Methodology and Computing in Applied Probability ( IF 0.9 ) Pub Date : 2022-06-16 , DOI: 10.1007/s11009-022-09965-y Salim Bouzebda, Issam Elhattab, Anouar Abdeldjaoued Ferfache

|

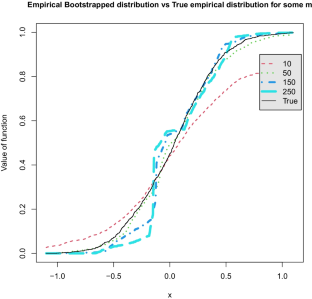

In the present paper, we consider the problem of the estimation of a parameter \(\varvec{\theta }\), in Banach spaces, maximizing some criterion function which depends on an unknown nuisance parameter h, possibly infinite-dimensional. The classical estimation methods are mainly based on maximizing the corresponding empirical criterion by substituting the nuisance parameter by a nonparametric estimator. We show that the M-estimators converge weakly to maximizers of Gaussian processes under rather general conditions. The conventional bootstrap method fails in general to consistently estimate the limit law. We show that the m out of n bootstrap, in this extended setting, is weakly consistent under conditions similar to those required for weak convergence of the M-estimators. The aim of this paper is therefore to extend the existing theory on the bootstrap of the M-estimators. Examples of applications from the literature are given to illustrate the generality and the usefulness of our results. Finally, we investigate the performance of the methodology for small samples through a short simulation study.

京公网安备 11010802027423号

京公网安备 11010802027423号