Abstract

In this study, we propose a regime-switching model for temperature dynamics, where the parameters depend on a Markov chain. We improve upon the traditional models by modeling jumps in temperature dynamics via the chain itself. Moreover, we compare the performance of the proposed model with the existing models. The results indicate that the proposed model outperforms in the short time forecast horizon while the forecast performance of the proposed model is in line with the existing models for the long time horizon. It is shown that the proposed model is a relatively better representation of temperature dynamics compared to the existing models. Furthermore, we derive prices of weather derivatives written on several temperature indices.

Similar content being viewed by others

References

Alaton, P., Djehiche, B., Stillberger, D.: On modelling and pricing weather derivatives. Appl. Math. Finance 9(1), 1–20 (2002)

Alexandridis, A.K., Zapranis, A.D.: The weather derivatives market. In: Weather Derivatives, pp. 1–20. Springer, New York, NY (2013). https://doi.org/10.1007/978-1-4614-6071-8_1

Benth, F.E., Šaltytė Benth, J.: Stochastic modelling of temperature variations with a view towards weather derivatives. Appl. Math. Finance 12(1), 53–85 (2005)

Benth, F.E., Šaltytė Benth, J.: The volatility of temperature and pricing of weather derivatives. Quant. Finance 7(5), 553–561 (2007)

Benth, F.E., Šaltytė Benth, J.: Weather derivatives and stochastic modelling of temperature. Int. J. Stoch. Anal. (2011). https://doi.org/10.1155/2011/576791

Benth, F.E., Šaltytė Benth, J.: Modeling and Pricing in Financial Markets for Weather Derivatives, vol. 17. World Scientific, Singapore (2013)

Benth, F.E., Šaltytė Benth, J., Koekebakker, S.: Putting a price on temperature. Scand. J. Stat. 34(4), 746–767 (2007)

Bo, L., Capponi, A.: Optimal investment under information driven contagious distress. SIAM J. Control Optim. 55(2), 1020–1068 (2017)

Brody, D.C., Syroka, J., Zervos, M.: Dynamical pricing of weather derivatives. Quant. Finance 2(3), 189–198 (2002)

Buffington, J., Elliott, R.J.: American options with regime switching. Int. J. Theor. Appl. Finance 5(05), 497–514 (2002)

Cappé, O., Moulines, E., Rydén, T.: Inference in Hidden Markov Models. Springer, New York (2005)

Carr, P., Madan, D.: Option valuation using the fast Fourier transform. J. Comput. Finance 2(4), 61–73 (1999)

CME: Weather products, http://www.cmegroup.com/trading/weather/ (2016). Accessed July 2016

Dempster, A.P., Laird, N.M., Rubin, D.B.: Maximum likelihood from incomplete data via the EM algorithm. J. R. Stat. Soc. Ser. B (Methodol.) 39(1), 1–38 (1977)

Diebold, F.X.: Comparing predictive accuracy, twenty years later: a personal perspective on the use and abuse of Diebold–Mariano tests. J. Bus. Econ. Stat. 33(1), 1–1 (2015)

Diebold, F.X., Mariano, R.S.: Comparing predictive accuracy. J. Bus. Econ. Stat. 20, 134–144 (2012)

Dornier, F., Queruel, M.: Caution to the wind. Energy Power Risk Manag. 13(8), 30–32 (2000)

Dufour, F., Elliott, R.: Filtering with discrete state observations. Appl. Math. Optim. 40(2), 259–272 (1999)

Elias, R., Wahab, M., Fang, L.: A comparison of regime-switching temperature modeling approaches for applications in weather derivatives. Eur. J. Oper. Res. 232(3), 549–560 (2014)

Elliott, R.J., Aggoun, L., Moore, J.B.: Hidden Markov Models: Estimation and Control, vol. 29. Springer, Berlin (1995)

Enders, W., Doan, T.: Estimating a threshold autoregression. In: RATS programming manual 2nd Edition. pp. 159–169 (2014)

Folland, G.: Real Analysis: Modern Techniques and Their Applications Pure and Applied Mathematics. Wiley, New York (1984)

Franses, P.H., Van Dijk, D.: Non-linear Time Series Models in Empirical Finance. Cambridge University Press, Cambridge (2000)

Glasserman, P.: Monte Carlo Methods in Financial Engineering, vol. 53. Springer, Berlin (2003)

Guo, X.: Information and option pricings. Quant. Finance 1(1), 38–44 (2001)

Hamilton, J.D.: A new approach to the economic analysis of nonstationary time series and the business cycle. Econometrica 57(2), 357–384 (1989). https://doi.org/10.2307/1912559

Hamilton, J.D.: Analysis of time series subject to changes in regime. J. Econom. 45(1), 39–70 (1990)

Hyndman, R.J., Koehler, A.B.: Another look at measures of forecast accuracy. Int. J. Forecast. 22(4), 679–688 (2006)

Janczura, J., Weron, R.: http://ideas.repec.org/s/wuu/hscode.html (2011). Accessed 21 Oct 2015

Janczura, J., Weron, R.: Efficient estimation of Markov regime-switching models: an application to electricity spot prices. AStA Adv. Stat. Anal. 96(3), 385–407 (2012)

Kallsen, J., Shiryaev, A.N.: The cumulant process and Esscher’s change of measure. Finance Stoch. 6(4), 397–428 (2002)

Kim, C.J.: Dynamic linear models with Markov-switching. J. Econom. 60(1), 1–22 (1994). https://doi.org/10.1016/0304-4076(94)90036-1

Mamon, R.S., Elliott, R.J.: Hidden Markov Models in Finance, vol. 104. Springer, Berlin (2007)

Mamon, R.S., Elliott, R.J.: Hidden Markov Models in Finance. Springer, Berlin (2014)

Mraoua, M., Bari, D.: Temperature stochastic modeling and weather derivatives pricing: empirical study with Moroccan data. Afr. Stat. 2(1), 22–43 (2007)

Naik, V.: Option valuation and hedging strategies with jumps in the volatility of asset returns. J. Finance 48(5), 1969–1984 (1993)

NCDC: National climatic data center, http://www.ncdc.noaa.gov/oa/ncdc.html (2014). Accessed 15 April 2014

Nelson, C.R., Kim, C.J.: State-Space Models with Regime-Switching. MIT Press, Cambridge (1999)

Shen, Y., Fan, K., Siu, T.K.: Option valuation under a double regime-switching model. J. Futures Mark 34(5), 451–478 (2014)

Sotomayor, L.R., Cadenillas, A.: Explicit solutions of consumption-investment problems in financial markets with regime switching. Math. Finance Int. J. Math. Stat. Financ. Econ. 19(2), 251–279 (2009)

Swishchuk, A., Cui, K.: Weather derivatives with applications to Canadian data. J. Math. Finance 3, 81–95 (2013)

Tong, H.: Threshold models. In: Threshold Models in Non-linear Time Series Analysis. Lecture Notes in Statistics, vol 21. Springer, New York, NY Springer (1983). https://doi.org/10.1007/978-1-4684-7888-4_3

Zapranis, A., Alexandridis, A.: Modelling the temperature time-dependent speed of mean reversion in the context of weather derivatives pricing. Appl. Math. Finance 15(4), 355–386 (2008)

Acknowledgements

We would like to thank the reviewers for useful comments and suggestions.

Author information

Authors and Affiliations

Corresponding author

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Appendix

Appendix

Threshold Autoregressive (TAR) model. Consider the 2-state version of the threshold autoregressive (TAR) model proposed by [42] given by

with

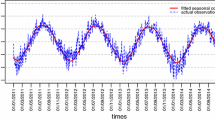

where \( \tau \) is the value of the threshold, see [21]. The estimation results of the 2-state TAR model for the deseasonalized temperature process are presented in Table 18, where the standard errors are given in parenthesis. Figure 16 shows the deseasonalized temperature data together with the TAR model threshold obtained from the estimation of the TAR model.

The TAR model for the deseasonalized temperature data together with the TAR model threshold

Proof of Lemma 2. Remember that, by Eq. (16), under \( \mathbb {P}, \)

By Lemma 1,

and

Hence, under \( \mathbb {Q}^{\theta } \) we can write

and by applying Itô’s Formula, the result follows. \(\square \)

Proof of Lemma 3. By Eq. (13), we have

From Eq. (46), we can write

and, thus,

Now, by Eq. (47), we have

Hence, by Eq. (61), we can write Eq. (60) as

Therefore, by putting Eq. (62) into Eq. (59), the result follows. \(\square \)

Proof of Theorem 1. Remember that by Eq. (4)

By Eq. (48) and Fubini’s Theorem, we have

since by the martingale property

It can be easily shown that

Thus, we have

and

Therefore, by inserting Eqs. (65) and (66) into Eq. (64), the result follows. \(\square \)

Proof of Lemma 4. Let be

and apply Itô’s Formula to \( e^{iuZ_{t}}\). Then,

We define for each \( s \le t \in [0, \mathsf {T}], \)\( \mathcal {\bar{G}}_{s, t}:= \mathcal {F}_{s}\vee \mathcal {F}^{\zeta }_{t}, \) which represents the enlarged \( \sigma \)-field generated by \( \mathcal {F}_{s} \) and \( \mathcal {F}^{\zeta }_{t}\). Moreover, write \( {\bar{\mathbf {G}}}:= ( \mathcal {\bar{G}}_{s, t}: \ s, t \in [0, \mathsf {T}] ) \) for the corresponding complete enlarged filtration. Let \( \varPhi _{Z_{t}|\mathcal {\bar{G}}_{s, t}} (u) \) denote the characteristic function of \( Z_{t} \) conditional on \( \mathcal {\bar{G}}_{s, t}; \) that is,

Then, from above we obtain

For notational convenience, we simply write \( \mathbf {B}^{\theta }(t)=\mathbf {B}^{\theta }(t,u). \) Let \( \mathbf {D}^{\theta }(t) := (d_{jl}^{\theta }(t))_{j,l=1, \ldots , N}, \) where

Notice that \( d_{jl}^{\theta }(t) = b_{jl}^{\theta }(t)/a_{jl}^{\theta }, \) for each \( j, l= 1, \ldots , N\). Define \( \mathbf {D}_{0}^{\theta }(t) := \mathbf {D}^{\theta }(t) - diag[d^{\theta }(t)], \) where \( d^{\theta }(t) = (d_{11}^{\theta }(t), \ldots , d_{NN}^{\theta }(t))' \in \mathbb {R}^{N}\). Then, we can write

where \( \mathcal {M}^{\theta }_{t}=(\mathcal {M}^{\theta 1}_{t}, \ldots , \mathcal {M}^{\theta N}_{t})' \in \mathbb {R}^{N}\). It can be easily shown that, by Remark 1, we can write

with

Therefore, Eq. (68) can be written as

We define

By Itô’s Formula we obtain

Here, we used \( \varPhi _{Z_{t}|\mathcal {\bar{G}}_{s, t}} (u) \zeta _{t} \langle g(t, u), \zeta _{t} \rangle = diag[ g(t, u)] \zeta _{t}\varPhi _{Z_{t}|\mathcal {\bar{G}}_{s, t}} (u)\).

Now, by using

we can write

It can be easily shown that

Hence, we can write

since

and

Thus, by combining Eqs. (73) and (74), we get

Thus, by Eqs. (75), (72) becomes

Therefore, by Fubini’s Theorem and using the martingale property, we have

Thus, we get

and after solving we have

Notice that

since \( \langle \zeta _{t}, \mathbf {1} \rangle = 1\).

Now, by the tower property and Eq. (78), we have

Therefore the result follows by Eq. (77). \(\square \)

Proof of Theorem 2. Remember that by Eq. (5)

Now by Lemma 5, we can write

Thus, by Eq. (79) and Fubini’s Theorem,

where \( \varPhi _{Y_{t}|\mathcal {G}_{s}} (u) = \mathbb {E}^{\theta } \left[ e^{iuY_{t}} | \mathcal {G}_{s}\right] \) is given by Eq. (54).

Therefore, by Fubini’s Theorem and Eq. (80), we obtain

We notice that, by Lemma 4,

Therefore, the result follows. \(\square \)

Rights and permissions

About this article

Cite this article

Türkvatan, A., Hayfavi, A. & Omay, T. A regime switching model for temperature modeling and applications to weather derivatives pricing. Math Finan Econ 14, 1–42 (2020). https://doi.org/10.1007/s11579-019-00242-0

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11579-019-00242-0