European Journal of Operational Research ( IF 6.4 ) Pub Date : 2021-09-10 , DOI: 10.1016/j.ejor.2021.09.003 Carol Alexander 1, 2 , Xiaochun Meng 1 , Wei Wei 1

|

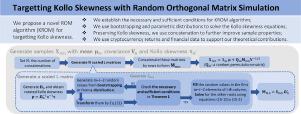

High-dimensional multivariate systems often lack closed-form solutions and are therefore resolved using simulation. Random Orthogonal Matrix (ROM) simulation is a state-of-the-art method that has gained popularity in this context because certain simulation errors are completely removed (Ledermann, Alexander, and Ledermann, 2011). Specifically, every sample generated with ROM simulation exactly matches a target mean and covariance matrix. A simple extension can also target a scalar measure of skewness or kurtosis. However, targeting non-scalar measures of higher moments is much more complex. The problem of targetting exact Kollo skewness has already been considered, but the algorithm proceeds via time-consuming trial-and-error which can be very slow. Moreover, the algorithm often fails completely. Furthermore, it produces simulations with very long periods of inactivity which are inappropriate for most real-world applications. This paper provides an in-depth theoretical analysis of a much quicker ROM simulation extension which always succeeds to target Kollo skewness exactly. It also derives new results on Kollo skewness in concatenated samples and applies them to produce realistic simulations for many applications, especially those in finance. Our first contribution is to establish necessary and sufficient conditions for Kollo skewness targeting to be possible. Then we introduce two novel methods, one for speeding up the algorithm and another for improving the statistical properties of the simulated data. We illustrate several new theoretical results with some extensive numerical analysis and we apply the algorithm using some real data drawn from two different multivariate systems of financial returns.

中文翻译:

使用随机正交矩阵模拟瞄准 Kollo 偏度

高维多元系统通常缺乏封闭形式的解决方案,因此使用模拟解决。随机正交矩阵 (ROM) 模拟是一种最先进的方法,由于完全消除了某些模拟错误,因此在这种情况下很受欢迎(Ledermann、Alexander 和 Ledermann,2011 年)。具体而言,ROM仿真生成的每个样品准确匹配目标均值和协方差矩阵。一个简单的扩展也可以针对偏度或峰度的标量度量。然而,针对更高矩的非标量度量要复杂得多。已经考虑了针对精确 Kollo 偏度的问题,但该算法通过耗时的反复试验进行,这可能非常缓慢。此外,该算法经常完全失败。此外,它会产生长时间不活动的模拟,这不适用于大多数现实世界的应用程序。本文对更快的 ROM 仿真扩展进行了深入的理论分析,该扩展总是能够准确地针对 Kollo 偏度。它还得出关于串联样本中 Kollo 偏度的新结果,并将其应用于许多应用程序的真实模拟,尤其是金融领域的。我们的第一个贡献是为 Kollo 偏度定位成为可能建立充分必要条件。然后我们介绍两种新方法,一种用于加速算法,另一种用于改进模拟数据的统计特性。我们通过一些广泛的数值分析来说明几个新的理论结果,并使用从两个不同的多元金融回报系统中提取的一些真实数据来应用该算法。

京公网安备 11010802027423号

京公网安备 11010802027423号