Abstract

A growing number of firms in software industry are embracing free entry strategy to promote product adoption. The prevalence of free strategy can be partly attributed to the positive network externalities exhibited by the information goods. In this paper, we model a new firm’s entry into an existing market with the free strategy. Consumers can use the new product’s basic functionality for free and pay a subscription fee for accessing the add-ons. The entrant firm’s new product infringes on the market in one of the three ways: homogeneous product competition, high-end encroachment and low-end encroachment. We find that the equilibrium market structure varies across the three settings. In particular, there exists a Bertrand equilibrium when the new firm provides a homogeneous product. When the new firm offers a heterogeneous product, our results show that the network externalities intensify the price competition and thus lead to a reduction in the profits. Moreover, whether the new firm should encroach on the existing market with high-end product or low-end product depends on the level of switching cost. If the switching cost is low, the new firm will benefit more from high-end encroachment and vice versa. We also find that it is not always optimal for the new firm to adopt the free entry strategy. In the high-end encroachment, the new firm will be better off providing a product for free if the network intensity is high enough, whereas in the low-end encroachment, the free strategy is dominant only when the network intensity falls within a given threshold.

Similar content being viewed by others

References

August T, Niculescu MF, Shin H (2014) Cloud implications on software network structure and security risks. Inf Syst Res 25(3):489–510

Barua A, Kriebel CH, Mukhopadhyay T (1991) An economic analysis of strategic information technology investments. MIS Q 15(3):313–331

Bawa K, Shoemaker R (2004) The effects of free sample promotions on incremental brand sales. Mark Sci 23(3):345–363

Cheng HK, Li S, Liu Y (2014) Optimal software free trial strategy: limited version, time-locked, or hybrid? Prod Oper Manag 24(3):504–517

Cheng HK, Liu Y (2012) Optimal software free trial strategy: the impact of network externalities and consumer uncertainty. Inf Syst Res 23(2):88–504

Cheng HK, Tang QC (2010) Free trial or no free trial: optimal software product design with network. Eur J Oper Res 205(2):437–447

Conner KR (1995) Obtaining strategic advantage from being imitated: when can encouraging ‘clones’ pay? Manag Sci 41(2):209–225

Demirhan D, Jacob VS, Raghunathan S (2007) Strategic IT investments: the impact of switching cost and declining IT cost. Manag Sci 53(2):208–226

Dhebar A (1994) Durable-goods monopolists, rational consumers, and improving. Mark. Sci. 13(1):100–120

Dogan K, Ji Y, Mookerjee VS, Radhakrishan S (2011) Managing the versions of a software product under variable and endogenous demand. Inf. Syst. Res. 22(1):5–21

Ellison G (2005) A model of add-on pricing. Q J Econ 120(2):585–637

Erat S, Bhaskaran SR (2012) Consumer mental accounts and implications to selling base products and add-ons. Mark. Sci. 31(5):801–818

Etzion H, Pang MS (2014) Complementary online services in competitive markets: maintaining profitability in the presence of network effects. MIS Q 38(1):231–247

Faugre C, Tayi GK (2007) Designing free software samples: a game theoretic approach. Inf Technol Manag 8(4):263–278

Fruchter GE, Gerstner E, Dobson PW (2011) Fee or free? How much to add on for an add-on. Mark Lett 22(1):65–78

Gallaugher JM, Wang YM (1999) Network effects and the impact of free goods: an analysis of the web server market. Int J Electron Commer 3(4):67–88

Gartner (2013) Forecast: Mobile App stores, Worldwide, Update. 2013. www.gartner.com/doc/2584918/

Haruvy EE, Miao D, Stecke KE (2013) Various strategies to handle cannibalization in a competitive duopolistic market. Int Trans Oper Res 20(2):155–188

Jing B (2000) Versioning information goods with network externalities. In: Proceedings of the twenty first international conference on Information systems. Association for Information Systems, Atlanta, pp 1–12

Jones R, Mendelson H (2011) Information goods vs. industrial goods: cost structure and competition. Manag Sci 57(1):164–176

Katz ML, Shapiro C (1985) Network externalities, competition, and compatibility. Am Econ Rev 75(3):424–440

Klastorin T, Tsai W (2004) New product introduction: timing, design, and pricing. Manuf Serv Oper Manag 6(4):302–320

Klemperer P (1987a) Markets with consumer switching costs. Q J Econ 102(2):375–394

Klemperer P (1987b) The competitiveness of markets with switching costs. RAND J Econ 18(1):138–150

Lieberman MB, Montgomery DB (2013) Conundra and progress:research on entry order and performance. Long Range Plan 46(4):312–324

Mehra A, Bala R, Sankaranarayanan R (2012) Competitive behavior-based price discrimination for software upgrades. Inf Syst Res 23(1):60–74

Moorthy KS (1988) Product and price competition in a duopoly. Mark Sci 7(2):141–168

Narasimhan C, Zhang ZJ (2000) Market entry strategy under firm heterogeneity and asymmetric payoffs. Mark Sci 19(4):313–327

Niculescu MF, Wu DJ (2014) Economics of free under perpetual licensing: implications for the software industry. Inf Syst Res 25(1):173–199

Nilssen T (1992) Two kinds of consumer switching costs. RAND J Econ 23(4):579–589

Parker G, Alstyne M (2005) Two-sided network effects: a theory of information product design. Manag Sci 51(10):1494–1504

Schmidt GM (2004) Low-end and high-end encroachment strategies for new products. Int J Innov Manag 8(2):167–191

Schmidt GM, Porteus EL (2000) The impact of an integrated marketing and manufacturing innovation. Manuf Serv Oper Manag 2(4):317–336

Seref MMH, Carrillo JE, Yenipazarli A (2015) Multi-generation pricing and timing decisions in new product development. Int J Prod Res. doi:10.1080/00207543.2015.1061220

Shapiro C, Varian HR (1998) Versioning: the smart way to sell information. Harv Bus Rev 107(6):107

Sheer I (2014) Player tally for “League of Legends” Surges. http://blogs.wsj.com/digits/2014/01/27/player-tally-for-league-of-legends-surges/. 2014-1-27

Shivendu S, Zhang Z (2015) Versioning in the software industry: heterogeneous disutility from underprovisioning of functionality. Inf Syst Res 26(4):731–753

Shulman JD, Geng X (2013) Add-on pricing by asymmetric firms. Manag Sci 59(4):899–917

Swinney R, Cachon GP, Netessine S (2011) Capacity investment timing by start-ups and established firms in new markets. Manag Sci 57(4):763–777

Vakratsas D, Rao RC, Kalyanaram G (2003) An empirical analysis of follower entry timing decisions. Mark Lett 14(3):203–216

Verboven F (1999) Product line rivalry and market segmentation with an application to automobile optional engine pricing. J Ind Econ 47(4):399–425

Wei XQ, Nault BR (2013) Experience information goods: “Version-to-upgrade”. Decis Support Syst 56:494–501

Wu S, Chen P (2008) Versioning and piracy control for digital information goods. Oper Res 56(1):157–172

Acknowledgements

This research is partially supported by research grants from the National Science Foundation of China under Grant Nos. 71271148, 71471128, and the Key Program of National Natural Science foundation of China under Grant No. 71631003.

Author information

Authors and Affiliations

Corresponding author

Appendices

Appendix 1

Proof of Lemma 1

Before the entrant (i.e., Firm B) enters into the market, the incumbent (i.e., Firm A) offers the product A at a monopoly price, \(p_{Am}\). Consumers in the market have two choices: buy or not buy the incumbent’s product. The corresponding net utilities are: \(U_{Am}=(\theta +\alpha Q_{Am})v_{A}-p_{Am}\) and 0. The marginal consumer, who is indifferent between buying and not buying, is located at \(\theta _{0}\), and

We derive \(\theta _{0}\) from Eq. (35) as follows:

where \(Q_{Am}\) is the expected network size. The consumers in \([0,\theta _{0}]\) do not purchase, while those in \([\theta _{0},1]\) purchase from the incumbent firm. Hence, the demand of product A is

Substituting Eqs. (37) into (36) and using the rational expectations theory, we derive the demand of product A,

The incumbent sets the price \(p_{Am}\) to maximize its profit \(\pi _{1m}=p_{Am}q_{Am}\).

Differentiating \(\pi _{1m}\) with respect to \(p_{Am}\) yields the following optimal price \(p_{Am}^*\), demand \(q_{Am}\) and profit \(\pi _{1m}^*\) for Firm A,

Thus, we find that

\(\square\)

Proof of Proposition 1

-

(i)

When \(v_{B}>v_{A}\), the analysis in Sect. 4 show that the possible market structures are (1)(4)(6)(5), (1)(3)(6)(5), (1)(3)(2)(5), (1)(6)(5) and (1)(3)(5). For the market structure (1)(4)(6)(5), we have \(\theta _{1}=\theta _{2}=r\). At the boundary point r, we have \(U_{1}(r)=U_{4}(r)\) (see Fig. 2). Simplify this equation and we can find that \(c=0\). Obviously, this violates our setup of \(c>0\). Therefore, this market structure does not exist equilibrium. Similarly, the market structure (1)(3)(2)(5) cannot exist in equilibrium either. For the market structure (1)(6)(5), we get that \(\theta _{1}=\theta _{2}=r=\theta _{3}\). At the boundary point r, we have \(U_{1}(r)=U_{6}(r)\). Furthermore, the price will be set such that \(U_{1}(r)\ge U_{3}(r)\). Note that \(U_{3}(r)=U_{6}(r)\), so we find a contradiction. As a result, the market structure (1)(6)(5) cannot exist when the market comes into equilibrium. Similarly, the market structure (1)(3)(5) cannot exist either. Hence, when \(v_{B}>v_{A}\), the only possible market structure is (1)(3)(6)(5).

-

(ii)

When \(v_{B}<v_{A}\), the proof is similar to that of (i).

-

(iii)

When \(v_{B}=v_{A}\). As noted above, in equilibrium, segment (1) and segment (4) cannot coexist, segment (2) and segment (5) cannot exist, and segment (3) and segment (6) cannot exist.

Hence, if segment 3 exists, we must have

In this case, we obtain that

This implies that no consumers will exercise option (2) and option (5). As a result, Firm B makes no profit in this case. If, however, Firm B charges a low enough price such that \(U_{2}(\theta )\ge U_{3}(\theta )\) and \(U_{5}(\theta )\ge U_{6}(\theta )\), then all consumers will buy from Firm B instead of from Firm A. In that case, Firm A will reduce its price in response to Firm B’s low price. This consequently leads to zero prices in the market and neither firm can be profitable.

Derivation of equilibrium outcomes for Sect. 5.1. Substituting Eqs. (3) and (4) into Eqs. (1) and (2) and employing the rational expectation theory, we derive the marginal consumers and the firms’ demands below.

We first compute the first order conditions of problems (P1) and (P2) and then solve the two conditions simultaneously for the prices \(p_{Ad}\) and \(p_{Bd}\). The closed form of expressions of equilibrium prices are

where \(m=(v_{B}-v_{A})(v_{A}-v_{Bb})-2\alpha v_{A}v_{Ba}\).

Substituting \(p_{Ad}^*\) and \(p_{Bd}^*\) back into the objective functions of problems (P1) and (P2) yields the equilibrium profits, \(\pi _{1d}^*\) and \(\pi _{2d}^*\), for the two firms.

Derivation of equilibrium outcomes for Sect. 5.2. Substituting Eqs. (16) and (17) back into Eqs. (14) and (15), we have

Solving the optimization problems (P3) and (P4) yields the equilibrium prices,

Substituting the above equilibrium prices into the objective functions of problems (P3) and (P4) yields the optimal profits, which are given by

Proof of Proposition 2

The first-order conditions of the profits of Firm A and Firm B with respect to c are given as follows.

where \(\partial p_{Ad}^*/\partial c\) and \(\partial p_{Bd}^*/\partial c\) are the first-order conditions of Eqs. (52) and (53). Taking the derivative of \(p_{Ad}^*\) and \(p_{Bd}^*\) with respect to c yields

The price of product A, \(p_{Ad}^*\), should be positive. According to Lemma 2, we have \(m>0\). Hence, the sign of \(\partial \pi _{1d}^*/\partial c\) depends on the sign of \(\partial p_{Ad}^*/\partial c\), which is positive as given by Eq. (58). Therefore, \(\partial \pi _{1d}^*/\partial c>0\). That is, the price of product A and the profit of Firm A increase with switching cost. Similarly, we can get that \(\partial \pi _{2d}^*/\partial c<0\), which means that the price of product B and the profit of Firm B decrease in the switching cost. \(\square\)

Derivation of equilibrium solutions for Sect. 6.1. By using Kuhn-Tucker conditions of the above function and the first-order condition of Firm A’s profit function, we find that the case of \(\mu >0\) yields the condition under which offering a free version product (i.e, \(p_f=0\)) is an optimal solution for Firm B. It follows that

where \(m=(v_{B}-v_{A})(v_{A}-v_{Bb})-2\alpha v_{A}v_{Ba}\), and

Derivation of equilibrium solutions for Sect. 6.2. The optimization problems could be solved in the same way as in Sect. 6.1. The case of \(\mu >0\) provides the condition under which offering a free version product (i.e, \(p_f=0\)) is an optimal solution for Firm B. It follows that

Proof of Proposition 3

In equilibrium, we find that \(\mu =\theta _{6}^{*}g(\alpha )\), where \(\theta _{6}^{*}\) is obtained by substituting the equilibrium prices back into the indifferent points, and \(g( \alpha )=-\frac{{{\alpha }^{2}}{{v}_{Ba}}+\alpha (2{{v}_{A}}+3{{v}_{B}}-{{v}_{Bb}})-2({{v}_{A}}-{{v}_{B}})}{\alpha ({{v}_{Bb}}+2{{v}_{A}}+{{v}_{B}})+{{v}_{B}}+{{v}_{Bb}}-2{{v}_{A}}}\). Because \(\theta _{6}^{*}>0\) in equilibrium, the above solution is feasible if and only if \(g( \alpha )>0\). Consequently, we have

where \({{\alpha }_{1}}=\frac{-2{{v}_{A}}-3{{v}_{B}}+{{v}_{Bb}}+\sqrt{4{{v}_{A}}({{v}_{A}}+5{{v}_{B}}-3{{v}_{Bb}})+{{({{v}_{B}}+{{v}_{Bb}})}^{2}}}}{2({{v}_{B}}-{{v}_{Bb}})}\), and \({{\alpha }_{2}}=\frac{2{{v}_{A}}-{{v}_{B}}-{{v}_{Bb}}}{2{{v}_{A}}+{{v}_{B}}+{{v}_{Bb}}}\).

Appendix 2

In Appendix 2, we consider a first time user cost in consumer utility functions. The first time user cost is incurred when the consumers use a new product at the first time. The consumers who buy from Firm A in stage 1 do not incur such a cost, but they incur a switching cost if moving to Firm B’s product. Let f denote the first time user cost. There are a total of six options available for consumers. Consequently, the utility for various options available to the consumers are listed below:

-

(1)

Consumers who have not purchased product A now use the free base part of product B and obtain a net utility of \({{U}_{1}}=\left( \theta +\alpha {{Q}_{Bd}} \right) {{v}_{Bb}}-f\).

-

(2)

Consumers who have not purchased product A now use the whole product B and obtain a net utility of \({{U}_{2}}=\left( \theta +\alpha {{Q}_{Bd}} \right) {{v}_{B}}-{{p}_{Bd}}-f\).

-

(3)

Consumers who have not purchased product A now adopt it and obtain a net utility of \({{U}_{3}}=\left( \theta +\alpha {{Q}_{Ad}} \right) {{v}_{A}}-{{p}_{Ad}}-f\).

-

(4)

Consumers who have purchased product A now switch to Firm 2’s free offering and the net utility is \({{U}_{4}}=\left( \theta +\alpha {{Q}_{Bd}} \right) {{v}_{Bb}}-c\).

-

(5)

Consumers who have purchased product A now switch to the whole product B and the net utility is \({{U}_{5}}=\left( \theta +\alpha {{Q}_{Bd}} \right) {{v}_{B}}-{{p}_{Bd}}-c\).

-

(6)

Consumers who have purchased product A now continue to pay for it. The net utility is \({{U}_{6}}=\left( \theta +\alpha {{Q}_{Ad}} \right) {{v}_{A}}-{{p}_{Ad}}\).

Lemma B1

Before Firm B enters the market, the incumbent offers its product at the price of \(\frac{1}{2}({v_A}-f)\). There are two segments of consumers in the market. The proportion of customers who do not buy from the incumbent is \(r=\frac{f+{v_{A}}-2\alpha {v_{A}}}{2{v_{A}}(1-\alpha )}\) and the proportion of buyers is \(1-r=\frac{{{v}_{A}}-f}{2{{v}_{A}}(1-\alpha )}\).

In this model setup, we find that different market structure exists in equilibrium under different conditions. In the following, we analyze the market structure under different conditions and give the equilibrium result under each structure.

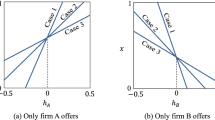

Case (i). \({{v}_{B}}>{{v}_{A}}\).

If \({{v}_{B}}>{{v}_{A}}\), the market structure must encompass the six segments in the order (1)(3)(2)(4)(6)(5) from the left. However, it does not imply all these six segments must exist. We show the equilibrium market structure under different conditions below.

Case (ia). \({{v}_{B}}>{{v}_{A}}\) and \(f>c>0\).

When \(f>c>0\), from the utility functions we obtain \({{U}_{2}}<{{U}_{5}}\). If in equilibrium the market structure is (1)(3)(2)(4)(6)(5), then the utility of the indifferent customers located at r should satisfy \({{U}_{2}}(r)={{U}_{4}}(r)\). Using \({{U}_{2}}<{{U}_{5}}\) and \({{U}_{2}}(r)={{U}_{4}}(r)\) gives us \({{U}_{4}}<{{U}_{5}}\), which implies that the customers on the right of indifferent point r will not choose option (4) and so option (4) is dominated. Therefore, the possible market structure is (1)(3)(2)(6)(5). Similarly, at the indifferent point r, the condition \({{U}_{2}}(r)={{U}_{6}}(r)\) should hold. Using \({{U}_{2}}<{{U}_{5}}\) and \({{U}_{2}}(r)={{U}_{6}}(r)\), we have \({{U}_{5}}>{{U}_{6}}\). This implies that option (6) is dominated by option (5). As a result, no consumers will exercise option (6) and the possible market structure is (1)(3)(2)(5). To implement this market structure, the condition \({{U}_{2}}(r)={{U}_{5}}(r)\) should be satisfied, but because \({{U}_{2}}<{{U}_{5}}\), we find a contradiction. Therefore, no consumers located on the left of r will exercise option (2). Consequently, the equilibrium market structure in this case is (1)(3)(5), as illustrated in Fig. 15.

Market structure when \({{v}_{B}}>{{v}_{A}}\) and \(f>c>0\)

In this setting, all consumers who have purchased from Firm A now switch to Firm B and pay for its add-ons. Next we determine the profit-maximizing prices set by Firm A and Firm B to implement this market structure. In segment (5), the price of Firm B is set so that the indifferent customers located at r get a weakly higher surplus from switching compared to the surplus from either continuing to buy from Firm A or use the free base product from Firm B. These constraints are given by

These constraints yield the price \({{p}_{Bd}}=\min \{\left( r+\alpha {{Q}_{Bd}} \right) {{v}_{B}}-\left( r+\alpha {{Q}_{Ad}} \right) {{v}_{A}}-c+{{p}_{Ad}},\left( r+\alpha {{Q}_{Bd}} \right) ({{v}_{B}}-{{v}_{Bb}})\}\), where \({{Q}_{Ad}}=r-{{\theta }_{13}}\), \({{Q}_{Bd}}=1-r+{{\theta }_{13}}\), and \(r=\frac{f+{v_{A}}-2\alpha {v_{A}}}{2{v_{A}}(1-\alpha )}\). Similarly, we can find \({{p}_{Ad}}=\min \{\left( {{\theta }_{13}}+\alpha {{Q}_{Ad}} \right) {{v}_{A}}-\left( {{\theta }_{13}}+\alpha {{Q}_{Bd}} \right) {{v}_{Bb}},\left( {{\theta }_{13}}+\alpha {{Q}_{Ad}} \right) {{v}_{A}}-\left( {{\theta }_{13}}+\alpha {{Q}_{Bd}} \right) {{v}_{B}}+{{p}_{Bd}}\}\). The indifferent point \({{\theta }_{13}}\) is obtained by solving \(\left( {{\theta }_{13}}+\alpha {{Q}_{Bd}} \right) {{v}_{Bb}}-f=\left( {{\theta }_{13}}+\alpha {{Q}_{Ad}} \right) {{v}_{A}}-{{p}_{Ad}}-f\).

The optimization problems of the firms are as follows:

Solving the above optimization problem of Firm A yields the price, indifferent point and profit as follows:

For Firm B’s optimization problem, we find that its profit is increasing in \(p_{Bd}\). By substituting \(p_{Ad}^*\) into the constraint, \({{p}_{Bd}}=\min \{\left( r+\alpha \left( 1-r+\theta _{13}^{*} \right) \right) {{v}_{B}}-\left( r+\alpha \left( r-\theta _{13}^{*} \right) \right) {{v}_{A}}-c+p_{Ad}^{*},\left( r+\alpha \left( 1-r+\theta _{13}^{*} \right) \right) ({{v}_{B}}-{{v}_{Bb}})\}\), we could get the optimal price of Firm B.

Case (ib). \({{v}_{B}}>{{v}_{A}}\) and \(0<f\le c\).

When \(0<f\le c\), we obtain \({{U}_{1}}\ge {{U}_{4}}\) and \({{U}_{3}}<{{U}_{6}}\). If the market structure in equilibrium is (1)(3)(2)(4)(6)(5), then at the indifferent point , the condition \({{U}_{2}}(r)={{U}_{4}}(r)\) should hold. Using \({{U}_{1}}\ge {{U}_{4}}\) and \({{U}_{2}}(r)={{U}_{4}}(r)\) gives us \({{U}_{1}}\ge {{U}_{2}}\), which implies that option (2) is dominated by option (1). Thus, no consumers will choose option (2). Hence, the possible market structure is (1)(3)(4)(6)(5). At point , we have \({{U}_{3}}(r)={{U}_{4}}(r)\). Using \({{U}_{3}}<{{U}_{6}}\) and \({{U}_{3}}(r)={{U}_{4}}(r)\) gives us \({{U}_{6}}>{{U}_{4}}\). Thus option (4) is dominated and the possible market structure is (1)(3)(6)(5). In this case, the condition \({{U}_{3}}(r)={{U}_{6}}(r)\) should be satisfied. However, from the utility function we have \({{U}_{3}}<{{U}_{6}}\). Hence, option (3) and option (6) cannot coexist. Consequently, the equilibrium market structure when \(0<f\le c\) is (1)(3)(5) or (1)(6)(5).

Under the market structure (1)(3)(5), we could derive the equilibrium results that are the same as in Case (ia). Next, we focus on the analysis on market structure (1)(6)(5), which is illustrated in Fig. 16.

Market structure when \({{v}_{B}}>{{v}_{A}}\) and \(0<f\le c\)

In this setting, the consumers in segment (6) buy from Firm A and thus the demand of Firm A is \({{\theta }_{56}}-r\), the consumers whose valuation is higher than \({{\theta }_{56}}\) purchase the add-ons from Firm B, and the consumers on the left of use the free base product from Firm B. In addition, in segment (6), the price of Firm A is set so that the indifferent customers located at \({{\theta }_{56}}\) get a weakly higher surplus from continuing to buy from Firm A compared to the surplus from switching to either free product or add-ons offered by Firm B. These constraints are given by

This constraint yields the price \({{p}_{Ad}}=\min \{\left( r+\alpha {{Q}_{Ad}} \right) {{v}_{A}}-\left( r+\alpha {{Q}_{Bd}} \right) {{v}_{Bb}}+c,{{p}_{Bd}}+c\left( r+\alpha {{Q}_{Ad}} \right) {{v}_{A}}-\left( r+\alpha {{Q}_{Bd}} \right) {{v}_{B}}\}\), where \({{Q}_{Ad}}={{\theta }_{56}}-r\) and \({{Q}_{Bd}}=1-{{Q}_{Ad}}\). Following similar logic we find that \({{p}_{Bd}}=\min \{\left( {{\theta }_{56}}+\alpha {{Q}_{Bd}} \right) {{v}_{B}}-\left( {{\theta }_{56}}+\alpha {{Q}_{Ad}} \right) {{v}_{A}}-c+{{p}_{Ad}},\left( {{\theta }_{56}}+\alpha {{Q}_{Bd}} \right) ({{v}_{B}}-{{v}_{Bb}})\}\). The indifferent point \({{\theta }_{56}}\) is obtained by solving \(-{{p}_{Bd}}-c+\left( {{\theta }_{56}}+\alpha {{Q}_{Bd}} \right) {{v}_{B}}=\left( {{\theta }_{56}}+\alpha {{Q}_{Ad}} \right) {{v}_{A}}-{{p}_{Ad}}\).

Accordingly, we can write the firms profit functions,

By examining the second order condition of \({{\pi }_{1d}}\), we find that \({{\pi }_{1d}}\) is convex in \({{p}_{Ad}}\). Thus, in equilibrium the optimal price of Firm A is \({{p}_{Ad}}=\min \{\left( r+\alpha {{Q}_{Ad}} \right) {{v}_{A}}-\left( r+\alpha {{Q}_{Bd}} \right) {{v}_{Bb}}+c,\left( r+\alpha {{Q}_{Ad}} \right) {{v}_{A}}-\left( r+\alpha {{Q}_{Bd}} \right) {{v}_{B}}+{{p}_{Bd}}+c\}\). Solving the optimization problem of Firm B yields \({{p}_{Bd}}=(-{{v}_{A}}\left( 1+a\left( 1-r \right) \right) +{{v}_{B}}\left( 1+ar \right) -c+{{p}_{Ad}})/2\) By substituting the expression for \({{p}_{Bd}}\) into \({{\theta }_{56}}\) and comparing \(\left( r+\alpha {{Q}_{Ad}} \right) {{v}_{A}}-\left( r+\alpha {{Q}_{Bd}} \right) {{v}_{Bb}}+c\) and \(\left( r+\alpha {{Q}_{Ad}} \right) {{v}_{A}}-\left( r+\alpha {{Q}_{Bd}} \right) {{v}_{B}}+{{p}_{Bd}}+c\) in the constraint for \({{p}_{Ad}}\), we could get the equilibrium prices and profits.

Case (ic). \({{v}_{B}}>{{v}_{A}}\) and \(f=0,c>0\).

When \(f=0,c>0\), we have \({{U}_{1}}>{{U}_{4}}\) and \({{U}_{3}}={{U}_{6}}\). If in equilibrium the market structure (1)(3)(2)(4)(6)(5) is implemented, then at point r, the condition \({{U}_{2}}(r)={{U}_{4}}(r)\) should satisfy. Using \({{U}_{1}}>{{U}_{4}}\) and \({{U}_{2}}(r)={{U}_{4}}(r)\), we have \({{U}_{1}}>{{U}_{2}}\). Thus, no consumers will exercise option (2) and so the possible market structure is (1)(3)(4)(6)(5). In this case, the condition \({{U}_{3}}(r)={{U}_{4}}(r)\) should hold at point . Using \({{U}_{3}}={{U}_{6}}\) and \({{U}_{3}}(r)={{U}_{4}}(r)\), we have \({{U}_{6}}\ge {{U}_{4}}\) for consumers on the right of point r. Thus, no consumers will exercise option (4). As a result, the market structure in equilibrium is (1)(3)(6)(5).

In the setting where \({{v}_{B}}>{{v}_{A}}\) and \(f=0,c>0\), we obtain the same results as shown in Sect. 5.1 in the main body.

Case (ii). \({{v}_{B}}<{{v}_{A}}\).

If \({{v}_{B}}<{{v}_{A}}\), the market structure must encompass the six segments in the order (1)(2)(3)(4)(5)(6) from the left.

Case (iia). \({{v}_{B}}<{{v}_{A}}\) and \(f>c>0\).

When \(f>c>0\), we have \({{U}_{3}}<{{U}_{6}}\). If in equilibrium the market structure (1)(2)(3)(4)(5)(6) is implemented, then at point , the condition \({{U}_{3}}(r)={{U}_{4}}(r)\) satisfies. Using \({{U}_{3}}<{{U}_{6}}\) and \({{U}_{3}}(r)={{U}_{4}}(r)\) gives us \({{U}_{6}}>{{U}_{4}}\), which implies that option (4) is dominated by option (6). Thus, no consumers will exercise option (4) and so the market structure is (1)(2)(3)(5)(6). At point , the condition \({{U}_{3}}(r)={{U}_{5}}(r)\) should be satisfied. Because \({{U}_{3}}<{{U}_{6}}\), we have \({{U}_{6}}>{{U}_{5}}\). Thus option (5) is dominated and so the possible market structure is (1)(2)(3)(6). In this case, however, the condition \({{U}_{3}}(r)={{U}_{6}}(r)\) cannot be satisfied because \({{U}_{3}}<{{U}_{6}}\). Therefore, option (3) will not be exercised. Consequently, the market structure in equilibrium is (1)(2)(6), as illustrated in Fig. 17.

Market structure when \({{v}_{B}}<{{v}_{A}}\) and \(f>c>0\)

In this setting, the new consumers located between \({{\theta }_{12}}\) and buy the add-ons from Firm B and all the old consumers located on the right of continue to buy from Firm A. In segment (2), the price of Firm B is set so that the marginal customers located at \({{\theta }_{12}}\) derive higher surplus from buying the add-ons compared to the surplus derived from either using Firm B’s free product or buy from Firm A. These constraints are

Thus we have \({{p}_{Bd}}=\min \{\left( {{\theta }_{12}}+\alpha {{Q}_{Bd}} \right) \left( {{v}_{B}}-{{v}_{Bb}} \right) ,\left( {{\theta }_{12}}+\alpha {{Q}_{Bd}} \right) {{v}_{B}}-\left( {{\theta }_{12}}+\alpha {{Q}_{Ad}} \right) {{v}_{A}} +{{p}_{Ad}}\}\). Here, \({{\theta }_{12}}\) is obtained by solving \(\left( {{\theta }_{12}}+\alpha {{Q}_{Bd}} \right) {{v}_{Bb}}-f=\left( {{\theta }_{12}}+\alpha {{Q}_{Bd}} \right) {{v}_{B}}-{{p}_{Bd}}-f\) and \({{Q}_{Bd}}=1-r\). Additionally, in segment (6), the price of Firm B is set so that the marginal customers located at r derive a weakly higher surplus from buying product A compared to the surplus that they derive from switching to either product offered by Firm B. These constraints are

Thus we get \({{p}_{Ad}}=\min \{\left( r+\alpha {{Q}_{Ad}} \right) {{v}_{A}}-\left( r+\alpha {{Q}_{Bd}} \right) {{v}_{Bb}}+c,\left( r+\alpha {{Q}_{Ad}} \right) {{v}_{A}}+{{p}_{Bd}}+c-\left( r+\alpha {{Q}_{Bd}} \right) {{v}_{B}}\}\).

The optimization problems of the firms are given below

It is straightforward that the profit of Firm A \({{\pi }_{1d}}\) is convex in \({{p}_{Ad}}\). Solving the problem of Firm B gives us the indifferent point, price and profit in equilibrium below,

The equilibrium price of Firm A could also be obtained by substituting \(p_{Bb}^{*}\) into the constraint \({{p}_{Ad}}=\min \{\left( r+\alpha {{Q}_{Ad}} \right) {{v}_{A}}-\left( r+\alpha {{Q}_{Bd}} \right) {{v}_{Bb}}+c,\left( r+\alpha {{Q}_{Ad}} \right) {{v}_{A}}-\left( r+\alpha {{Q}_{Bd}} \right) {{v}_{B}}+{{p}_{Bd}}+c\}\). Consequently, we have \(p_{Ab}^{*}=\{r+c+a\left( 1-r \right) {{v}_{A}}-r\left( 1+a \right) {{v}_{Bb}},r+c+a\left( 1-r \right) {{v}_{A}}-r\left( 1+a \right) {{v}_{B}}+({{v}_{B}}-{{v}_{Bb}})(a+r-ar)/2\}\).

Case (iib). \({{v}_{B}}<{{v}_{A}}\) and \(0<f\le c\).

When \(0<f\le c\), the market structure in equilibrium could be obtained in the same way as in Case (iia). Consequently, the equilibrium market structure in this case is (1)(2)(6). Furthermore, the market outcomes in this setting are also the same in the above setting. Hence, we rule out the corresponding analysis here.

Case (iic). \({{v}_{B}}<{{v}_{A}}\) and \(f=0,c>0\).

When \(f=0,c>0\), we have \({{U}_{3}}={{U}_{6}}\). If in equilibrium the market structure (1)(2)(3)(4) (5)(6) is implemented, then at point the condition \({{U}_{3}}(r)={{U}_{4}}(r)\) should hold. Using \({{U}_{3}}={{U}_{6}}\) and \({{U}_{3}}(r)={{U}_{4}}(r)\) yields \({{U}_{6}}>{{U}_{4}}\) for customers on the right of point . Hence, option (4) is dominated by option (6) and the possible market structure is (1)(2)(3)(5)(6). In this case, using \({{U}_{3}}(r)={{U}_{5}}(r)\) at point r and \({{U}_{3}}={{U}_{6}}\), we get \({{U}_{6}}>{{U}_{5}}\). Therefore, no customers will choose option (5). Consequently, the equilibrium market structure is (1)(2)(3)(6).

In the setting where \({{v}_{B}}<{{v}_{A}}\) and \(f=0,c>0\), we could obtain the same results as shown in Sect. 5.2 in the main body.

Rights and permissions

About this article

Cite this article

Nan, G., Li, X., Zhang, Z. et al. Optimal pricing for new product entry under free strategy. Inf Technol Manag 19, 1–19 (2018). https://doi.org/10.1007/s10799-016-0271-7

Published:

Issue Date:

DOI: https://doi.org/10.1007/s10799-016-0271-7