Research in International Business and Finance ( IF 6.143 ) Pub Date : 2021-07-07 , DOI: 10.1016/j.ribaf.2021.101491 Masayasu Kanno 1

|

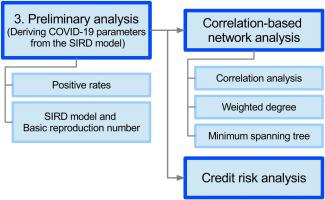

The novel coronavirus disease (COVID-19) is one of the worst pandemics in human history. Our research objective is to assess the contagion effect on Japanese firms and to evaluate the Japanese government's COVID-19 measures during the period from April 7, 2020, to May 25, 2020. We propose a susceptible-infected-recovered-dead model for COVID-19 and derive COVID-19 parameters for Japan. Subsequently, we analyze the effect of COVID-19 on Japanese firms through correlation-based network and credit risk analyses. The main findings are that the Tokyo Stock Price Index moved in the opposite direction of COVID-19 parameters and COVID-19 parameters are almost the only risk factors that impact a firm's credit risk during the period. Finally, we find that the interconnection analysis between the COVID-19 infection network and the financial networks contribute to the existing pandemic risk management knowledge.

中文翻译:

COVID-19 在日本公司的风险传染:一种网络方法

新型冠状病毒病 (COVID-19) 是人类历史上最严重的流行病之一。我们的研究目标是评估对日本企业的传染效应,并评估日本政府在 2020 年 4 月 7 日至 2020 年 5 月 25 日期间的 COVID-19 措施。我们提出了 COVID 的易感感染-康复-死亡模型-19 并导出日本的 COVID-19 参数。随后,我们通过基于相关性的网络和信用风险分析来分析 COVID-19 对日本公司的影响。主要发现是,东京股票价格指数与 COVID-19 参数的走势相反,而 COVID-19 参数几乎是该期间影响公司信用风险的唯一风险因素。最后,

京公网安备 11010802027423号

京公网安备 11010802027423号