for P with fixed T. The gray dotted lines are 0% and 5%.

We first investigate size performances of the tests in terms of the data dimension P in Figure 2 and Table 1. Figure 2 displays sizes of \(Q_T\), \(W_T\) for \(P= 2, 4, \cdots , 40\) with fixed \(T = 200, 2000\). We consider the iid DGP with homoscedasticity, \(\phi = 0\), \(\rho _0 = 0\) and normal error. In Figure 2, \(Q_T\) is shown to have good size for all range of P in the figure. On the other hand, \(W_T\) has very unstable size: only up to very small P (4 for \(T = 200\)), \(W_T\) shows acceptable size; next up to some moderate P (16 for \(T = 200\)), \(W_T\) has under-size close to 0%; next up to \(P \le 40\), \(W_T\) reveals severe over-size; and for \(P >40\), \(W_T\) is infeasible to implement. Severe over-size or infeasibility of \(W_T\) for some moderate P (\(P>16\) for \(T=200\)) is a consequence of singularity of \(\hat{E}\) because its dimension \(P(P-1)/2\) is not sufficiently larger than the data dimension T. The under-size problem was discussed by Posch et al. (2019). On the other hand, \(Q_T\) shows good size for all P. These findings imply that the size of \(W_T\) is affected severely by relative magnitude of P and T, but that of \(Q_T\) is not.

Table 1 reports sizes of \(Q_T\) for some pairs (P, T) with \(T\in \{50, 200\}\) and large \(P \in \{50, 200\}\) under which \(W_T\) is infeasible because of singularity problem in \(\hat{E}\). The table reveals that \(Q_T\) has reasonable size and is implemented stably for all (P, T), correlation parameter \(\rho _0\), serial correlation parameter \(\phi \) and conditional heteroscedasticity parameter \((\alpha _1, \beta _1)\) considered here.

In Table 2, we look into sizes of the tests \(Q_T\), \(W_T\) for \((P,T) \in \{4,10\} \times \{200, 2000\}\) in terms of serial dependence, conditional heteroscedasticity or unconditional heteroscedasticity. The 5% critical values of the test \(Q_T\) is 40.1 for both of \(P = 4,10\) and those of \(W_T\) are (4.47, 23.21) for \(P =(4,10)\). From the table, we see that the size of \(Q_T\) is close to the nominal level 5% for all cases. However, the size of \(W_T\) is severely distorted for serially dependent or conditionally heteroscedastic samples. The test \(W_T\) also tends to have non-ignorable over-size for cross-sectionally correlated sample with \(\rho _0 = 0.5\) and small T and tends to have under-size for \(P= 10\) under homoscedasticity. Moreover, \(W_T\) shows uncontrolled sizes substantially greater than 5% under unconditional heteroscedasticity, meaning that \(W_T\) tends to identify changes in the variances as a change in correlation even though there is no change in correlation, see Demetrescu and Wied (2019) and Duan and Wied (2018) for related discussions. The over-size problem of \(W_T\) is severer for \(t_3\) error than for normal error while size of \(Q_T\) is acceptable for \(t_3\) error.

People often test for breaks for GARCH filtered returns, see Demetrescu and Wied (2019) and Duan and Wied (2018). It would be interesting to study performances of the GARCH-filtered tests \(Q_T^*\) and \(W_T^*\) which are values of \(Q_T\) and \(W_T\) computed from the GARCH(1,1)-filtered data \(\{\hat{\epsilon }_{it} = X_{it}/\hat{\sigma }_{it}\}\) instead of \(\{X_{it}\}\), where \(\hat{\sigma }_{it}\) is estimated by fitting (4) using data \(\{X_{it}, t=1,\cdots ,T\}\). Size results for \(\phi =0\) and normal error \(e_{it}\) are reported in Table 3 which are computed under the same setup for Table 2. Even though the GARCH-filtered Wied test \(W_T^*\) has improved size over the original Wied test \(W_T\), it still has size distortion: some over-size under unconditional heteroscedasticity and some under-size under homoscedasticity and under conditional heteroscedasticity. On the other hand, \(Q_T^*\) has good size for all cases considered. Therefore, we can say that the proposed test \(Q_T\) has also better size than the Wied test \(W_T\) when they are applied to GARCH-filtered data.

We next compare powers of the tests \(Q_T\), \(W_T\) for serially independent and homoscedastic normal error under which the sizes of the tests \(Q_T\), \(W_T\) are controlled being close to 5% except for under-size of \(W_T\) for \((P,T) = (10,200)\) as shown in Table 2. A DGP with one break for power study is constructed for model (3) with the correlation matrix \(R_t = R_{01}I(t\le t_0) + R_{02} I(t >t_0)\) having a correlation change at \(t_0 =0.25T, 0.5T\). The correlation matrices \(R_{01}\) and \(R_{02}\) are specified as (i) the values \(R_{01}\) and \(R_{02}\) with equal correlation \(\rho _0 = 0\) and 0.2, respectively, considered by Wied (2017), (ii) the historical values \(R_{01}\) and \(R_{02}\) estimated from the stock log-returns \(\{X_{it}\}\) discussed in Remark 3.8, and (iii) totally cancelling breaks of \(R_{01} = 0\) and \(R_{02}= (\Delta _{ij})\), where \(\Delta _{ij}\) = 0.2 or -0.2 for \(P = 4\) and \(\Delta _{ij} = 0.05\) or -0.05 for \(P = 10\) such that \(\sum _{1 \le i < j \le P} \Delta _{ij} = 0\).

The difference \(R_{01}-R_{02}\) between the historical values \(R_{01}\) and \(R_{02}\).

Figure 3 displays the difference \(R_{01}\) - \(R_{02}\) of historical correlation changes. Among the 45 pairs, 9 pairs are negative and the other pairs are positive saying that some correlations get bigger and the others get smaller after T/2 whose sum is not totally cancelling.

Power values are reported in Table 4. Consider first the Wied break (i) and the historical break (ii). All the tests \(Q_T\), \(W_T\) have increasing power, as T increases from 200 to 2000, indicating consistency of \(Q_T\), \(W_T\) under the alternative hypotheses. The test \(Q_T\) has acceptable power for all DGPs and all (P, T). The test \(W_T\) seems to have worse power than \(Q_T\), especially for \((P=10,T=200)\), which however largely dues to the under-size of \(W_T\) for small T (\(T=200\)) as shown in Table 2. The powers of \(Q_T\), \(W_T\) are higher in the order of \(t_0 = 0.5T\), \(t_0 = 0.25T\), \(t_0 = 0.1T\). For break point near the boundary like \(t_0 = 0.1T\), power of \(Q_T\) is substantially smaller than that for break point near the center, which however increases as T increases. Consider next the total cancelling break (iii). Against the total cancelling break (iii), we see power of \(W_T\) for \(T = 2000\) but no power of \(Q_T\). In addition to the power values for \(P = 4, 10\), we also report acceptable power values \(\{89.4\%, ~99.6\%, ~91.4\%, ~100\%\}\) of \(Q_T\) under the alternative (i) of Wied (2017) with \(\{(P,T) = (50,50),~ (50, 200),~ (200, 50), ~(200, 200)\}\) of large P and \(t_0 = T/2\).

Powers of the tests are further investigated under double breaks. For double breaks, we consider two alternatives of \(R_t = R_{01} I(1 \le t \le \frac{T}{3}) + R_{02}I(\frac{T}{3}<t \le \frac{2T}{3}) +R_{03}I(\frac{2T}{3} < t \le T)\): (i) the values \(R_{01}\), \(R_{02}\), \(R_{03}\) with equal correlation 0.2, 0.7, 0.2, respectively; (ii) the historic values \(R_{01}\), \(R_{02}\), \(R_{03}\) being the sample correlation matrices of the stock return data in Sect. 5 for the periods \((1, \frac{T}{3}]\), \((\frac{T}{3}, \frac{2T}{3}]\), \((\frac{2T}{3},T]\), respectively. For the double break alternatives, the multi-break extension \(Q_T^S\) with \(L = 4\) in Remark 3.9 is also considered. Powers are reported in Table 5. Against the up-down double breaks of (\(0.2\rightarrow 0.7 \rightarrow 0.2\)), \(W_T\) has power, \(Q_T\) has no power, but the extended subsample test \(Q_T^S\) has power. Against the historic double breaks, both \(Q_T\) and \(W_T\) have powers.

From Tables 1-5, we can say that \(Q_T\) is useful in practice. Test \(Q_T\) has better size than \(W_T\) for the samples with not small P or with the main features (the serial dependence, cross-sectional dependence, unconditional heteroscedasticity or conditional heteroscedasticity) apparent in economic or financial data set. The test \(Q_T\) has reasonable power for a single non-cancelling break, and the no-power aspect of \(Q_T\) for up-down (or down-up) type double breaks may be overcame by the subsample analysis of Remark 3.9 as illustrated by good power of \(Q_T^S\).

5 Example

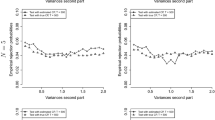

We now see applications of the correlation break tests. We consider the stock log returns of the companies of 10 largest weights of the NASDAQ 100 index as of August 1, 2019, (Microsoft Corp, Apple Inc, Amazon.com Inc, Alphabet Inc, Cisco Systems Inc, Intel Corp, Comcast Corp, PepsiCo Inc, Adobe Inc, Netflix Inc) and five volatility indexes for options on individual equities (Amazon (VXAZN), Apple (VXAPL), Goldman Sachs (VXGS), Google (VXGOG), IBM (VXIBM)). The stock returns (volatility indexes) feature the weak (strong) serial dependence and strong (strong) conditional heteroscedasticity. We discuss the difference between the results of the correlation matrix break tests \(Q_T\) and \(W_T\) for the real data sets in terms of these features. The period of stock returns and volatility indexes is considered as 06/01/2010 - 06/30/2019 (\(T\cong 2000\)). The stock return and volatility index data sets are obtained from the website (https://finance.yahoo.com/) and Chicago Board Options Exchange (CBOE) website (http://www.cboe.com/products/vix-index-volatility/volatility-indexes), respectively.

Table 6 reports test results for the stock return and volatility indexes. The test \(W_T\) is computed from 999 moving block bootstrap samples for the bootstrap covariance matrix estimator \(\hat{E}\). In the table, the statistics \(\hat{\rho }_1^S\), \(\hat{\rho }^C\) and (\(\hat{\alpha }_1\), \(\hat{\beta }_1\)) are the mean of the first order P within-series sample autocorrelations, the mean of \(P(P-1)/2\) values of pairwise cross-sectional sample correlations and the means of the P within-series GARCH parameter estimators, respectively. From the statistics \(\hat{\rho }_1^S\), \(\hat{\rho }^C\) and (\(\hat{\alpha }_1\), \(\hat{\beta }_1\)), we identify that the return data sets have weak serial correlation, substantial cross-sectional correlation and strong conditional heteroscedasticity, and the volatility index data sets have strong serial correlation, strong cross-sectional correlation and strong conditional heteroscedasticity.

In the table, at 5% level, the existing test \(W_T\) tells significant presence of correlation matrix break for both return data set and volatility index data set. On the other hand, the proposed self-normalization test \(Q_T\) tells no correlation matrix break for both data sets. Recall that \(Q_T\) is designed for single break alternative. The non-rejection by \(Q_T\) may be a consequence of more than one break. The subsample test \(Q_T^S\) with \(L = 4\) in Remark 3.9 indicates absence of correlation break for return correlation matrix but presence of it for volatility index correlation matrix.

Since \(T \cong 2000\) spans a long time of 9 years of 109 months, more than one break may be possible, which leads us to consider the subsample scan analysis of Remark 3.9 with \(L=4\) of subsamples of size T/4 corresponding to the subperiods \(A = \{\frac{l-1}{4}T < t \le \frac{l}{4}T,~l = 1,2,3,4\}\) and \(B = \{\frac{T}{8}+\frac{l-1}{4}T \le t < \frac{T}{8} +\frac{l}{4}T,~l = 1,2,3 \}\) from which subsample versions, \(Q_{lT}^A\), \(W_{lT}^A\), \(l = 1, \cdots ,4\) and \(Q_{lT}^B\), \(W_{lT}^B\), \(l = 1, 2,3\) are computed and are tabulated in Table 7. Our test \(Q_{lT}^A, l = 1, \cdots ,4\) and \(Q_{lT}^B\), \(l = 1,2,3\) indicate no break for return correlation matrix for any subsample and significance of volatility index correlation matrix break during \((\frac{T}{8}, \frac{3T}{8}]\) and during \((\frac{3T}{8}, \frac{5T}{8}]\) at 5% level. Note that the former period \((\frac{T}{8}, \frac{3T}{8}]\) contains the time (\(z_0\) = 25 month/ 109 month =0.23) of the end of the European debt crisis (June/2012) and the latter period \((\frac{3T}{8}, \frac{5T}{8}]\) contains the time (\(z_0\) = 61 month/ 109 month = 0.55) of the beginning of the Greek debt crisis (June/2015). Noting further that all the assets are American stocks, the analysis by \(Q_{lT}^A\) and \(Q_{lt}^B\) tells us that the European events induce correlation matrix change for American stock return volatility indexes but not for the American stock returns. On the other hand, the subsample results of \(W_{lT}^A\) and \(W_{lT}^B\) tells us return correlation matrix breaks during (0, T/4], (3/4T, T] and volatility index correlation matrix breaks during (0, T/4], (T/4, 2T/4], (2T/4, 3T/4], (3T/4, T].

6 Conclusion

We have proposed a self-normalization test for testing constancy of correlation matrix. We construct a nuisance parameter free simple asymptotic null distribution of the self-normalization test, which makes it unnecessary to estimate covariance of the sample correlations. Unnecessariness of covariance estimation allows the proposed test to be free from the singularity problem of the existing test of Wied (2017) and to resolve the size distortion of the existing test for samples with not small number of variables, with serial correlation, with non-ignorable cross-section, with conditional heteroscedasticity or with unconditional heteroscedasticity. We demonstrate size and power performances of the self-normalization test in a Monte-Carlo simulation. Applications of the self-normalization test to the stock log returns and volatility indexes are made.

7 Proofs

Proof of Lemma 3.1

The proof is given in Wied (2017, Theorem 1). \(\Box \)

Proof of Lemma 3.2

Observing \(\sum _{1 \le i<j \le P} \hat{\rho }^{ij}_{1, [Tz]} = J^T vecho(\hat{R}_{1,[Tz]})\) and \(J^T E^{1/2} B_0^{\frac{P(P-1)}{2}}(z) = (J^T EJ)^{1/2} B_0^1(z)\), we get the result from Lemma 3.1. \(\Box \)

Proof of Theorem 3.3

The result follows if we show, jointly,

By Lemma 3.2, it holds

Therefore, if we show

then we have (5) because

We show (9). From the proof of Wied (2017, p.19), under \(H_0\) and (A1)-(A4), we observe, as \(T\rightarrow \infty \), for fixed P,

where \(B^N\) is N-dimensional standard brownian motion. Therefore, we have

Transforming \(H_{T}(z)\) into the correlation vector \((vecho(\hat{R}_{[Tz]+1,T})- vecho(\hat{R}_{1,T}))\) as provided in proof of Theorem 1 in Wied (2017), we get

by applying Theorem 4.2 in Billingsley (1968) and the functional delta method of Theorem A.1 in Wied et al. (2012). Then, by the continuous mapping theorem, we get (9) and hence (5) from (10). The results (6), (7) are arrived at by the combining continuous mapping theorem, Lemma 3.2 and (9). All the convergences in (5)-(7) are joint because they are based on a single convergence of Lemma 3.1. \(\Box \)

Proof of Theorem 3.7

We obtain the result by proving

By (A4), we have, for all t, \(E[X_{it}] = m_{X_i},\) \(E[X_{it}^2] = m_{X_i^2}\) for some constant \(m_{X_i}\) and \(m_{X_i^2}\). Therefore, by the weak law of large numbers, we have, as \(T \rightarrow \infty \), for all i, \(\hat{\sigma }_i^2 = \frac{1}{T} \sum _{t=1}^T (X_{it} - \bar{X}_{i,1,T})^2 {\mathop {\longrightarrow }\limits ^\mathrm{p}}m_{X_i^2} - (m_{X_i})^2 = \sigma _i^2,\) where \(\bar{X}_{i,k,l} = \frac{1}{l-k } \sum _{t=k}^l X_{it}\). Let \(a_{k,l}^{ij} = \frac{1}{l-k} \sum _{t=k}^l (X_{it} - \bar{X}_{i,k,l}) (X_{jt} - \bar{X}_{j,k,l})\). Since \(\hat{\sigma }_i^2\) are consistent, they can be assumed to be known. Under known \(\sigma _i^2\) and \(\sigma _j^2\), we have \(a_{k,l}^{ij} = \hat{\rho }_{k,l}^{ij} \sigma _i \sigma _j\) and therefore

For (11), it suffices to show, as \(T \rightarrow \infty \) and \(t_0/T \rightarrow z_0\), for fixed P,

for which we will show

for some finite random variables \(c_{2}\) and \(c_{3}\).

We first show (i). By (A5), we have \(a_{l,k}^{ij} = \{ m_{X_iX_j} + \frac{1}{l-k} \sum _{t=k}^l (e_t^{ij} + \Delta _{ij} I(t>t_0) )\}\) for some \((e^{12}_t, e^{13}_t, \cdots , e^{1P}_t, e^{23}_t, \cdots , e^{P(P-1)/2}_t)^T\), a stationary NED process satisfying conditions similar to (A1)-(A4) with zero mean and finite variance matrix. We have

Applying the same argument for proving (5) with \(e_t^{ij}\) in place of \(\hat{\rho }_t^{ij}\), we have

and, similarly, we have

for some random variables \(c_{11}\) and \(c_{12}\). Thus, from \(|C_{13}| = | \sqrt{T} \sum _{1 \le i<j \le P} \Delta _{ij}| \rightarrow \infty \), we get (i). The result (ii) is obtained by a similar argument for (12)-(14) as

and the result (iii) is also derived similarly. \(\Box \)

Proof of Theorem 3.10

Let \(C_1(z)\), \(C_2(z)\), \(C_3(z)\), \(Q_T(z)\) be defined in the proof of Theorem 3.7. We have \(Q_T = \sup _{z\in [0,1]} Q_T(z)\), \(Q_T(z) =\frac{\{ \sqrt{T} z (1-z)C_{1}(z)\}^2}{TC_{2}(z) + T C_{3}(z)}\). From proofs of Theorem 3.3, 3.7, we have, jointly,

and hence the result.\(\Box \)

References

Adams Z, Gluck T (2015) Financialization in commodity markets: a passing trend or the new normal? J Bank Finance 60:93–111

Berens T, Weiß GNF, Wied D (2015) Testing for structural breaks in correlations: Does it improve Value-at-Risk forecasting? J Empir Finance 32:135–152

Billingsley P (1968) Convergence of probability measures. Wiley, New York

Choi JE, Shin DW (2019a) Moving block bootstrapping for a CUSUM test for correlation change. Comput Stat Data Anal 135:95–106

Choi JE, Shin DW (2019b) A self-normalization test for correlation change. Econ Lett. https://doi.org/10.1016/j.econlet.2019.02.007

Choi J E, Shin D W (2020) Subsample scan test for multiple breaks based on self-normalization, working paper

Demetrescu M, Wied D (2019) Testing for constant correlation of filtered series under structural change. Econom J 22:10–33

Duan F, Wied D (2018) A residual-based multivariate constant correlation test. Metrika 81:653–687

Galeano P, Wied D (2014) Multiple break detection in the correlation structure of random variables. Comput Stat Data Anal 76:262–282

Goncalves S, White H (2005) Bootstrap standard error estimates for linear regression. J Am Stat Assoc 100:970–979

Kiefer NM, Vogelsang TJ, Bunzel H (2000) Simple robust testing of regression hypotheses. Econometrica 68:695–714

Le V, Wang Q (2014) Robust thresholding for diffusion index forecast. Econ Lett 125:52–56

Lobato IN (2001) Testing that a dependent process is uncorrelated. J Am Stat Assoc 96:1066–1076

Posch PN, Ullmann D, Wied D (2019) Detecting structural changes in large portfolios. Empir Econ 56:1341–1357

Shao X (2010) The dependent wild bootstrap. J Am Stat Assoc 105:218–235

Shao X, Zhang X (2010) Testing for change points in time series. J Am Stat Assoc 105:1228–1240

Wied D (2017) A nonparametric test for a constant correlation matrix. Econom Rev 36:1157–1172

Wied D, Krämer W, Dehling H (2012) Testing for a change in correlation at an unknown point in time using an extended functional delta method. Econom Theory 28:570–589

Wied D, Ziggel D, Berens T (2013) On the application of new tests for structural changes on global minimum-variance portfolios. Stat Pap 54:955–975

Yau CY, Zhao Z (2016) Inference for multiple change points in time series via likelihood ratio scan statistics. J R Stat Soc 78:895–916

Acknowledgements

The authors are very thankful of two anonymous referees whose comments improved the paper considerably. This study was supported by a grant from the National Research Foundation of Korea (2019R1A2C1004679).

Author information

Authors and Affiliations

Corresponding author

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Rights and permissions

About this article

Cite this article

Choi, JE., Shin, D.W. A self-normalization break test for correlation matrix. Stat Papers 62, 2333–2353 (2021). https://doi.org/10.1007/s00362-020-01188-y

Received:

Revised:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s00362-020-01188-y