Research in International Business and Finance ( IF 6.143 ) Pub Date : 2021-03-04 , DOI: 10.1016/j.ribaf.2021.101402 Ricardo Laborda , Jose Olmo

|

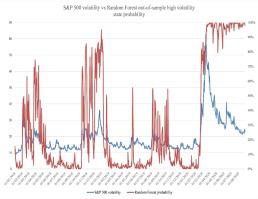

This paper measures volatility spillovers between sectors of economic activity using network connectivity measures. Volatility spillovers are an accurate proxy for the transmission of risk across sectors and are particularly informative during crisis periods. To do this, we apply the novel methodology proposed in Diebold and Yilmaz (2012) to seven economic sectors of U.S. economic activity and find that Banking&Insurance, Energy, Technology and Biotechnology are the main channels through which shocks propagate to the rest of the economy. Banking&Insurance is especially relevant during the 2007–2009 global financial crisis while the Energy sector and Technology are especially relevant during the COVID-19 crisis. We also show that volatility spillovers exhibit ability to predict high episodes of volatility for the S&P 500 index being useful as early financial crisis indicators.

中文翻译:

金融危机预测中各经济部门之间的波动溢出:跨越重大金融危机和Covid-19大流行的证据

本文使用网络连通性度量来衡量经济活动部门之间的波动性溢出。波动性溢出是跨部门风险转移的准确替代,在危机期间尤其有用。为此,我们将Diebold和Yilmaz(2012)提出的新颖方法应用于美国经济活动的七个经济部门,发现银行与保险,能源,技术和生物技术是冲击波传播到其他经济体的主要渠道。在2007-2009年全球金融危机期间,银行与保险业尤为重要,而在COVID-19危机期间,能源行业与技术业尤为重要。我们还表明,波动性溢出表现出了预测标普500波动性高发生的能力。

京公网安备 11010802027423号

京公网安备 11010802027423号